Crypto asset prices are not the only things to have recovered over the past couple of months. Blockchain-based lending is also seeing a revival following the big slump in 2022 during the slew of crypto collapses and contagions.

On December 19, Bloomberg reported that blockchain-based private credit lending has seen a partial revival in 2023, with active loans up 55% since the start of the year.

Blockchain Loan Revival

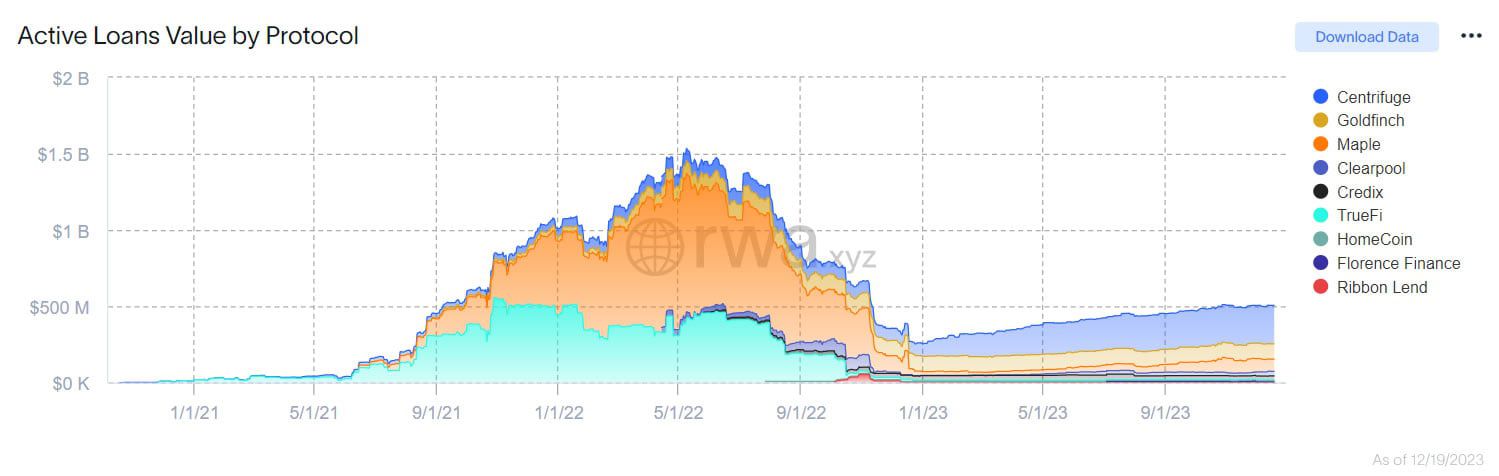

Blockchain loans have climbed to about $500 million, according to tokenized private credit tracker RWA.xyz. However, this is still below the $1.5 billion peak last June.

Centrifuge is the market leader for tokenized private credit with $257 million in active loans.

Additionally, blockchain lending protocols can charge lower interest rates than traditional private credit lenders. Interest rates on crypto loans can be less than 10% compared to double-digits with traditional lenders.

This is because the transparency of blockchains and automated smart contracts reduce risks. Agost Makszin, co-founder of Lendary Capital, commented on the reduced risks:

“This has likely resulted in lower borrowing rates compared with traditional private credit, which is often slower and has a longer liquidation process.”

Read more: Real World Asset (RWA) Backed Tokens Explained

Consumer loans, auto loans, fintech, real estate, carbon projects, and crypto trading make up most of the blockchain lending activity currently. Consumer and auto loans have the largest shares, with over half the total between them.

“Bullish on-chain private credit markets,” commented Circle CEO Jeremy Allaire on December 19. Nevertheless, it is still a fraction of the booming $1.6 trillion traditional market for private credit.

Furthermore, last year’s crypto collapse hurt the credibility of digital asset lending when several speculative lending and borrowing projects failed.

Crypto Credit Obstacles Remain

Additionally, several obstacles remain for the fledgling finance sector. These include banking barriers and uneven access to banks for crypto companies. There is also skepticism from traditional finance about crypto and blockchain tech and a lack of credit rating systems.

Nevertheless, protocols such as Centrifuge, Maple Finance, and Goldfinch are showing recovery. They can provide access to investor funds, typically using the Ethereum blockchain and stablecoins, allowing borrowers to access the funds under terms set in smart contracts.

Maple Finance co-founder Sidney Powell said, “We’ll try and leverage the fact that we use the blockchain and smart contracts to manage our loans, take out costs, and fund loans quicker, to try and get a competitive edge,”

Bloomberg concluded that it was unclear if blockchain lending would ever reach a large scale. However, real-world asset tokenization could bring more collateral and lending.