On June 30, 2024, the regulation “Markets in Crypto Assets” (MiCA) will officially come into effect within the European territory, and significant measures will be introduced to curb the expansion of stablecoins managed from overseas in order to favor those local ones correlated to the EURO.

The leading exchanges of the continent such as Binance, OKX, and Kraken have already prepared for the regulatory change and have revised some of the products offered to their customers in Europe.

All this could, however, limit the technological expansion of the Union in the crypto sector, leading to a general regression rather than growth.

Let’s delve deeper into the topic in this article.

Summary

MiCA and stablecoin: the crypto regulation that limits electronic money issuers will come into effect on June 30

On October 10, 2023, the regulation “Markets In Crypto Assets” (MiCA) was approved by the European Parliament with a favorable vote of 28 members, and now it is about to come into force, officially marking the introduction of the first EU regulation that governs the crypto sector.

The topics present in the new Text are aimed at a wide range of subjects operating in the industry, such as issuers of crypto-assets, providers of services related to crypto-assets (CASP), and cryptographic exchange platforms, addressing key issues such as consumer protection, new obligations for anti-money laundering, environmental impact, and corporate social responsibility.

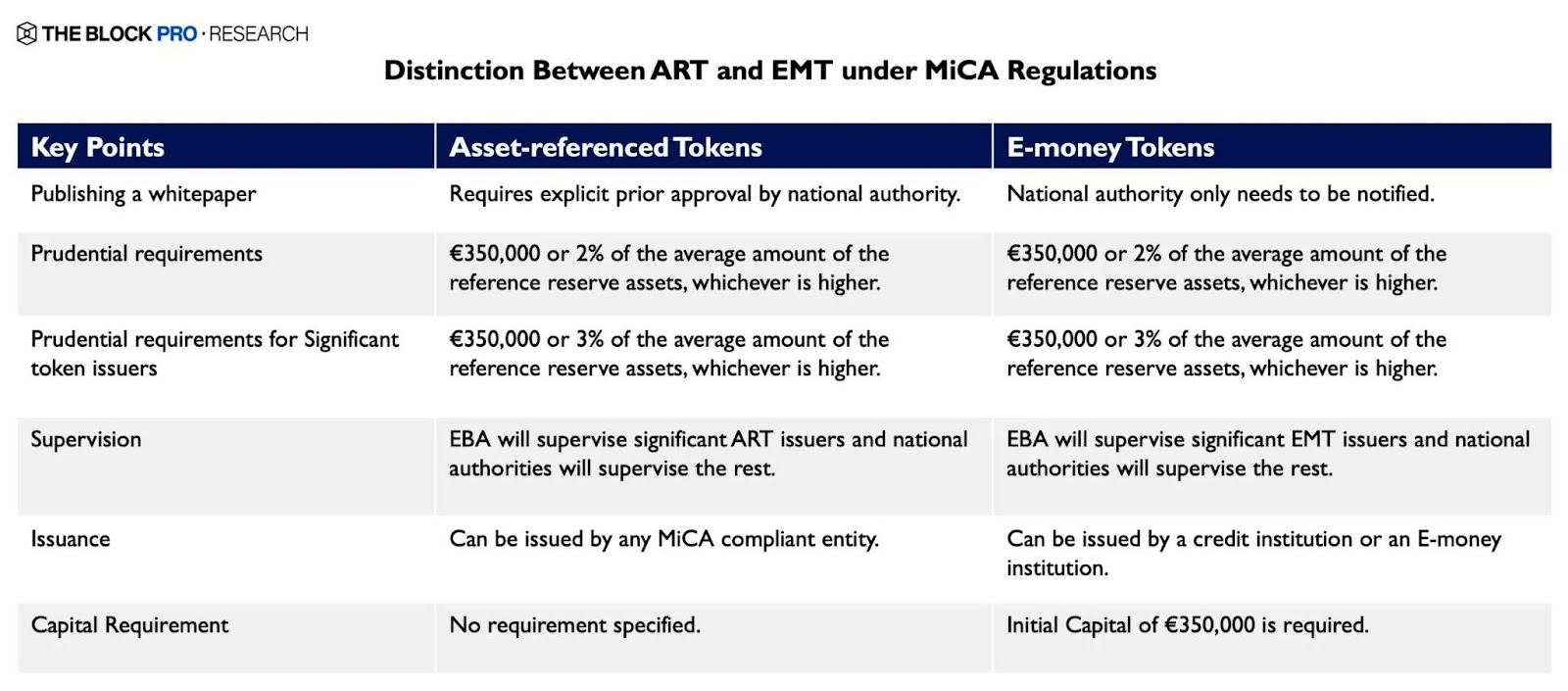

An entire section of the regulation is, however, dedicated exclusively to the world of stablecoins, more precisely in relation to the issuers of e-money token (EMT), that is, a specific type of crypto-asset that aims to maintain a stable value by referring to the value of an official currency.

This definition distances itself from that of asset-referenced token (ARTs) which identifies crypto-assets aimed at maintaining a value relative to the combination of multiple assets or official currencies.

The MiCA establishes the tax relevance of exchanges (swaps) between cryptocurrencies and e-money tokens, while exchanges from cryptocurrencies to asset-referenced tokens should not be considered in this sense.

The new MiCa regulation also stipulates that the only stablecoins allowed to be freely traded in Europe are those that meet certain requirements, such as their supervision by the European Banking Authority (EBA) and the presence of a specific “electronic money license”.

These requirements strongly limit some established stablecoins both in Europe and in other continents such as $USDT, which becomes effectively illegal due to the lack of the specific license, obtainable in case of deposit of collateral assets at a credit institution based in the EU.

Furthermore, the new law that will soon come into effect sets a maximum limit of 200 million euros of daily trading volume (quarterly average): this number is much lower compared to the volumes recorded daily by the major stablecoins in the crypto market.

According to some experts on the subject, such as Mathieu Hardy from the OSOM wealth management app, this limitation of MiCa on the stablecoin front can be considered a strong discrimination against electronic money tokens with a peg in USD.

Observing the average volume of the last 30 days of the main USD stablecoins, we can see how the top 10 diversified coins by blockchain of belonging would abundantly exceed the limit of 200 million euros daily.

Monthly stablecoin transfer volume breakdown: https://t.co/wWd6qcES3n pic.twitter.com/MGnRSxX028

— Token Terminal (@tokenterminal) June 19, 2024

Kaiko Research: a springboard for EURO-pegged stablecoin crypto

According to Kaiko Research, the imminent MiCA regulation in Europe could reassess the scope of EURO-pegged stablecoins, issued and managed by companies based within the Union.

The new regulation is indeed seen as a springboard for local emoney tokens, which currently record volumes still particularly low compared to those of other foreign e-money tokens.

Already in recent months, several credit institutions have moved to offer their own stablecoin, such as Société Générale with the launch of EURCV.

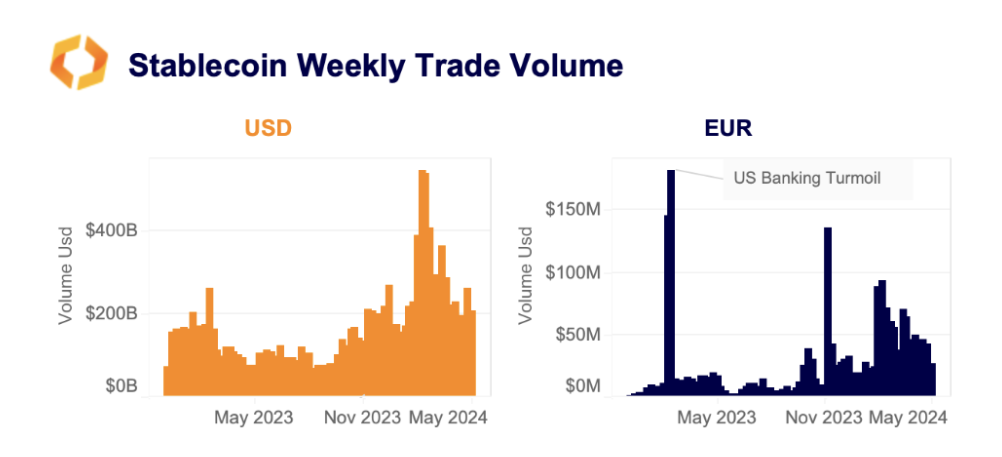

From October 2023 onwards, ever since the European Parliament approved the MiCA regulation, the weekly trading volumes of stablecoins pegged to the EURO have seen a strong increase, even temporarily surpassing 100 million, suggesting that demand is finally increasing in European markets.

We remind you, however, that the road to competing with products pegged to the US dollar is still very long.

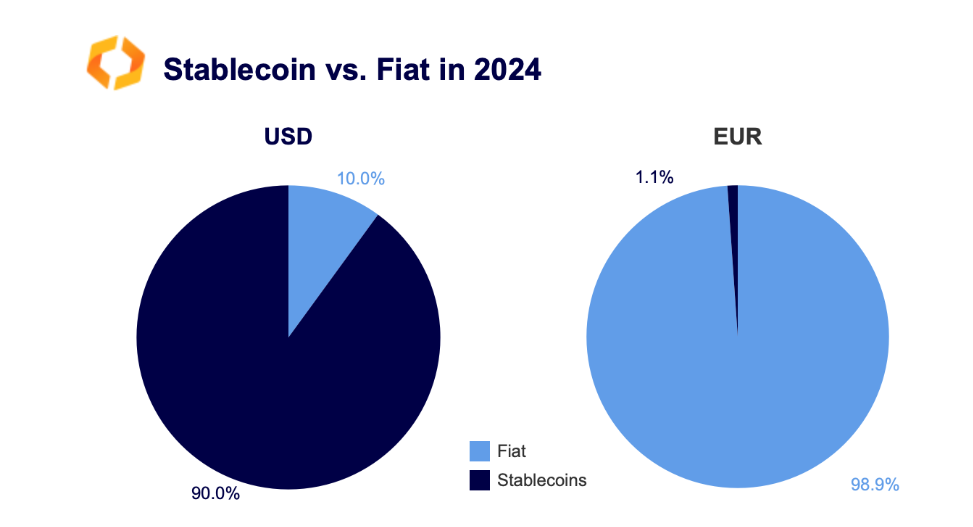

As of today according to the data from The Block, 99.3% of the market share of Ethereum stablecoins is dominated by those in USD, while the respective currencies in EUR collect just 0.63%.

The euro is still the “second best choice” compared to other FIAT currencies outside of the dollar in this context, being the second most used currency in the stablecoin field.

Overall, the USD-backed stablecoin continues to dominate the bull and bear cryptocurrency market.

Almost 90% of all crypto transactions are executed using USD-backed stablecoins relative to the USD.

Their average weekly volume in 2024 was 270 billion dollars, which is 70 times higher compared to their EU counterparts. On the contrary, only 1.1% of all transactions are carried out using Euro-backed stablecoins.

However, it is worth noting that this share has increased from almost zero in 2020 and is currently at historic highs.

While only time will tell if the introduction of Mica will push EUR-pegged stablecoins to compete with those overseas, in the meantime experts already agree that the regulation is having a positive impact on the crypto sector even before it actually comes into effect.

For example, Dante Disparte, the Head of Global Policy at Circle, observed in a post on X that thanks to regulatory development in Europe, the share of VC investments in cryptographic projects on the continent has increased by almost 10 times from 2022 to 2023, rising from the initial 5.9% to 47.6%.

In the same period, the share of VC investments in the United States and Dubai has significantly decreased.

The MiCA effect 🇪🇺🚀

— Patrick Hansen (@paddi_hansen) May 9, 2023

The share of VC investment into European crypto projects is up almost 10x in one year – from a share of 5.9% in Q1 2022 to 47.6% in Q2 2023.

Regulatory clarity attracts capital & entrepreneurs from around the world. Great development for crypto in Europe! pic.twitter.com/kUVp3rwlg3

Exchange, Tether e $USDT: la regolamentazione MiCA come passo indietro per l’Europa

The major crypto exchanges operating in Europe have already prepared for the regulatory earthquake that will soon be unleashed with MiCa, and have proceeded to delist from their trading-pairs those stablecoins that are found to be non-compliant with the regulation.

Binance has announced in this regard that it has differentiated its offering between stablecoin “regulated” and “unauthorized”, without however explicitly referring to which coins will be excluded for European customers.

What we know for the moment is that the launchpads in FDUSD will be suspended, and that the rewards in $USDT for the “Spend-to-Earn” section will no longer be credited after June 29, except for the rewards accrued before that period: However, it is not clear if $USDT, which turns out to be the stablecoin most affected by the new regulation, can still be traded on Binance’s spot and futures markets.

The exchange OKX, on the other hand, delisted $USDT already in March, without referring to the MiCa regulation but with obvious underlying connections, while Kraken recently denied intentions of a similar delisting.

In the meantime, from the latest news from the crypto market, the decision of UpHold to delist on July 1, 6 stablecoins including $USDT, $DAI, $FRAX, $GUSD, $USDP, and $TUSD, excluding $USDC from the list, emerges.

Cryptocurrency exchange Uphold announced that due to the MiCA in Europe on June 30, it will stop supporting multiple stablecoins, including Tether ($USDT), Dai ($DAI), Frax Protocol ($FRAX), Gemini Dollar ($GUSD), Pax Dollar ($USDP) and TrueUSD ($TUSD) from July 1. They will be…

— Wu Blockchain (@WuBlockchain) June 18, 2024

The bullism of MiCA towards USD-pegged stablecoins, although motivated to leave space for EURO counterparts, could generate onboarding problems for European customers of exchanges, who still use $USDT as the main means to transition from FIAT to CRYPTO.

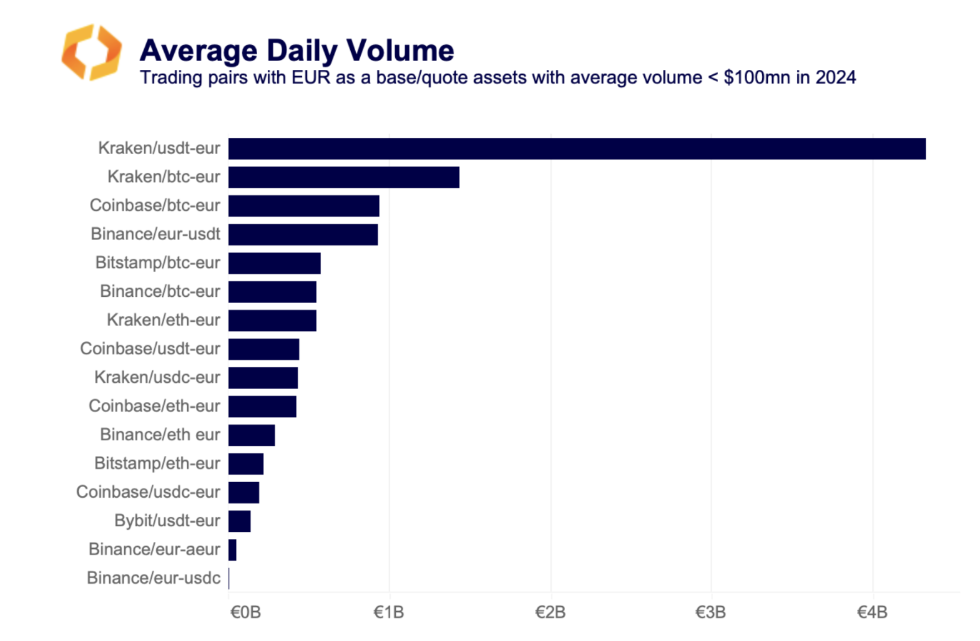

In fact, as highlighted by the data from Kaiko Research, both on Binance and Kraken, the $USDT-EUR pair turns out to be a more traded instrument in terms of volumes compared to BTC-EURO, demonstrating that Tether’s currency represents an essential resource for European markets.

In such a context, while OTC trading will continue to provide $USDT-EUR liquidity, many traders might choose to rotate towards regulated alternatives like $USDC.

Paolo Ardoino, current CEO of Tether, has strongly criticized the upcoming Mica regulation, emphasizing how the requirement for issuers to hold at least 60% of reserves in bank deposits acts as a counter-efficient measure in terms of security for the end customer.

In fact, the European Central Bank insures only bank deposits up to 100,000 euros, a figure significantly lower than the market capitalization of $USDT, which amounts to 112 billion dollars.

Imposing on issuers like Tether to establish their reserves with simple bank deposits to become compliant with the regulations offers a possible premise for one of the largest financial disasters in the world of cryptographic finance in case of a collapse of the custodian bank.

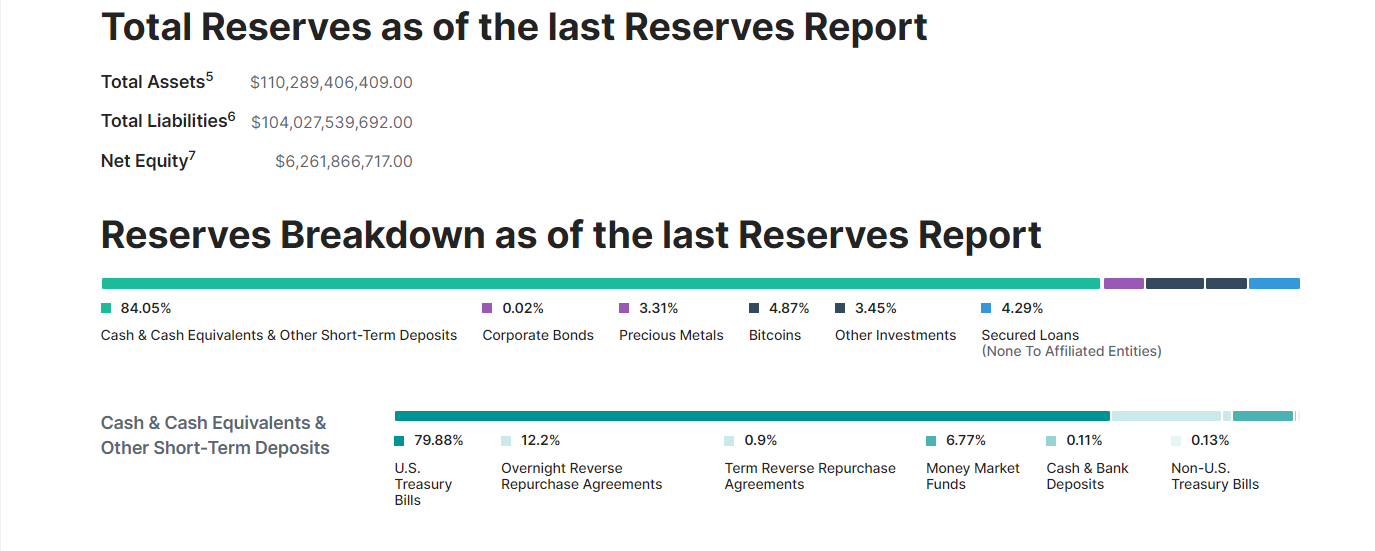

We remind that Tether currently holds reserves in cash and equivalents, US treasury securities, precious metals, Bitcoin and other investments, offering a perfectly differentiated asset allocation weighted according to the financial situation of the tech giant, which in the first quarter of 2024 recorded profits of 4.5 billion dollars.