Quantinuum, the quantum computing company majority-owned by Honeywell, has filed to go public in what would be the sector’s first major traditional IPO. The company is looking to raise up to approximately $1.05 billion through a Nasdaq listing under the ticker “QNT.”

The numbers behind the filing

Quantinuum submitted its Form S-1 registration statement to the SEC on approximately May 8, 2026. The company is targeting a valuation exceeding $20 billion, a figure that would represent a meaningful jump from its most recent private market pricing.

That last private round closed in September 2025, when Quantinuum raised $600 million at a $10 billion pre-money valuation. So the IPO is essentially asking public market investors to pay a premium of more than 2x what private backers paid less than a year ago.

J.P. Morgan and Morgan Stanley are running point as joint lead book-running managers.

Total capital raised since inception now sits at roughly $1.5 billion across multiple funding rounds. Before the September 2025 raise, Quantinuum pulled in $300 million in January 2024 at a $5 billion pre-money valuation. In other words, the company’s perceived value has quadrupled in roughly two years.

From lab merger to IPO candidate

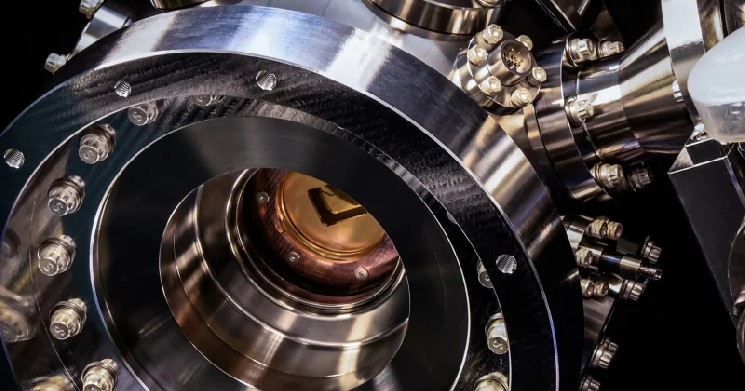

Quantinuum came into existence in late 2021 through the merger of Honeywell Quantum Solutions and Cambridge Quantum Computing. The combination married Honeywell’s trapped-ion quantum hardware with Cambridge Quantum’s software and algorithm capabilities.

The company has also invested in post-quantum cryptography and quantum-secure technologies. These are defensive tools designed to protect data from future quantum computers powerful enough to crack today’s encryption.

The path from confidential draft submission in February 2026 to formal S-1 filing in May suggests the company and its advisors moved relatively quickly once they decided the market window looked favorable. That three-month turnaround from confidential to public filing is brisk by IPO standards.

What this means for investors

Quantinuum’s decision to pursue a traditional IPO rather than a SPAC is itself a statement. It suggests the company believes it can withstand the scrutiny of a conventional roadshow, where institutional investors ask pointed questions about revenue, burn rate, and the timeline to profitability. SPAC mergers allowed companies to lean heavily on forward-looking projections. A traditional IPO demands more substance.

The jump from $10 billion to $20 billion-plus in under a year will raise eyebrows. Private-to-public valuation step-ups of this magnitude aren’t unusual in hot sectors, but they do shift the risk profile. Public market investors would be paying a significant premium over sophisticated private investors who had access to the same data just months earlier.