Credit Scoring: Traditions vs New Technologies

Credit scoring or simply scoring is the concept which is probably known to every adult, even to those who have never heard such words. Scoring system is the system used by credit organizations to calculate the creditworthiness of a potential borrower is a scoring system. Credit scoring is the process during which a person who applies for a loan receives an assessment of his financial status.

Blot on the biography

In developed countries, such as the USA or Germany, points calculated by national scoring systems have become a very important social indicator.

The loss of even a few points of a credit rating becomes almost a personal tragedy for a person and instantly leads to a decrease in the status and availability of banking and other services. A high credit score is the evidence of success, well-being and confidence in the future.

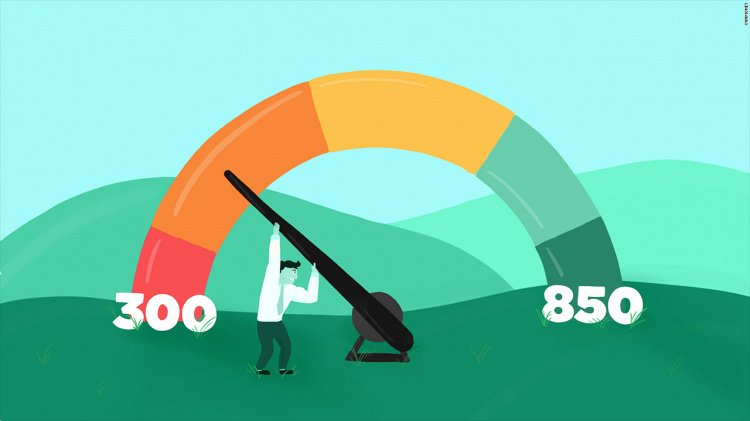

Traditional scoring systems

In some countries, there is no complex parameter to assess creditworthiness. As a rule, it is replaced by services of the “blacklists” of borrowers. They are registries with the data on non-fulfilment of obligations, delayed payments and other problems regarding credit organizations. Austria is a good example of such a country.

A more common approach is presented in countries such as India and the USA: the number of points is calculated using a rather complex mathematical model, different parameters of a citizen’s financial profile are used, historical data become the basis for predicting future creditworthiness. A final result is a three-digit number assigned to a citizen. Credit institutions use this rating to evaluate potential customers and calculate the risk when dealing with them.

FICO is the most famous and popular among organizations that offer self-developed credit scoring models. FICO products are several types of calculating systems, for example, for the automotive market or for mortgage loans. There is also a universal scoring from FICO. The credit institution decides which one to choose, and the number of calculated points will be slightly different as a result.

FICO credit rating is calculated in the range from 300 to 900 points, where 300 is the lowest score and 900 is the highest. The scale looks like this:

- 300-579 points — is the worst rating. Lenders are likely to refuse to provide a loan or the interest rate will be very high;

- 580-669 — not a very high rating, but creditors will seem to be very supportive and probably without refusals;

- 670-739 — good credit rating and the borrower can count on the standard interest rate;

- 740-799 — very good credit rating, most likely, bonuses and favorable conditions will be provided;

- 800-855 — excellent credit rating, so you can foot open the office door, drink coffee together with the bank director and get a personal badge “customer of the year”.

People off the board

Traditional banking scoring systems all around the world exclude bad borrowers — individuals with no credit history or bad loans in the past. As a result, an impressive number of people who still have a need for loan funds are outside the “coverage area” of banking services.

However, desire will not help to earn money on people with low credit ratings. Even if the traditional scoring system doesn’t work with them, some method of assessment is still needed. At this very moment, great and powerful robots with inhuman intelligence come to the fore: they analyze the data of borrowers, take over the world and begin to rule people. Almost true.

Non-obvious dependences

The emergence and development of credit scoring systems with artificial intelligence were preceded by two things: first, it was noted that the tendency of borrowers to pay on time or to skip payment terms may have an unobvious connection with data that were not previously taken into account. For example, with the kinds of goods that a person buys or with the way he prefers to spend his free time.

The second thing is the progress in computer technology, which gave the world relatively inexpensive high-power computing systems, storage systems and computer networks. With the emergence of available computing resources, artificial intelligence systems and machine learning, in particular, began to develop rapidly.

Do you want a loan? Show your posts on Facebook

So, entrepreneurs and developers know that a potential borrower can be assessed not only by credit history but also by other parameters. What data about the client can be used?

Progress and development of technologies turned out to be very useful: social networks, online services, online stores and payment systems store huge amounts of data — modern people leave a well-read and deeply individual digital mark on the Internet.

To solve the problem, you simply need to take these data (most of which do not even require user permission — information, for example, such as profiles in social networks, is publicly available) and uploaded to the input of machine learning.

To find the links between a borrower's digital footprint and its creditworthiness in an accurate way, a computer intelligent system needs to have a learning process. This is not so difficult: you need to take historical data of customers who have already taken loans and paid on them (and did not pay, of course), download them all the system along with additional data of social activity on the Internet and make a setup.

Pros and cons of scoring with machine learning

The advantages of using smart machines to assess borrowers are obvious: the ability of powerful computers to find links in large volumes of information and analyze data is inaccessible to humans. The speed of processing requests and scoring points necessary for the full functioning of modern, often automatic services can only be provided by computers.

Another advantage of using complex computing systems is that the machines are deprived of the human factor, they cannot make biased decisions because of cognitive distortions, fatigue, stress, etc. This means that where a computer system is used, the percentage of lost “good” clients will decrease and the share of unjustifiably high marks that cause loss of money issued to “bad” borrowers will also fall.

There is also a downside to the use of “too intelligent” scoring systems. In many cases, the process of calculating customer ratings and the subsequent decision isn’t transparent: the links between the different data that the machine found are left inside it and they are not understandable to humans.

Artificial intelligence experts call this phenomenon a “black box” problem. From an ethical, and from a practical point of view, it is impossible to create a situation in which the computer system user has no idea what influences the result of her work. Moreover, in such a sensitive area as finances and the decision of the borrower's fate where the need to receive loan funds is definitely an important event in the life of any person.

Image courtesy of Analytics Magazine