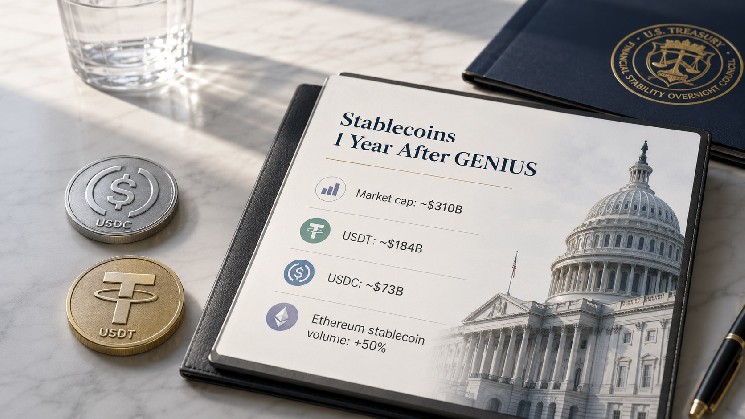

On the eve of the $GENIUS Act’s first anniversary, the stablecoin market holds about $310 billion, including roughly $184 billion in $USDT and $73 billion in $USDC.

President Donald Trump signed the law on July 18, 2025, creating a federal framework with one-for-one liquid reserves, redemption rights, and monthly reserve disclosures for a market that moved faster than the rulebook.

Federal Reserve researchers measured stablecoin capitalization at $317 billion on Apr. 6, up more than 50% from early 2025, and recorded a 50% increase in Ethereum stablecoin transaction volume since enactment. As of July 17, core implementation measures are still in proposal form.

Kyle Sonlin, president and co-founder of Global Settlement Network, said his conversations with governments and institutions now start from acceptance of stablecoins as financial infrastructure, and his team spends “far less time explaining why stablecoins matter.”

| Metric | Current / recent figure | Why it matters |

|---|---|---|

| Total stablecoin market cap | ~$310B | Shows $GENIUS is regulating a large, systemically relevant market |

| Fed April 6 stablecoin market cap estimate | $317B | Confirms market crossed the $300B threshold during $GENIUS’s first year |

| Market-cap growth since early 2025 | >50% | Shows adoption accelerated before implementation finished |

| $USDT market cap | ~$184B | Highlights Tether’s continued dominance |

| $USDC market cap | ~$73B | Shows Circle remains the largest regulated-U.S.-aligned competitor |

| Ethereum stablecoin transaction volume since enactment | +50% | Shows activity increased alongside capitalization |

Permission reached the sales desk

Sonlin described $GENIUS as a credible federal direction that let banks, payment companies, and infrastructure providers commit money to longer-term plans.

He said that financial infrastructure rarely reorganizes within 12 months, and companies kept preparing for a regulated stablecoin market as agencies worked through implementation.

Triple-A CEO Eric Barbier sees the commercial result inside the enterprise sales funnel. His payment company has recorded more businesses moving from evaluation toward implementation, plus a “marked reduction” in sales cycles for enterprise customers that enable stablecoin payments through its platform.

Barbier’s evidence covers Triple-A’s own pipeline, providing the legitimacy thesis with a concrete operational measure.

Visa’s expansion offers a larger institutional reference point, as its stablecoin settlement pilot supported nine blockchains by April and reached a $7 billion annualized settlement run rate, up 50% from the previous quarter.

On July 16, Visa introduced an enterprise platform that provides financial institutions and fintech firms with access to stablecoin storage, redemption, minting, and burning through a single Visa-managed environment.

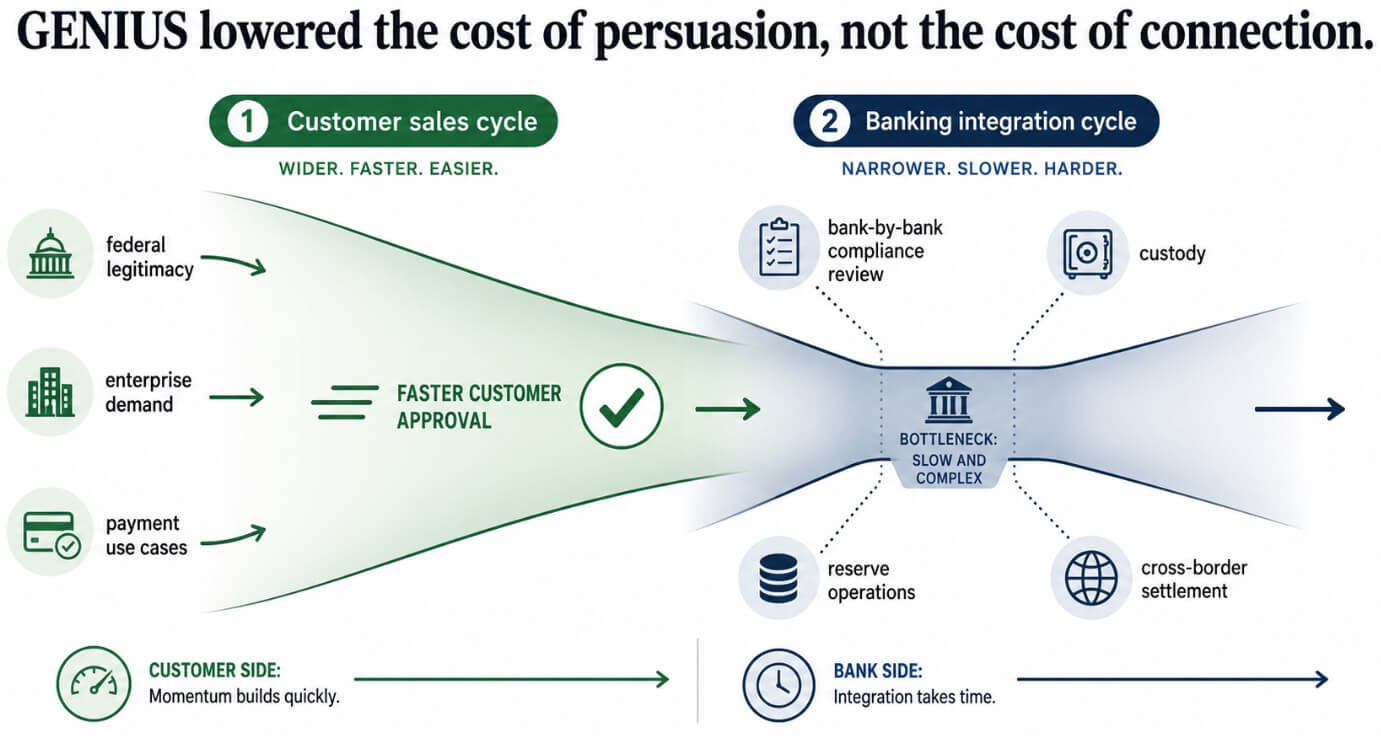

The sales environment now has a recognized product, a federal direction, and payment incumbents building access layers.

Deployment depends on banks, custody arrangements, reserve operations, and compliance teams that interpret unfinished rules for each relationship.

Banking friction survives

Diogo Cassinelli, sales and partnerships manager at Trace Finance, said that clarity on issuance addressed half of the operating problem.

Cross-border payment companies still need each banking partner to make an independent compliance judgment about how stablecoins enter accounts, leave accounts and settle across jurisdictions.

Cassinelli said those reviews add “months to timelines that should take weeks,” and the cost repeats whenever an operator enters a new country or adds another bank.

Stablecoin providers can close a customer faster under $GENIUS, then spend longer connecting that customer to the banks and payment providers that move the money.

Enterprise buyers now understand the use case and accept the federal direction. Banking partners still need a shared legal and supervisory standard that lets compliance teams approve the same activity consistently.

Edwin Mata, CEO and co-founder of Brickken, placed that plumbing inside a larger capital-markets architecture.

Regulated dollars can provide the cash leg for tokenized securities, private credit, investment funds, and asset servicing. The US opportunity extends from payment acceptance into issuance, distribution, and settlement across on-chain financial products.

Regulatory access sets the field

Alex Witt, general partner at Verda Ventures, gave the first-year verdict a harder edge. He credited $GENIUS with legitimizing the sector and drawing institutional firms into the federal perimeter.

Witt also argued that charter decisions and product launches can give selected firms an early advantage before regulators complete the operating rules.

The Office of the Comptroller of the Currency conditionally approved national trust bank applications or conversions involving Ripple, Fidelity Digital Assets, BitGo, Paxos, and First National Digital Currency Bank in December 2025.

Tether launched USA₮ in January 2026, with Anchorage Digital Bank as the issuer and Cantor Fitzgerald as the reserve custodian and preferred primary dealer.

Those moves show companies building toward $GENIUS before its effective date. They also concentrate early access among firms that already have capital, legal teams, banking partners, and federal relationships.

Startups face the same unfinished framework with fewer resources to absorb repeated compliance reviews.

The OCC opened its broad implementation proposal in February, and Federal agencies published an interagency customer-identification proposal in June. Public comments stay open through Aug. 21, more than a month beyond the anniversary deadline Congress set for regulations.

The January test

The Senate Banking Committee advanced the CLARITY Act 15-9 on May 14, leaving the bill short of a floor vote.

In the bull case, final $GENIUS rules and further CLARITY progress give banks a common compliance reference, contract integration timelines, and turn regulated stablecoins into routine settlement assets for payments and tokenized markets.

The bear case gives early access durable value, as conditional charter approvals, incumbent payment networks, and established banking partnerships let a small group define distribution before smaller firms can comply at comparable speed.

$GENIUS then legitimizes the category and channels much of its commercial value toward companies that entered the federal perimeter first.

| Scenario | What happens before Jan. 18, 2027 | Winners | Risk |

|---|---|---|---|

| Bull case: rules lower connection costs | Final $GENIUS rules give banks a common compliance reference; CLARITY progresses | Payment firms, stablecoin issuers, tokenized-asset platforms, banks | Integration timelines shorten and stablecoins become routine settlement rails |

| Base case: legitimacy stays ahead of plumbing | Rules remain incomplete or unevenly interpreted; banks continue individual reviews | Larger firms with compliance teams and existing bank relationships | Stablecoins remain easier to sell than to deploy |

| Bear case: early access hardens | Conditional charters, payment-network access and banking relationships define distribution first | Incumbents and well-capitalized firms | Startups face higher compliance costs and slower market access |

| Policy-delay case: uncertainty persists | Comment periods, agency coordination and CLARITY delays stretch beyond expectations | Firms able to wait and absorb legal costs | Adoption continues, but operational fragmentation remains |

The statute takes effect on the earlier of Jan. 18, 2027, or 120 days from the date federal regulators issue final implementing regulations.

The first year lowered the cost of persuasion, and the six months through Jan. 18 will show whether federal rules can lower the cost of connection too.