Happy Thursday, advisors!

In today’s newsletter, David Lawant, head of research at Anchorage Digital reviews crypto’s evolving role in 401(k)s, as regulatory clarity is poised to open up investments.

Then, in Ask an Expert, Kevin Tam answers questions about crypto adoption around the world looking at the recent 13F filings.

Happy Reading.

Modernizing the nest egg: the past, present, and future of crypto in 401(k) plans

The United States retirement system is about to reach a structural inflection point. For over a decade, the $10 trillion 401(k) market remained insulated from crypto assets due to regulatory ambiguity and litigation concerns. However, a decisive shift in federal policy is transforming 2026 into the year of integration, which in the long term will move crypto from the periphery into the institutional core of the American retirement system.

The regulatory shift from “extreme care,” to “principled neutrality,” to "democratizing access."

The Department of Labor (DOL) is responsible for making sure that ERISA, the 1974 federal law that sets minimum standards for most voluntarily established retirement and health plans in private industry, is at the epicenter of this issue. In March 2022, it issued Compliance Assistance Release No. 2022-01. This release created a de facto ban on crypto assets in retirement plans by mandating that fiduciaries exercise “extreme care” and threatening targeted investigations for those engaging with crypto assets.

On May 28, 2025, the DOL formally abandoned the “extreme care” standard with the Compliance Assistance Release No. 2025-01. This release formally rescinded the restrictive 2022 guidance, stating that the previous stance had “deviated from the requirements of ERISA” and the department's “historically neutral, principled-based approach”. The rescission re-established the legal standard set by the Supreme Court which holds that fiduciaries must act prudently based on a contextual evaluation of risk and return, rather than adhering to categorical bans on specific asset classes.

But the real catalyst came with President Donald Trump’s Executive Order 14330, signed on August 7, 2025. Titled “Democratizing Access to Alternative Assets for 401(k) Investors,” this directive fundamentally redefined the government’s stance, shifting from a cautionary tone to an affirmative mandate for facilitating access to “alternative assets,” which the order explicitly defined to include crypto assets among more established classes such as private equity and real estate.

Upcoming DOL guidance on alternative assets and what adoption could look like

This past January, the DOL submitted a proposed rule that would clarify its position on alternative assets and the appropriate fiduciary process. The document is not public yet and is still sitting with the Office of Management and Budget (OMB), but given that the 180-day White House deadline has already expired, there is expectation that it could be released for public comment quite soon.

For crypto specifically, attention hinges on the design of the upcoming fiduciary safe harbor. This regulatory ‘’checklist’ is intended to immunize fiduciaries from liability for investment losses, provided specific standards are met. Its critical pillars are expected to include qualified custody requirements, liquidity constraints and portfolio allocation caps.

Even after the major regulatory hurdle is cleared, however, broad adoption will likely unfold more akin to a glacial shift over several years than like a speculative spark.

The evolution from high-friction Self-Directed Brokerage Accounts (SDBAs) toward seamless inclusion in core menus and Target Date Funds relies on myriad critical factors, including fiduciary buy-in and platform compatibility. Investment consultants like Mercer, Aon and Willis Towers Watson serve as critical gatekeepers, and although they tend to move cautiously, allocation to alternatives is emerging as a top-of-mind issue. Simultaneously, the industry must bridge the gap between legacy 'mutual fund plumbing' and digital asset infrastructure to ensure 401(k) platforms can seamlessly handle the new asset class.

Still, the 401(k) market is critical not only due to its sheer size but also because of its unique flow profile acts as a mechanical volatility dampener. Because retirement participants are price-inelastic, their bi-weekly, non-discretionary payroll contributions provide a stabilizing bid that persists regardless of short-term market sentiment. This effect is reinforced by managed accounts and target-date funds (TDFs), which institutionalize “buying the dip” by automatically purchasing assets during market corrections to restore target weights.

Unlike the high-velocity debut of spot exchange-traded funds (ETFs), the move into retirement accounts will likely be an accumulating wave that will build over years. Yet the sheer size and unique stability of this investor base make 2026 the year crypto’s role in the American nest egg became an undeniable, permanent fixture.

- David Lawant, head of research, Anchorage Digital

Ask an Expert

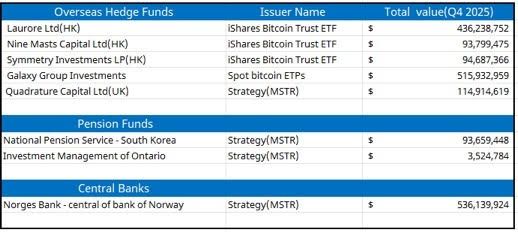

Q: What do Norges Bank and overseas hedge funds have in common?

Overseas hedge funds from Hong Kong and the UK are showing a massive appetite for regulated exposure, heavily accumulating spot bitcoin ETFs to build their portfolios. Laurore Ltd. has newly emerged with a 100% portfolio concentration IBIT.

In Pension fund growth, South Korea’s National Pension Service increased its MSTR exposure to $93.6 million, far outpacing the $3.5 million position held by Investment Management of Ontario (IMCO).

In Q4, the Central Bank of Norway opened a new position of MSTR valued at $536 million.

Q: Is Canada’s bitcoin bet starting to cool off?

National Bank of Canada cut its stake in MSTR by 51% in Q4 2025, reducing shares simultaneously with the stock’s price drop. The bank’s position dropped from $659 million to $152 million in this quarter. Notably, the bank also holds $52.4 million in put options on MSTR.

Q: What does the global regulator roadmap tell us about bitcoin’s trajectory into 2026 and beyond?

The direction is towards legalization. Regulatory timelines show a coordinated global build-out with MiCAR implemented across the EU in June 2025, the GENUIS Act signed in the US in July 2025, and HK, Singapore andthe UAE all establishing formal digital asset frameworks. Looking further, Canadian Securities Administrators are expected to propose amendments enabling broader tokenization of securities and ETFs in Q4 2026.

Driven by regulatory clarity and the continued adoption of digital asset ETFs, institutional investors view them as strategic assets for diversification and long-term growth.

- Kevin Tam, digital asset research specialist

Keep Reading

- Bed Bath and Beyond enters the blockchain space with the acquisition of Tokens.com.

- Trading platform Crypto.com receives conditional approval for a U.S. banking license.

- Meta re-enters the stablecoin conversation with plans to launch its coin later this year.