download

downloadA recent report by Moody’s Investors Service reveals that it is still the monetary policies of central banks that are the main market movers in this historical period.

More aggressive monetary policies move the market strings

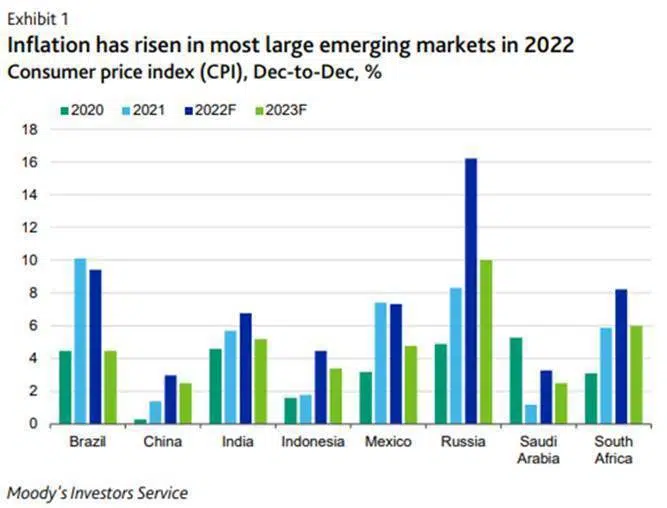

The report says that due to accelerating inflation in many G-20 emerging markets, central banks will continue to raise interest rates despite the fragile economic recovery, especially in those countries that are still early in the cycle of increasing rates, or that have not begun yet.

This process is now underway almost everywhere in the G-20, and will still go on at least through the remainder of 2022.

However, the impact of rising inflation and monetary tightening on the banking sector is still not entirely clear, with two opposing effects.

On the one hand, higher rates produce more net interest margins, thus increasing banks’ profitability. But, at the same time, higher rates lead to slower economic growth, and thus higher burdens on borrowers, resulting in weaker loan quality and higher credit costs.

The report points out that in 9 of the 10 G-20 emerging markets, bank margins have historically increased with rising inflation. Thus Moody’s predicts that in India, Saudi Arabia, and South Africa banks will see their margins increase in 2022-2023. In contrast, in Brazil and Turkey such increases will be less significant, should inflation go above expectations.

The effects of inflation and rising rates on the economy

This does not detract from the fact that credit costs will also rise, as has happened historically in 7 of the 10 countries. In particular, Moody’s expects the greatest increases from this point of view in Russia and Turkey, but also in Argentina, South Africa and Brazil, should inflation go above expectations.

In such a scenario, if inflation rises sharply the disadvantages would eventually outweigh the benefits for the banking sector.

However, Moody’s also expects inflationary pressures to fall in all 10 markets in 2023.

So while there is a risk that tight monetary policies will create further problems, much will depend on how inflation rates evolve. If, as Moody’s predicts, they will peak this year and from next year start to fall, then it is possible that the banking sector will even end up benefiting. Otherwise, the disadvantages will outweigh the advantages.