Here’s what you need to know about reporting crypto on your 2024 taxes:

- The IRS treats crypto as property, not currency

- You must report all crypto transactions, even small ones

- Taxable events include selling, trading, and using crypto to buy goods

- Use Form 8949 to report crypto gains/losses

- Report crypto income on Schedule 1 or Schedule C

Key steps for crypto tax reporting:

- Gather all transaction records

- Calculate gains/losses for each transaction

- Fill out Form 8949 and Schedule D

- Report any crypto income

- Answer the digital asset question on Form 1040

Common pitfalls to avoid:

- Not reporting all transactions

- Incorrect cost basis calculations

- Misclassifying transaction types

Use crypto tax software to simplify reporting. Stay updated on IRS rule changes for 2024, including new reporting requirements for exchanges.

Transaction types and their tax treatment

- Buying crypto: not taxable.

- Selling crypto: subject to capital gain or loss.

- Trading crypto: subject to capital gain or loss.

- Receiving as payment: treated as regular income.

- Mining rewards: treated as regular income.

When in doubt, consult a tax professional familiar with crypto regulations.

Basics of crypto taxation

Understanding how cryptocurrencies are taxed is key for anyone using digital assets. The IRS has rules for taxing crypto, and knowing these rules helps you follow the law and avoid penalties.

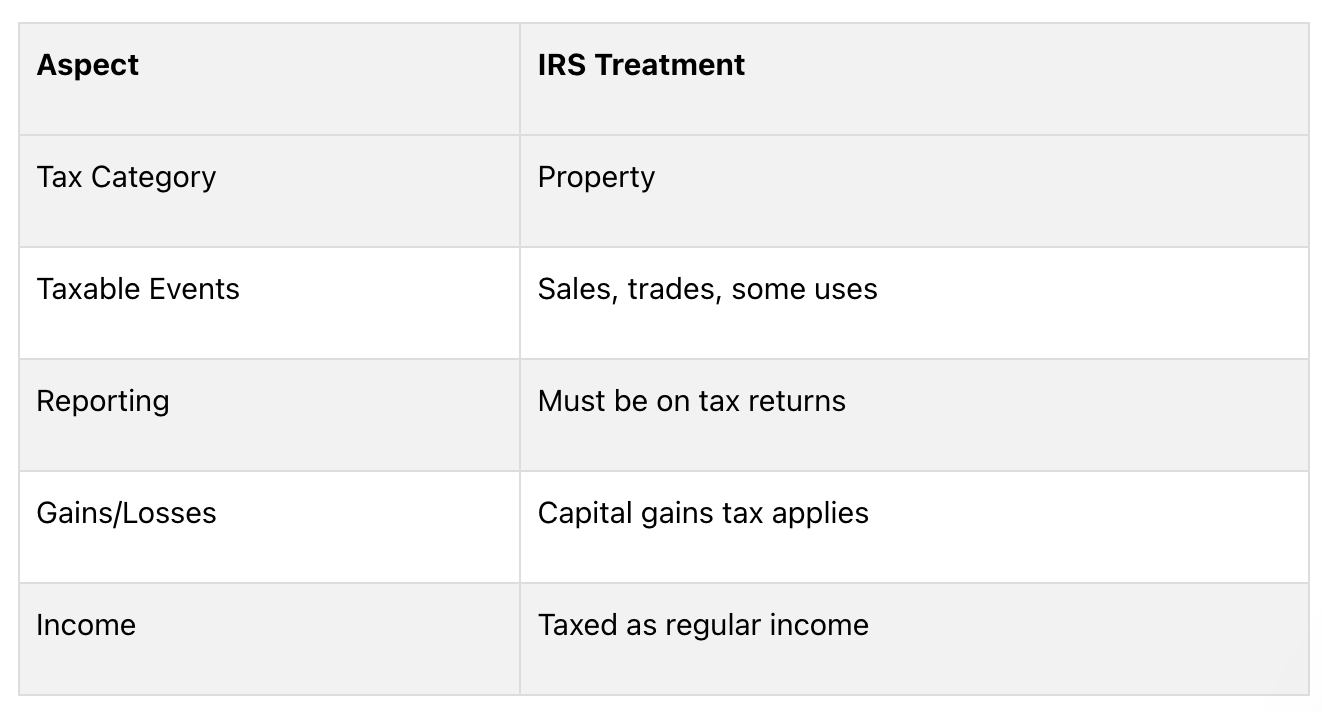

How the IRS views crypto

The IRS treats crypto as property, not money. This affects how they’re taxed:

Because tokens are property, the IRS uses the same tax rules for them as for other property. This means you need to report any gains or losses from crypto on your taxes.

Taxable vs. non-taxable events

Knowing which crypto activities are taxable is important for correct reporting. Here’s a simple breakdown:

Taxable events

- Selling crypto for regular money

- Trading one token for another

- Buying things with crypto

- Getting paid in crypto

- Mining crypto

- Receiving staking rewards

- Receiving airdrops or hard forks

Non-taxable events

- Buying crypto with regular money

- Moving tokens between your own wallets

- Donating crypto to approved charities

- Gifting crypto (note: gift tax rules may apply)

Even for non-taxable events, keep records. They might affect your taxes later.

Getting ready for tax reporting

Preparing for crypto tax reporting requires good organization. By gathering the right documents and keeping good records, you can make the process easier and follow IRS rules.

Collecting required documents

To report your crypto transactions correctly, you’ll need these documents:

Document type and descriptions

- Exchange Statements: records of all your trades.

- Form 1099-B: shows money from sales (provided by some platforms).

- Wallet Addresses: list of all wallets you used.

- Purchase Receipts: records of when you bought crypto.

- Sale Records: records of when you sold crypto.

- Fee Information: details of trading and network fees.

Get these documents well before taxes are due so you have time to report correctly.

Keeping track of transactions

Good record-keeping is key for accurate tax reporting. Here’s what to do:

1. Use a crypto transaction journal: keep a detailed log with:

- Date of each transaction

- Type of token

- Amount traded or moved

- Value in US dollars at the time

- Why you made the transaction (trade, buy, sell)

- Fees you paid

2. Use tax software: think about using special crypto tax software to help you. It can:

- Bring in transactions from different exchanges and wallets

- Figure out your gains and losses

- Make tax forms for you

3. Sort your transactions: group your transactions by how long you held the crypto:

- Short-term: Held for less than a year

- Long-term: Held for more than a year

4. Record non-taxable events: even if some crypto activities aren’t taxed, keep records of:

- Moving crypto between your own wallets

- Buying crypto with regular money

- Giving crypto as gifts (gift tax rules might apply)

How to Report Crypto on Your Taxes

Reporting crypto on your taxes can be tricky. Here’s a step-by-step guide for the 2024 tax season:

Figuring Out Gains and Losses

To report your crypto transactions correctly:

- Find the cost basis for each transaction

- Calculate how much you got from each sale or trade

- Subtract the cost basis from what you got to find your gain or loss

Remember:

- Short-term: Held less than a year (taxed like regular income)

- Long-term: Held more than a year (lower tax rates apply)

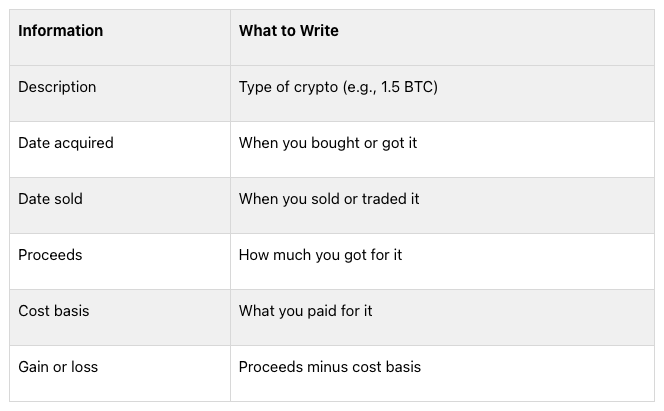

Filling Out Form 8949

Form 8949 is key for reporting crypto transactions:

- Use separate forms for short-term and long-term transactions

- Fill in the top part, checking box (c) for crypto

- For each transaction, include:

Tip: List your transactions in date order to make it easier.

Using Schedule D

After Form 8949, move the totals to Schedule D:

- Put short-term transactions in Part I

- Put long-term transactions in Part II

- Add up your total gain or loss on Line 16

If you lost money on crypto in past years, include that on Schedule D too.

Reporting Crypto Income

For crypto income not from buying and selling:

- Use Schedule 1 of Form 1040 for most crypto income (like mining or staking)

- If you work for yourself, use Schedule C

- Report the value of crypto you got as payment on the day you received it

Don’t forget to answer “Yes” to the digital asset question on Form 1040 if you did anything with crypto during the year.

Special Cases in Crypto Taxes

Crypto-to-Crypto Trades

When you swap one token for another, it’s a taxable event. Here’s what to do:

- Find the market value of the crypto you’re trading when you make the swap

- Figure out the difference between what you paid for the crypto and its current value

- Report this difference as a gain or loss on Form 8949

Note: You must report these trades even if you don’t change your crypto to regular money.

Airdrops and Hard Forks

Airdrops and hard forks can lead to unexpected taxes:

Event and Tax Treatment

- Airdrops: taxed as regular income.

- Hard forks: new tokens usually taxed as regular income.

New tokens usually taxed as regular income

For both, use the value of the tokens when you get them or can use them. Report this on Schedule 1 of Form 1040.

Lost or Stolen Crypto

Dealing with lost or stolen crypto is tricky for taxes:

Situation and Tax Treatment

- Lost crypto: usually can’t be deducted.

- Stolen crypto: not tax-deductible for individuals in 2024.

However, you might have some options:

1. Abandonment Loss:

- Might be the best choice for taxpayers

- You need proof that you meant to abandon the crypto and took action to do so

2. Exchange Shutdowns or Scams:

- Reporting losses on Form 8949 is risky

- Talk to a CPA before you decide what to do

3. Bankruptcy Cases:

- You might get a tax deduction once you know how much you’ll get back

- The deduction is what you paid minus what you get back

- It’s usually treated as a regular loss, not a capital loss

Common Mistakes and How to Avoid Them

When dealing with crypto taxes, many people make mistakes. Here are some common errors and ways to avoid them:

Not Reporting All Transactions

Some crypto owners think they only need to report big transactions. This is wrong. The IRS wants you to report all crypto transactions, no matter how small. Not doing this can cause problems:

Problem and How to Avoid It

- IRS audits: keep records of all transactions.

- Fines: use software to track all crypto activities.

- Extra charges: report even small transactions under $600.

- Possible legal issues: know the latest IRS rules.

The IRS has ways to find unreported crypto transactions. It’s important to report all your crypto activities correctly to stay out of trouble.

Wrong Cost Basis Calculations

Getting the cost basis wrong can change how much tax you owe. Common mistakes include:

- Getting the purchase date wrong

- Forgetting about fees

- Not counting previous trades

To avoid these errors, use crypto tax software. It can figure out the cost basis and keep track of your transactions for you.

Misclassifying Transactions

It’s important to label your crypto transactions correctly for taxes. Here’s a simple guide:

What You Did and How It’s Taxed

- Traded crypto for money: capital gain/loss.

- Traded one crypto for another: capital gain/loss.

- Earned crypto as pay: regular income.

- Got crypto from mining: regular income.

- Got crypto from staking: probably regular income (ask a tax expert).

To get this right:

- Write down why you made each transaction

- Use software to sort your transactions

- If you’re not sure, ask a crypto tax expert

Tools for Crypto Tax Reporting

Reporting crypto taxes can be hard, but there are tools to help. Let’s look at some useful software and IRS resources.

Crypto Tax Software

Crypto tax software can make reporting easier. Here are some popular options:

Software and What It Does

- CoinTracker: tracks wallets, updates portfolio.

- Best for: people who want to see all their crypto in one place.

- TurboTax Premium: files full tax return, offers expert help.

- Best for: people with complex taxes.

- CoinTracking: helps with international tax laws.

- Best for: people who need guidance on different countries’ rules.

- TokenTax: calculates gains/losses automatically.

- Best for: people who want simple reporting.

When picking software, think about:

- How many transactions you have

- Which exchanges you use

- If you need extra features like tax loss harvesting

IRS Resources

The IRS also has tools to help with crypto taxes:

1. Virtual Currency Guidance: Official rules on how to treat crypto for taxes

2. Form 8949: Use this to report crypto gains and losses

3. Schedule D: Use with Form 8949 to show total gains and losses

4. FAQ on Virtual Currency: Answers common questions about crypto taxes

5. Publication 544: General info on selling assets, which can apply to crypto

These resources can help you understand the official rules and fill out your forms correctly.

Keeping Up with Tax Rules

Knowing the latest crypto tax rules is key for correct reporting. The IRS often changes its rules for digital assets, so taxpayers need to stay informed.

2024 IRS Rule Changes

Here are the main updates for the 2024 tax year:

- New Form: The IRS has a draft of Form 1099-DA for digital asset transactions.

- Exchange Reporting: Starting in 2023, crypto platforms must report transactions to the IRS and users.

- $10,000 Rule: Businesses don’t need to report crypto transactions over $10,000 until new rules come out.

- Tax Rates: New rates for 2024 affect how crypto gains are taxed.

- NFT Rules: The IRS now treats NFTs as collectibles for taxes.

What’s Next

As crypto grows, tax rules will change. Here’s what to watch for:

1. More Checks: The IRS has hired crypto experts to look closer at tax reports.

2. New Laws: Keep an eye on proposed rules about crypto mining taxes and wash sales.

3. DeFi Rules: The IRS is working on how to tax decentralized finance trades.

4. Global Rules: Expect more teamwork between countries on crypto taxes.

To stay up-to-date:

- Check the IRS website often

- Use good crypto tax software

- Talk to a tax expert who knows about crypto

- Join online groups that talk about crypto taxes

Conclusion

Reporting crypto taxes correctly is important. This guide has shown you how to do it right and why it matters.

Main Points to Remember

- Report all crypto activities on the right IRS forms

- Use crypto tax software to make reporting easier

- Keep up with new crypto tax rules

- Keep good records of all your crypto activities

- Watch out for common mistakes like missing transactions or wrong calculations

If you’re not sure about your situation, it’s best to ask a tax expert for help.