ISO 20022 protocol is a standard for electronic data interchange between financial services in the payment industry. It is based on DLT (distributive ledger technology) and uses ISO 20022 as a messaging mechanism.

ISO 20022 is a more advanced format based on the XML protocol and the Abstract Syntax Notation One (ASN.1) specification for bank communication, which meets the ISO 20022 standard for financial messaging. It better reflects today’s financial activities and transactions, locally, regionally, and globally.

Banks worldwide have already committed to this worldwide regulatory framework, which backs SWIFT and the Federal Reserve. And as we move toward this new quantum financial system, any third party that wants to interact with banks must be able to use the ISO 20022 format.

With the financial sector on the same page worldwide, there’s no question that ISO 20022 will be a significant catalyst for investors.

How is ISO 20022 changing in 2022

Banks and financial institutions worldwide are entering a new era as they gear up to switch their payment systems from using SWIFT messages to ISO 20022, a much more structured and>

Image Source: Temenos payments hub (webinar)

The following cryptocurrencies are ISO 20022-compliant as of this writing:

- Stellar (XLM)

- Hedera (HBAR)

- IOTA (MIOTA)

- XDC Network (XDC)

- Ripple (XRP)

- Algorand (ALGO)

- Quant (QNT)

Each of these cryptos was developed to make global transactions more accessible, and because of this, they could comply with the ISO 20022 standard more quickly.

However, as more cryptos do not want to be left out of the worldwide payment sector and move toward ISO 20022 compliance, this list will only expand.

And just because they follow ISO 20022 doesn’t necessarily mean they’re suitable investments…

Ripple is an excellent example of crypto with numerous disadvantages compared to benefits – and Helena Margarido encourages you to avoid it. (Here’s why.)

Hedera is a fascinating penny coin with a lot of potential that you can learn more about here, and it certainly belongs on your watchlist. (These picks were hand-chosen by our team of experts if you’re searching for penny coins that are flashing buys.)

What impact will ISO 20022 have around the world?

It is anticipated that this worldwide acceptance of similar financial messaging will significantly influence financial institutions, companies, and any organization with a stake in the finance and large value payments sector.

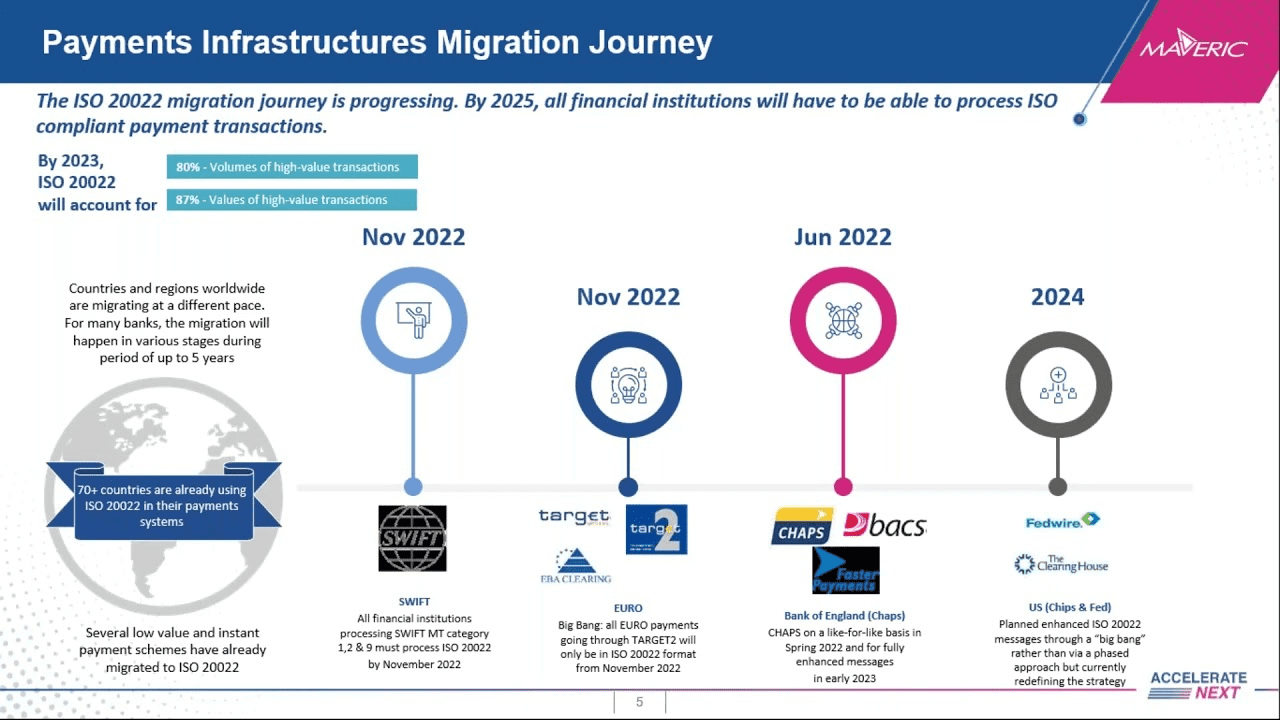

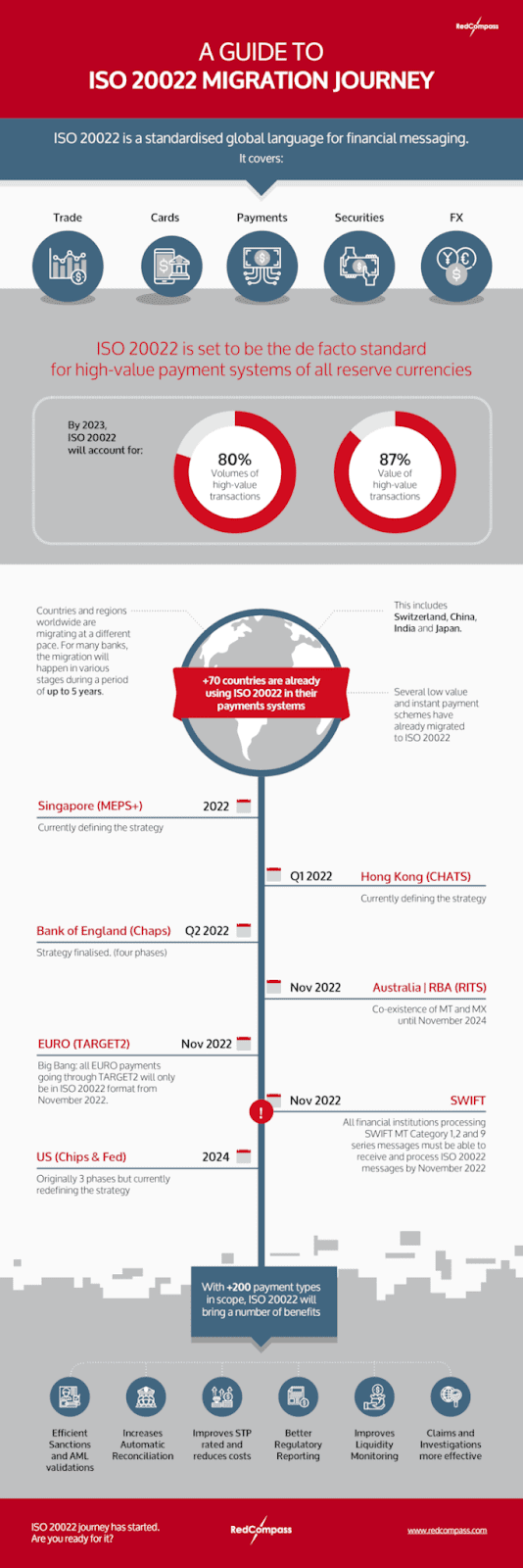

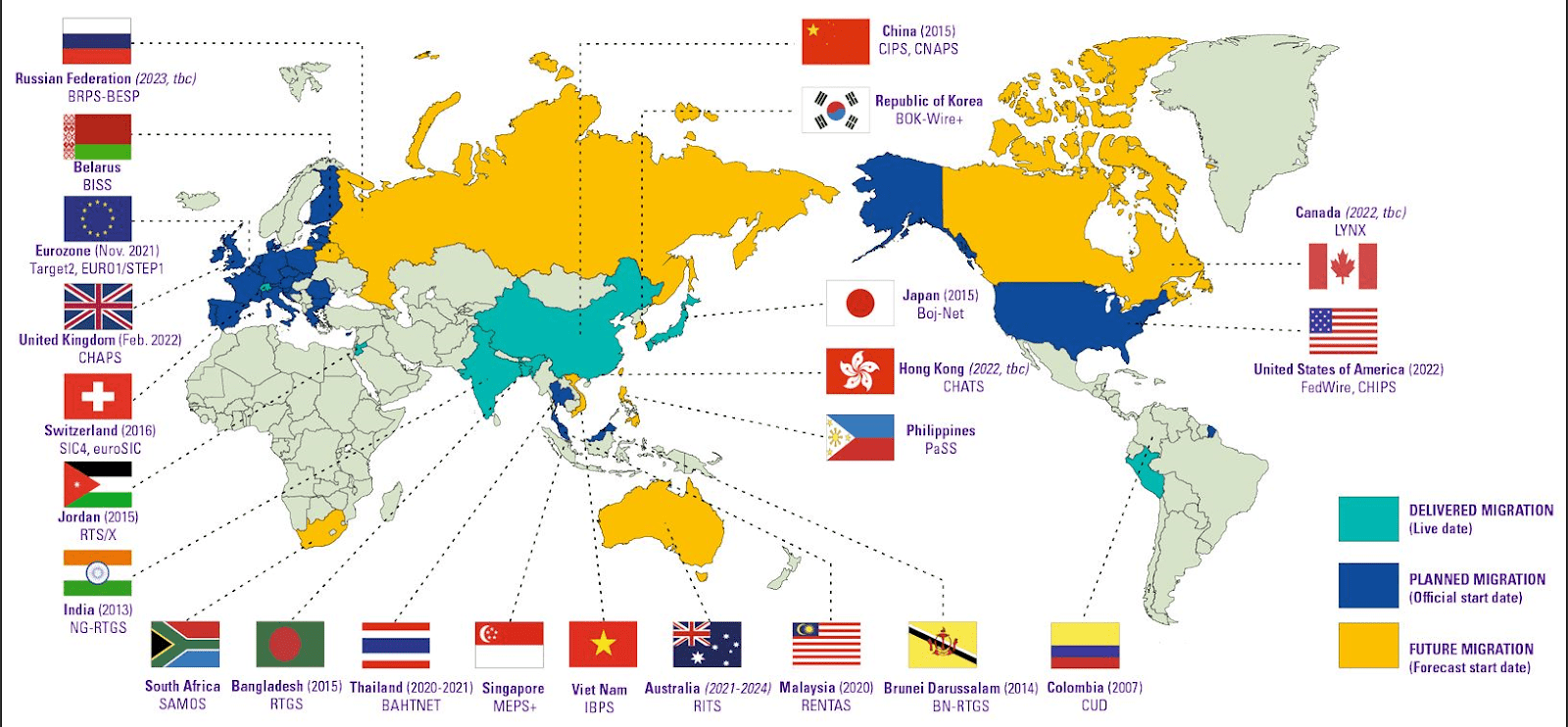

Over 70 countries have adopted ISO 20022 in their payment systems, including Switzerland, China, India and Japan. And with over 200 payment types in scope, it will harmonize formats and data components from different payment methods that could not previously work together.

ISO 20022 is now being used by over 70 countries, including Switzerland, China, India, and Japan, in their payment systems. With over 200 payment types, it will combine formats and data components from numerous payment techniques that could not previously communicate with one another due to differences in standards.

The ISO 20022 standard will apply to domestic, ACH, real-time, high-value, and cross-border payments.

Image Source: Red Compass

What banks must do to stay ahead of the competition

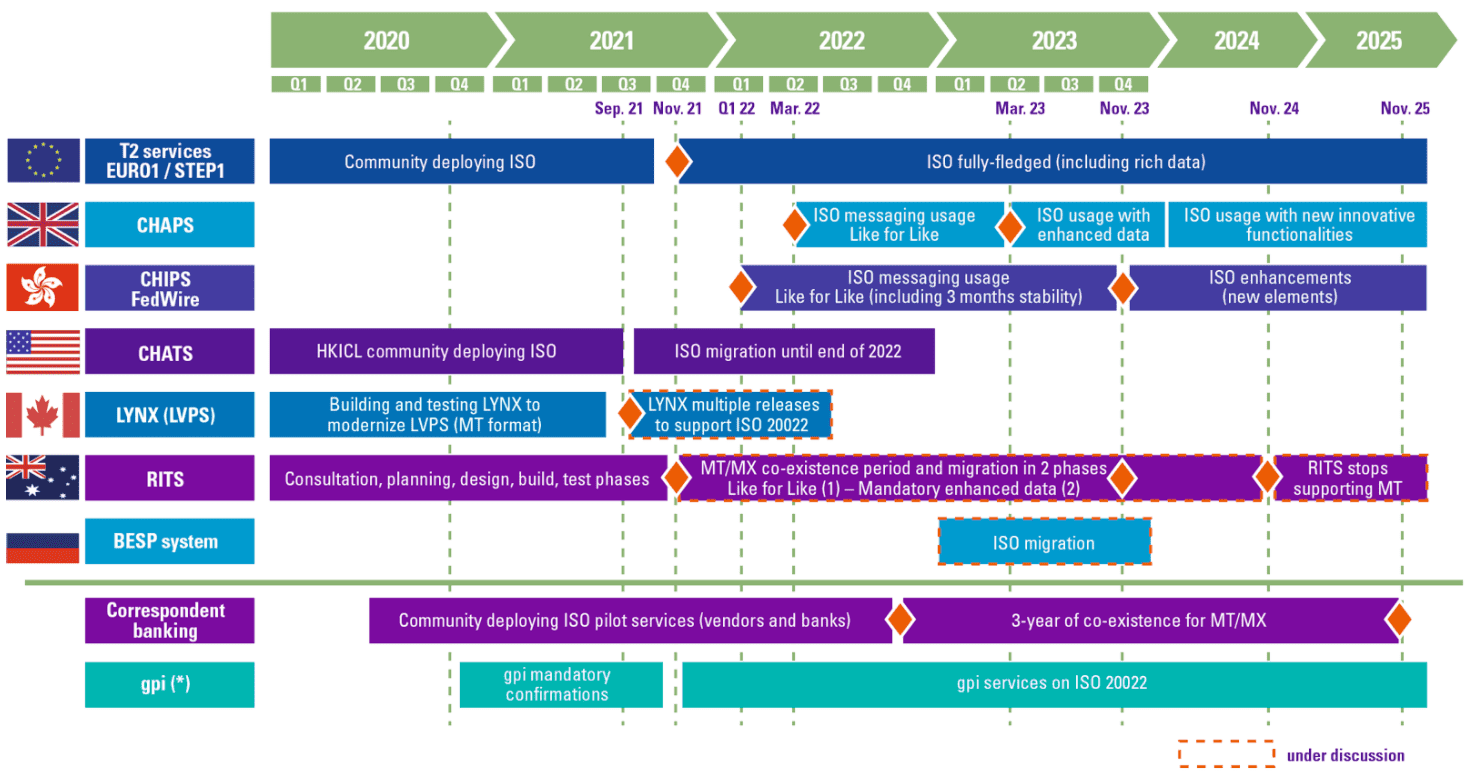

SWIFT’s technological shift from MT to ISO 20022 will be complete. Banks will need to upgrade their messaging interfaces and test them before November 2022 to ensure they are compatible with the new payment communication standard.

Banks are under competitive strain to migrate to the ISO 20022 standard as the overall migration of the payment industry toward immediate payments makes their existing goods and services vulnerable.

Because ISO 20022 is a more modernized and versatile standard than conventional legacy formats, it requires significantly greater data volume processing. As a result, bank systems and databases will need to be capable of handling these larger volumes at quicker speeds for real-time payments, daily liquidity management, compliance checks, and fraud detection and prevention.

It’s critical to allow enough time for testing so that syntax and formatting information is accurate, and the data’s migration into all linked payment and clearing systems. Testing should ideally be completed by the second quarter of 2022 at the latest.

Banks must inform their corporate customers about the additional data that may be accessible, as well as how it will be utilized. In addition, those clients should be completely informed and involved in end-to-end testing.

Image Source: Compact

High-Value Payments (HVPs) on ISO 20022

To establish a road map to standardization for high-value payments and real-time gross settlement (RTGS), the SWIFT, global central banks and market infrastructures have established the HVPS+ market practice task group.

“By unifying messaging standards across HPVs, participants in the payment system will be able to benefit from efficiencies and lay the groundwork for new services.” Michael Knorr, Wells Fargo Bank’s Head of Payments & Liquidity Management for Financial Institutions.

To stay on top of these high-value payment systems, you’ll need a solution to keep track of them. HVP systems are crucial to international finance, so monitoring these significant value transfers with the appropriate monitoring and performance management solution is critical.

RTGS is changing the global financial landscape

Image Source: Compact

Keeping up with new technologies, legal changes, and the introduction of new international payments standards is difficult. With ISO migration just around the corner, organizations can turn data into knowledge to ensure that worldwide payment systems run safely and effectively.