FinTech Geography. Who’s In The Vanguard?

As Bitnewstoday wrote earlier, the Policy Department of the European Parliament (Econ) published a report about competition in the field of FinTech, which certainly made the market players consider FinTech as the force to be reckoned with. Even if this force is currently at the very beginning of its development. In addition to the main topic and the particularly resonant thesis that Bitcoin and other cryptos are under threat from banking institutions, this study contains a lot of interesting statistics. A review of analytics and reports can lead to an important insight about the state and development of the FinTech companies worldwide. Let's try to draw conclusions where previously only numbers could be seen.

Mirror, mirror on the wall, who's the FinTech of them all?

According to the authors, the Crunchbase databases were involved in the analytics of the FinTech industry. But the problem was to determine the boundaries of the term “FinTech”. The formula "finance + technological development = FinTech" is still relevant, but it is incapable to express the completeness of the industry. Econ specialists took the most out of every category — everything that can be applied to the industry, and compiled a database of almost 4000 companies which were thoroughly studied.

Breakdown by countries has shown which is the “alpha”. USA world leadership is almost indisputable: 1500 startups come from the States, indicating that there are headquarters of nearly 40% of all FinTech companies.

However, something is wrong even in the USA. Thus, in 2017, the number of funding rounds in American companies dropped sharply. If in 2016 this number was 398, then in 2017 — only 298. Are companies trying to escape from the USA? Hardly that. The same statistics reveal that large US corporations and management companies are interested in acquisition: takeover and startup migration to the US is at the highest level. Startups also leave for the EU but to a much lesser extent.

Europe is in the “underdog” role

The fact is that the decrease in the number of funding rounds is observed not only in the USA. In 2017, this indicator grew only in the EU countries, which demonstrated exceptionally positive dynamics for the last 20 years. It was about 245 that is still smaller than in the US.

The top performer in terms of startup numbers in the Old World is the United Kingdom — 454 FinTech companies. This is quite understandable. According to the E&Y survey, the UK is considered to have the most friendly legal framework to FinTech, making it look lucrative for business. Add a “sandbox”, a way for companies to test products with temporary regulatory approval, and you’ll understand why Britain is the undisputed leader in Europe by the number of FinTech startups based on its territory. The next leaders are Spain (100) and Germany (90). It is curious that the US and the EU have been competing by every measure since 1997, while other world countries experienced a real but unsustainable FinTech boom only in 2014. Though, it didn’t last long.

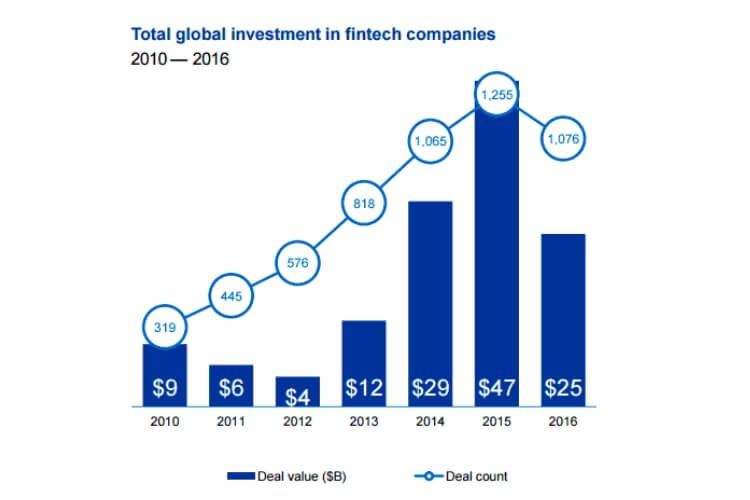

Investors would like to see the sustainable industry

Turning to the decline in investment prospects, the problem is obvious. It is more than just the number of funding rounds, but the real amount of investments attracted to the financial technologies. Even 2016 demonstrated a decrease in investors’ interest in the industry.

Source: Pulse of Fintech Q4'16, Global Analysis of Investment in Fintech, KPMG International

Right from 2014, the banking sphere started to feel the threat coming from FinTech companies. Earlier, in the eyes of business sharks, this was seen as a “sandbox” indeed, but by that time the banks understood the power of the opponent.

Those five stages of grief

It all looks like the Kübler-Ross model: firstly the banking institutes denied the new players, then the anger came. Probably, this was the time when investors were worried about facing the new frontiers, and the markets stood still. The bargaining followed, when the traditional players understood the opportunities and started adapting, acquiring the startups or bringing up their own. The bargaining continues, it is the right time to name the prices. USA and EU acknowledge that, harnessing the power of FinTech companies. “Depression and acceptance” is not so long away. FinTech needs to catch some breath for a new rally.

The developing markets would become a new driving force, but this is the story for our next article.