This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

Something very interesting showed up in the FOMC November meeting minutes this week that had nothing to do with rate cut expectations.

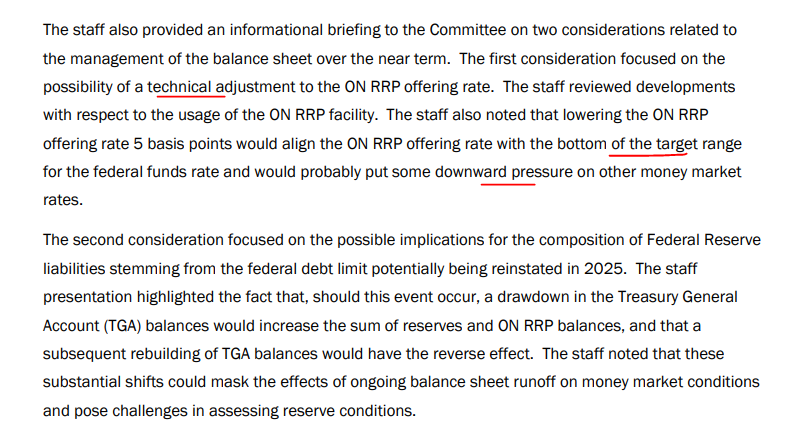

Hidden deep in the minutes was the following excerpt:

Essentially, the Fed is considering lowering the award rate on Reverse Repo Facility assets by 5-basis points, which would lower the bottom of the target range of the federal funds rate band.

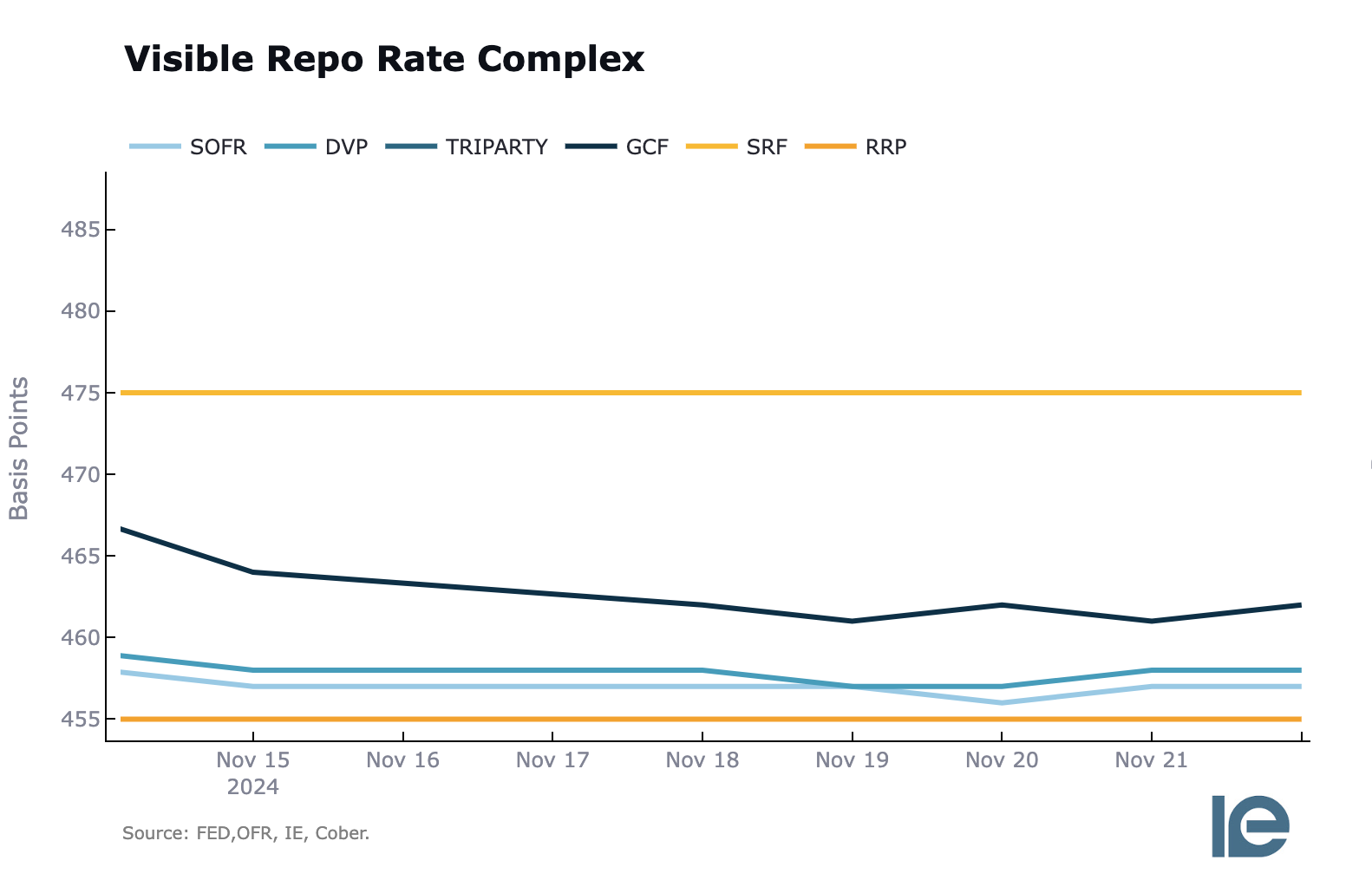

Here is what that complex looks like visually:

One can only speculate as to why the FOMC wants to lower this rate, but there’s a convincing theory:

Given the recent uptake in the Standing Repo Facility that occurred at the end of the previous quarter, paired with FOMC members acknowledging that the clock is ticking on how much longer QT can continue without potential strain showing up in the monetary plumbing system, the FOMC might be trying to get ahead of this by encouraging outflows from the RRP and increasing bank reserves to provide ample liquidity.

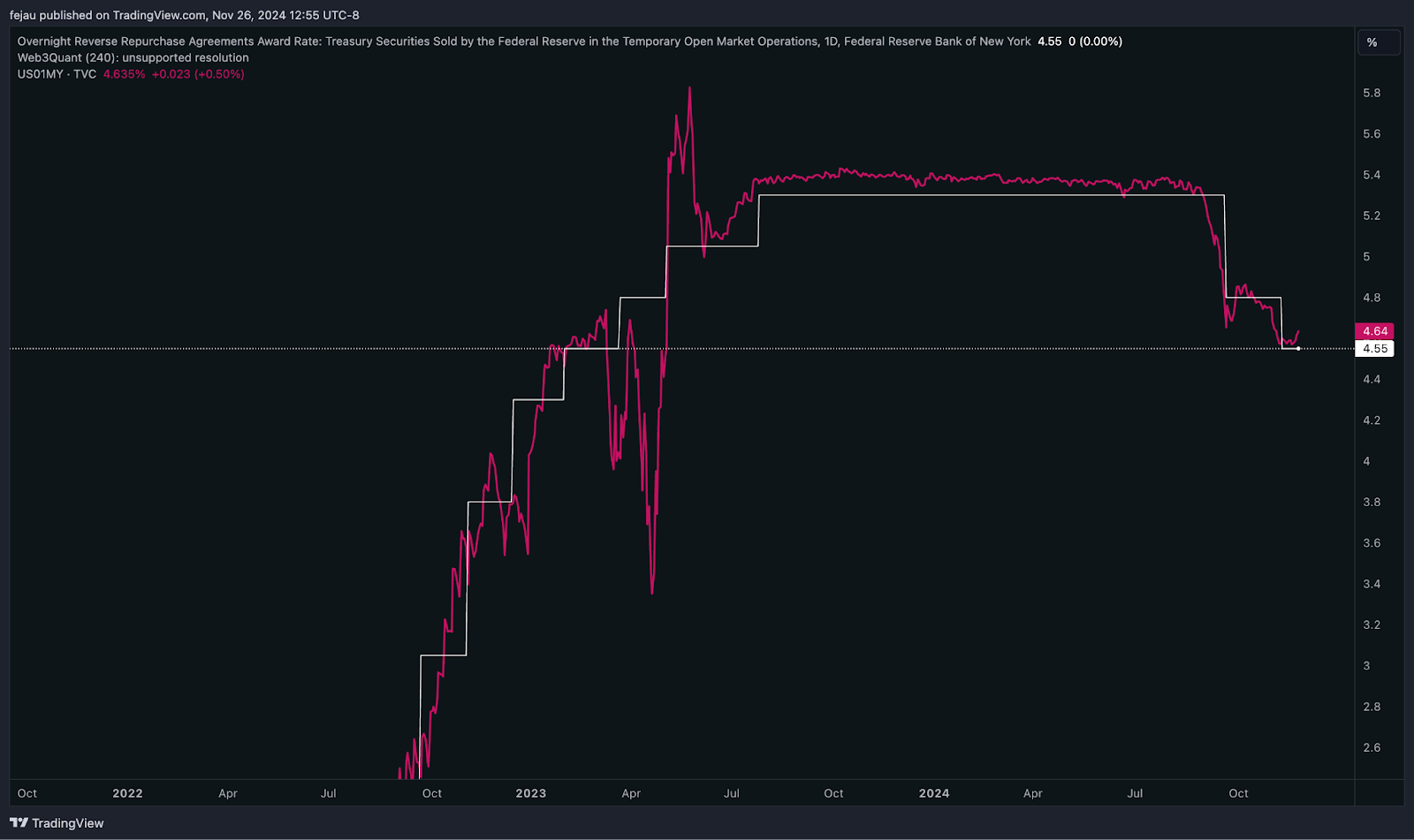

As shown in this chart comparing the $1 million T-bill with the RRP award rate, money market funds are generally alternating between owning the two, depending on which has the higher yield at the time. By decreasing the award rate, T-bills are made more attractive:

As we can see in the current balance of the RRP, there’s still $186 billion of cash that is “stuck” in the RRP. By lowering the award rate, it appears the FOMC is trying to get this money into the broad financial system to ensure liquidity remains ample. This comes in the face of ongoing QT that is getting closer to a potential target that could strain bank reserve levels:

We will need to wait until the next FOMC meeting in December to confirm if this will indeed be the case. The fact is, though, that by even acknowledging this potential dynamic, the FOMC is signaling that they are becoming increasingly concerned about bank reserve liquidity levels.