Ultimate Blockchain Solutions for Ecommerce Startups

An eCommerce has seen its fair share of changes in the recent decade. For example, innovations in shipment and customer support were quite impactful and changed the way companies do businesses. However, none of the innovations and changes made within this timeframe had the potential to transform the entire industry forever. This innovation, of course, is blockchain.

The technology has the potential to make eCommerce easier and safer by introducing unmatched cost reductions in payments, eliminating inefficiencies in the supply chain, reducing fraud, and unlocking many other benefits.

One question that people often ask blockchain experts when talking about the impact of technology on eCommerce: “Why don’t we hear eCommerce businesses announcing their blockchain projects if the technology has so much potential for the industry?”

There are two great answers to this reasonable question. First and foremost, many eCommerce companies are quietly working on a bunch of blockchain-related projects to obtain a competitive advantage, so they don’t go around broadcasting the news about that.

Second, we already know about many such projects. Amazon, for example, has recently launched its own blockchain service for creating and managing scalable blockchain networks with open-source frameworks. Also, they’ve announced a partnership with a startup called Kaleido to make the usage of blockchain easier for their customers.

1. Improved Payment Methods

Online payments are a common target for cyber criminals, so the news about malware and online fraud are something that we’re used to seeing these days. For example, one of the latest news that shocked the world was revealed last year; apparently, malware that was built inside a battery optimization app could steal money from PayPal accounts. Those protected by two-factor authentication were reported to be at risk, too.

Online transactions are at huge risk of fraud as well, so finding new, more effective ways to provide secure payments is a significant concern for many companies. Besides, reports say that 4 out of 5 online consumers consider the protection of data a top priority.

So, adopting blockchain technology for payments could be a good way for startups to improve customer satisfaction as well as the security of online transactions.

2. Eliminating Middlemen from Online Transactions

As I’ve described in the previous section, a customer authorizes the transfer of cryptocurrencies from their wallet to a seller’s wallet easily with a couple of clicks. This means that there are no banks and other financial institutions are involved, so the two won’t have to pay fees and commissions for the transaction.

In fact, Satoshi NAKAMOTO, the creator of Bitcoin, saw cutting middlemen as one of the biggest promises of the cryptocurrency.

“[Bitcoin is] A purely peer-to-peer version of electronic cash [that] would allow online payments to be sent directly from one party to another without going through a financial institution,”

— he wrote in this white paper on bitcoin.org.

3. Take Advantage of Decentralized Apps

Decentralized apps (dApps) are the apps that lack a centralized server owned by an app store of a third-party company. This is the most important difference that sets DApps from traditional apps in the backend (the front end in both types is actually very similar).

“A startup can benefit from having a DApp since all data, including all financial transactions, are stored using blockchain,” says Ben MONCRIEF, a blockchain researcher from Grab My Essay:

“This means that no other parties will be able to change or remove any information and/or data from the app; moreover, it also eliminates the need for a third party managing and hosting the app.”

4. Simplify Order Fulfillment Process

By using a blockchain-powered eCommerce website, you can get a complete visibility of your order fulfillment process, as each block with an order connects to the previous one. As a result, the chain of orders allows you to monitor the performance of your business.

For example, if a customer makes a purchase from your website, they initiate a process in the blockchain system. Here’s how that process would look like:

-

Block #1: order placement. This act initiates the process by creating the first block in the system.

-

Block #2: payment processing. The action creates a block that proves the transaction for the business.

-

Block #3: order fulfillment. The business reviews the previous two blocks and ships the product bought by the customer; the system creates a block proving that this action was completed.

-

Block #4: shipping to the customer. The last block indicates that the product was shipped, so the order was completed by the business.

Each block comes with the time of initiation and completion, so you can monitor when a certain action was performed. As a result, the entire process of order fulfillment becomes fully transparent, which, in turn, increases accountability and trust between your business and customers.

5. Improve Contract Enforcement with Smart Contracts

Blockchain is a tool that supports a more effective business process fulfillment with smart contracts. Simply defined, these are a collection of software codes with components created to automate contract execution and settlement. As a result, businesses can manage transactions in an automated, pre-programmed way.

Here’s the process that makes start contracts possible:

-

The terms and conditions of a contract are written in the form of a computer code

-

The code is stored and replicated on the blockchain

-

The code is executed and implemented by computers running the blockchain

-

The code is updated according to the terms (e.g., a party makes a payment for products).

Where can your startup use smart contracts? They can enable you to exchange money, or basically anything of value in a conflict-free, transparent way while avoiding the involvement of middlemen.

For example:

-

A party to the smart contract — the buyer — is entitled to paying a certain amount of cryptocurrency if the conditions are met

-

The two parties agree on the conditions and execution terms (“If this, then that”)

-

The decentralized blockchain network utilizes the contract code to determine if the conditions are met; if they are, the payment is conducted automatically

-

The seller receives the payment.

So, a business involved in the development of smart contracts can define specific events and terms required to complete business operations. This, in combination with legal contract templates, can improve the execution of B2B contracts and other business processes that your business needs to be completed. To protect the document from hackers, encryption can be used.

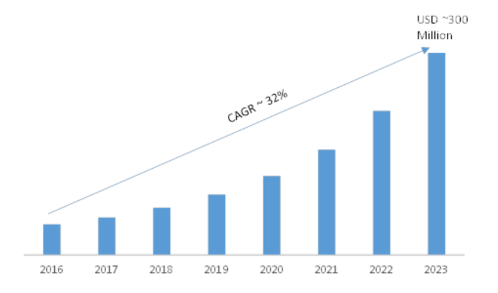

A lot of businesses are considering using smart contracts or already taking advantage of the technology. According to Market Research Future report, the global smart contracts market is projected to reach about $300 million with a compound annual growth rate of 32 percent during the forecasted period from 2017 to 2023.

Credit: Market Research Future

Clearly, smart contracts have the potential to increase efficiency and transparency in the legal industry, and help companies to get their contracts completed properly.

Wrapping Up

Undoubtedly, blockchain opens a number of new, exciting opportunities for startups, with the above ones being some of the most impacting on the list. With more and more businesses realizing the advantages of using blockchain-enabled technologies in eCommerce, it makes perfect sense to see how they can give you a competitive advantage.

Hopefully, this guide was a good introduction to the world of blockchain for you and inspired you to explore how you can achieve higher transparency, security, credibility, and cost-effectiveness and advance your business in an innovative way.

About the Author:

Dorian Martin is a frequent blogger and an article contributor to a number of websites related to digital marketing, AI/ML, blockchain, data science and all things digital. He is a senior writer at Supreme Dissertations, runs a personal blog NotBusinessAsUsusal and provides training to other content writers.