The US government’s regulation of DeFi is reaching a critical point, with Uniswap as its next major battleground.

Our industry as a whole must defend Uniswap’s role in the future of finance, or risk losing a foundational technology that allows decentralized ecosystems to thrive.

The New York outfit behind the popular DEX just agreed to pay $175,000 to the CFTC for facilitating retail trade of a suite of leveraged index tokens, which, going by the tickers in the complaint, were built by Index Coop.

Part of the CFTC settlement dictates that Uniswap Labs must cease offering those kinds of tokens to the general public.

Pairs for those tokens are no longer available through Uniswap Labs’ own front-end for the DEX. The website says “Not available. You can’t trade this token using the Uniswap App.”

Uniswap Labs can technically block as many tokens as it likes on its web app for US residents, but the tokens will still be tradable on the technology itself underneath, either through a different web app or by interacting with the smart contracts directly with code.

Watch for that particular nuance to be debated ad nauseam should the Securities and Exchange Commission follow through with its Wells notice and actually sue Uniswap Labs.

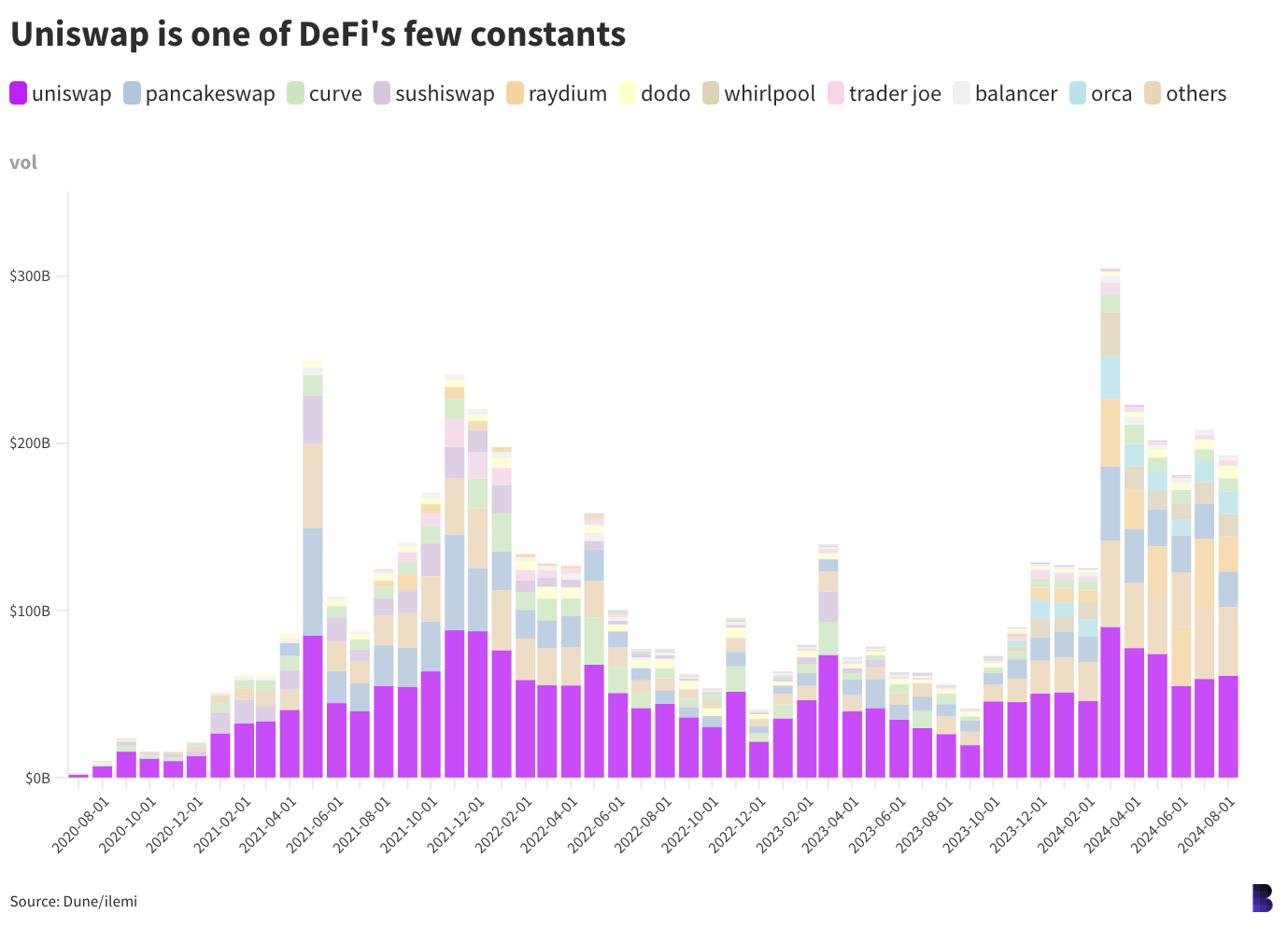

The firm itself is a bedrock of DeFi, on par with Maker (which has recently rebranded to Sky). Uniswap volumes have stayed relatively consistent over the years despite waves of new trading platforms looking to eat its lunch.

With this in mind, if and when Uniswap Labs goes to court, they’d be doing so on behalf of all of DeFi. That’s a different battle than, say, the fight to prove that bitcoin and ether are “money,” or at the very least, commodities.

Read more: CFTC Commissioners dissent on Uniswap settlement

Money is just one of many apps for blockchains. But so far, it’s clearly the most popular.

Bitcoin is perhaps the purest expression of the money app in the blockchain context. And the bitcoin war has been largely fought and won — the CFTC has long considered it a commodity and the SEC never stood a chance of finding Satoshi Nakamoto in any case.

The ETF issuers and other lobbyists, in my view, planted the victory flag in the war over crypto’s potential moneyness.

ETH gained its own commodity label in light of bitcoin winning that fight. And while a commodity classification doesn’t automatically make either bitcoin or ether “money,” it does put them on par with more ancient currencies with intrinsic value, such as silver and gold. Which is just as good.

Running political defense of bitcoin these days isn’t so much about the right to transact digital money peer-to-peer as it is about the right to mine bitcoin, especially in areas that haven’t been so receptive to the industry.

Just as it is possible to separate money (the app) from the blockchain, it’s also possible to separate Uniswap, the front-end app, and Uniswap, the technology — the bundle of smart contracts that make its trades, listings and liquidity provision possible.

At least, that’s what Uniswap Labs will most likely have to prove again and again.

Vitalik (and other smart city proponents) might wish for our minds to immediately go to other use cases when we think of blockchains. Tokenized digital identities, wedding registries and driver’s licenses, not memecoin trading and yield farms.

They might have a point. There could very well be more to life than recreating traditional finance on blockchain rails.

One day, the world may run on smart contracts and AI-agents. Until then, DeFi is arguably crypto’s most vibrant user base — and right now, protecting it is critical.

A modified version of this article first appeared in the daily Empire newsletter. Subscribe here so you don’t miss tomorrow’s edition.