Buried deep within Ripple’s developer documentation sits a page that, until recently, drew little attention outside engineering and payments compliance circles. The page lists bank identifiers, featuring short numeric codes used to route international payments, organized by country and, in some cases, by individual financial institutions.

Before now, the document served a narrow purpose. Notably, it helps payment operators configure beneficiary details correctly when sending cross-border transactions.

Then the $XRP community discovered it. Soon after, screenshots spread rapidly across social media. Commentators pointed to the sheer size of the list as evidence of something much larger.

WOW! 💥

RIPPLE has assigned BANK IDs to over 500 BANKS! 🏦🔥

And some people still think #$XRP won’t be used?! 🤡

The train is moving full speed either you’re on board or you’re getting left behind! 🚀🚀🚀#XRPArmy #XRPCommunity #QFS #crypto pic.twitter.com/wLqiCJurLe

— $XRP Warrior (@$XRP_Warrior_) May 30, 2026

Discussions exploded across forums and $XRP community channels, with many users interpreting the document as proof of massive $XRP adoption, widespread bank integration, and future price acceleration. However, the document itself had not changed. Only the audience reading it had.

This article examines what Ripple’s bank identifier list actually contains, why the company created it, and where the line sits between legitimate insight and speculative overreach. For investors, fintech professionals, and curious observers alike, understanding that distinction matters.

A Ripple Document Few People Noticed Is Now Drawing Industry Attention

Most technical documentation exists quietly in the background. API references, routing tables, and configuration guides are written for engineers and compliance teams who need operational precision rather than headlines. Ripple’s bank identifier page was no different. The company placed it within its Payments ODL documentation as a reference tool for operators configuring beneficiary payouts in different markets.

Notably, Ripple never presented the page as a major announcement. The company issued no press release, executives made no public statements about it, and investor briefings never highlighted its contents. By all appearances, it functioned as a technical appendix.

Nonetheless, once members of the $XRP community began circulating screenshots online this month, the reaction became immediate and widespread. The apparent scale of the document, covering dozens of countries and hundreds of institutions, seemed to provide concrete evidence of Ripple’s global network reach. For a community that has spent years searching for proof of institutional adoption, the document felt significant.

As interest grew, attention expanded beyond retail crypto circles into fintech media and institutional analyst discussions. Those observers began asking a more precise question: What exactly does this bank ID list represent, and do its contents support the conclusions many people are drawing from it?

Why Do More Than 500 Financial Institutions Appear in One Place?

The first thing most readers will notice about Ripple’s bank identifier documentation is the sheer volume of institutions listed across multiple regions. For the uninitiated, the document can resemble a roster of Ripple partners or $XRP adopters. In reality, the reason so many names appear in one place is more procedural than strategic.

The Numbers Behind the Discussion

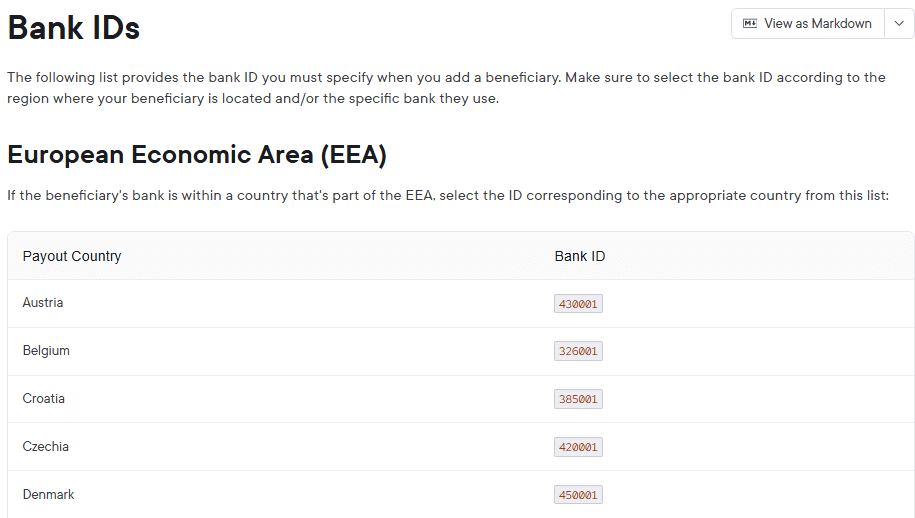

Ripple’s bank identifier document covers several regions, including Asia, Europe, the United Kingdom, and Oceania. The European Economic Area (EEA) section lists 26 countries, each assigned a country-level identifier. Meanwhile, the United Kingdom section includes the mainland alongside overseas territories such as Gibraltar, Jersey, Guernsey, and the Isle of Man, with identifiers varying by territory and payout currency.

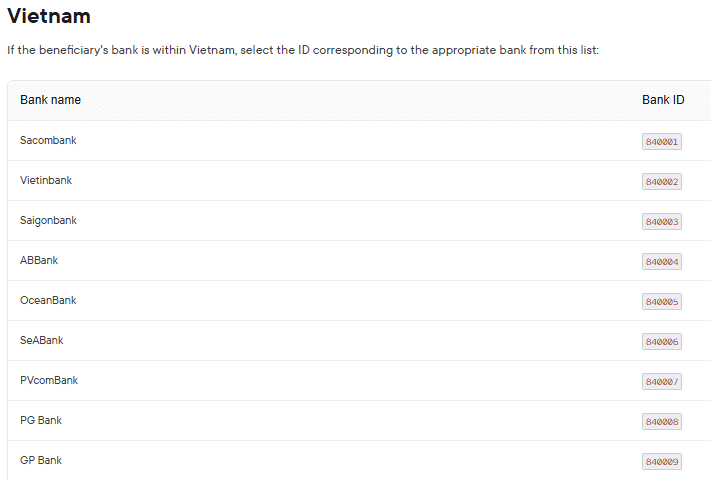

In Asia, several countries were included, such as Vietnam, China, South Korea, Thailand, and Indonesia. Specifically, Vietnam appears far more granular. The documentation lists more than 50 individual banks by name, each assigned its own unique numeric identifier.

When combined, these entries extend well above 500 banks. To readers expecting a curated partnership directory, the numbers appear striking. Yet for payments engineers familiar with routing infrastructure, the list simply reflects the large number of institutions operating within the payment corridors Ripple’s infrastructure supports.

Regions Represented in the Records

The document spans several of the world’s most active cross-border payment corridors. Europe processes enormous volumes of international transfers through the SEPA framework, while the United Kingdom continues handling substantial EUR- and GBP-denominated payment activity after Brexit.

At the same time, Vietnam has emerged as one of Southeast Asia’s most important remittance destinations, receiving significant inflows from diaspora communities across North America, Europe, Japan, and South Korea.

These are not random markets. Instead, they represent regions where legacy payment systems remain costly and inefficient, making them attractive targets for fintech innovation and blockchain-based payment infrastructure. Consequently, Ripple’s documentation reflects deliberate strategic focus rather than accidental expansion.

Why the List Appears Larger Than Expected

One major reason the document appears so extensive is the difference in how regions structure their routing systems.

Within Europe, a single identifier covers all banks inside a country. For example, a payment to France uses one country-level code regardless of whether the recipient banks with BNP Paribas, Société Générale, or a regional institution.

Vietnam, for instance, operates differently. There, routing architecture works at the institutional level. BIDV has its own identifier. Techcombank has another. HSBC Vietnam also uses a separate code.

Importantly, this structure is not unique to Ripple. It mirrors Vietnam’s domestic banking conventions. However, it also creates the visual impression that Ripple maintains dozens of separate banking relationships in Vietnam, when in reality the system simply uses a more granular technical structure than Europe’s country-wide approach.

Understanding this distinction is essential before drawing broader conclusions.

What Ripple Intended These Identifiers to Accomplish

Every piece of payment infrastructure exists to solve an operational problem. Ripple’s bank identifiers are no exception.

Operational Functions Behind the Entries

When a payment operator uses Ripple Payments, formerly ODL (On-Demand Liquidity), to send funds internationally, the system must route the transaction accurately to the correct beneficiary institution.

Beneficiaries are not abstract entities. They hold accounts at specific banks operating within specific regulatory and settlement systems. Consequently, Ripple’s infrastructure needs a reliable way to identify those institutions.

The bank identifier acts as that routing key. It maps a beneficiary institution to the correct settlement pathway. Without accurate identifiers, payments can fail, become delayed, or land in the wrong account. In other words, the identifiers form part of Ripple’s operational configuration layer rather than a public registry of partnerships.

How Payment Networks Organize Institution Data

Every major cross-border payment network relies on institutional identifiers in some form. For instance, SEPA depends on IBAN structures. The UK’s Faster Payments network uses sort codes, while India’s IMPS system relies on IFSC identifiers.

Ripple’s bank ID list follows the same principle. It functions as a structured routing reference that allows payment software to direct funds correctly across different markets and banking systems.

As a result, the existence of such a list demonstrates that Ripple has built operational payment infrastructure. However, it does not prove that every listed institution actively uses Ripple’s network or $XRP itself.

Why Accuracy Matters in Cross-Border Transfers

In cross-border payments, routing accuracy is critical. Misrouted funds can take days or even weeks to recover. In some jurisdictions, recovery may not happen at all.

Additionally, regulators require financial institutions to maintain precise transaction records identifying both the sending and receiving institutions. Compliance teams therefore treat routing data as a core risk-management function rather than a technical afterthought.

For that reason, Ripple’s documentation must remain highly detailed and comprehensive. The thoroughness of the list reflects operational necessity, not necessarily widespread adoption.

The Assumption Driving Many $XRP Headlines

Misinterpreting technical documentation is not unique to Ripple. However, within the $XRP community, evidence of institutional connectivity often becomes closely linked to expectations of future price appreciation.

Sources for the Adoption Narrative

Many $XRP supporters believe Ripple’s payment network will eventually onboard large numbers of financial institutions. Under that thesis, banks using Ripple infrastructure could create sustained demand for $XRP as a bridge asset in cross-border settlements.

Viewed through that lens, the bank identifier document appears highly significant. If Ripple maintains routing identifiers for dozens of countries and financial institutions, some observers naturally assume those entities already participate in the network. Consequently, the adoption narrative develops quickly.

Why Investors Connected the Dots

Notably, the reasoning is not entirely irrational. Ripple has publicly announced real banking partnerships, signed payment agreements, and expanded infrastructure across several global markets over many years.

Therefore, the identifier list did not emerge in isolation. It reflects infrastructure built for genuine payment corridors and real-world operational use. However, it becomes problematic when observers confuse active commercial participation with technical reachability. Those are fundamentally different concepts.

The Missing Piece in Many Interpretations

What the bank identifier list cannot reveal is whether a specific institution actively uses Ripple’s platform, processes ODL transactions, or utilizes $XRP as a liquidity asset.

Instead, the document reflects addressability — the technical ability to route payments to those institutions if needed.

That distinction matters enormously. A logistics company may have the infrastructure to deliver packages to several addresses. However, it does not mean every address actively ships packages through that network every day.

Reading the List Through a More Accurate Lens

Once readers understand the operational purpose behind the identifiers, the document becomes easier to interpret realistically.

Network Access Versus Network Activity

The identifiers define reachable endpoints within Ripple’s infrastructure. They show where payments can potentially go. However, they do not show which institutions actively process payments through the network on a regular basis.

Modern payment infrastructure always maintains routing data that exceeds current transaction activity. Networks build ahead of demand so clients can access destinations when needed. Therefore, measuring network activity by counting routing endpoints would be like measuring highway traffic by counting highway exits.

Infrastructure Presence Versus Product Usage

Ripple operates several products. Notably, RippleNet functions primarily as a messaging and settlement layer, while Ripple Payments uses $XRP and RLUSD as a bridge asset.

An institution may appear within Ripple’s broader infrastructure without ever using $XRP directly. Even within the payment solution itself, inclusion in routing documentation does not automatically confirm active transaction activity or liquidity usage.

Visibility Versus Verification

Since the document appears within Ripple’s official materials, many observers treat it as verified proof of institutional adoption. While official documentation certainly carries more credibility than rumors, visibility still does not equal confirmation of commercial activity.

Investors seeking to evaluate Ripple’s true market penetration must rely on additional evidence such as partnership announcements, transaction volumes, quarterly reports, and independent blockchain analytics.

What the Records Actually Suggest About Ripple’s Global Footprint

Although the document cannot prove mass adoption, it still reveals meaningful information about Ripple’s operational strategy and infrastructure development.

Established Banking Corridors

The regions covered, including Asia, the EEA, and the UK, represent commercially important payment corridors with large remittance flows and strong demand for faster settlement infrastructure.

Europe-to-Vietnam remittance activity remains particularly significant due to Vietnamese diaspora communities across Germany, France, and other European markets. Ripple’s infrastructure presence in these regions aligns with a company pursuing valuable payment lanes rather than speculative expansion.

International Coverage Across Markets

The breadth of Ripple’s EEA coverage also stands out. Beyond major economies like Germany and France, the documentation includes smaller jurisdictions such as Malta, Monaco, and Iceland.

That level of regional completeness suggests Ripple designed its infrastructure for comprehensive operational coverage rather than selective market participation.

Signs of Long-Term Infrastructure Development

The institution-level detail within Vietnam’s banking system especially suggests sustained investment and long-term planning.

Building that kind of granular routing architecture requires local regulatory understanding, integration work, and deep familiarity with domestic banking networks. Consequently, the documentation reflects serious infrastructure development rather than superficial market exploration.

The Limits of What the Data Can Prove

Meanwhile, the identifier list leaves many critical questions unanswered.

What Remains Unconfirmed

The document does not confirm that the listed institutions have signed agreements with Ripple. Nor does it verify active use of Ripple Payments or $XRP liquidity services.

Additionally, the records provide no transaction volumes, revenue figures, or details about which institutions actively operate within Ripple’s ecosystem.

Questions the List Cannot Answer

The document does not reveal how many Vietnamese banks actively process Ripple transactions, what percentage of EEA institutions engage with Ripple infrastructure, or whether listed banks participate operationally beyond basic reachability.

While Ripple periodically discloses partnerships and network developments elsewhere, those answers do not exist within the routing documentation itself.

Why Context Matters More Than Headlines

In today’s information environment, headlines often prioritize engagement over context. As a result, claims such as “Ripple Connected to Over 500 Banks” may sound technically defensible while still creating misleading impressions.

The responsible approach requires understanding the purpose of technical documentation and resisting the temptation to equate infrastructure breadth with verified commercial adoption.

That approach produces a more balanced picture — one that acknowledges Ripple’s legitimate achievements without overstating them.

Final Thoughts on Ripple’s Banking Connections

Ripple has spent years building payment infrastructure across several important international corridors. The bank identifier list offers a genuine glimpse into that effort, revealing detailed routing architecture spanning Europe, the United Kingdom, and Asia.

However, the document does not prove mass $XRP adoption, confirm hundreds of active banking partnerships, or reveal large-scale transaction activity.

What it does demonstrate is operational seriousness. Ripple has clearly invested in detailed infrastructure capable of supporting real-world payment professionals across multiple jurisdictions.

That may sound less dramatic than many viral $XRP narratives. Yet it is also a more sustainable and defensible conclusion. The gap between what the evidence proves and what online speculation often claims should not diminish Ripple’s accomplishments. Instead, it should encourage investors and observers to evaluate those accomplishments carefully, and to seek stronger evidence where stronger claims are made.

Frequently Asked Questions

What is Ripple’s bank identifier list?

Ripple’s bank identifier list is part of the company’s technical documentation. The document provides numeric routing codes that can be used to identify destination institutions when configuring beneficiary payments through Ripple’s payment infrastructure.

Why are banks included in the list?

Banks appear because Ripple’s routing infrastructure needs standardized identifiers to direct payments accurately. Inclusion reflects payment reachability, not necessarily a commercial partnership.

Does the list confirm $XRP adoption?

No. The document does not confirm active $XRP usage, signed agreements, or institutional adoption. It only shows that Ripple’s infrastructure can theoretically route payments to those institutions.

How does Ripple use bank identifiers?

Ripple uses bank identifiers as routing references that connect payments to the correct settlement pathways, banking systems, and jurisdictions during cross-border transfers.

Why has the document become controversial?

Many $XRP investors interpreted the large number of listed institutions as proof of widespread banking adoption. However, that interpretation often confuses technical routing capability with verified commercial activity.