Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

Ten years ago, blockchain was a novelty technology that appealed to few beyond Bitcoin’s small community of “magic internet money” users. That coterie of supporters grew after the creation of a distributed smart contract framework called Ethereum. But even then, most of the world dismissed it as a solution in search of a problem: slow, energy-hungry, and difficult to scale.

The story is very different today. Mainstream interest is burgeoning, with PayPal among the latest in a slew of household names adopting blockchain-powered solutions that are being seamlessly integrated into our everyday lives. The venerable London Stock Exchange Group jumped on the bandwagon in early September, announcing plans to launch a blockchain-powered digital asset trading platform.

You might also like: The rise of CBDCs is inevitable but not risk-free | Opinion

This uptick in big brands and conglomerates embracing web3 tech points to an undeniable truth: that unlike the “solution in search of a problem” of the past, advances in blockchain have, in many cases, made it a better solution for many problems than more traditional tech stacks: one that is safer, more scalable, and easier to use.

From BTC to PYUSD

PayPal’s decision to launch a blockchain-based stablecoin last month is a perfect illustration of this. PayPal is using blockchain to make the crypto-to-fiat currency conversion process seamless, to power fast transfers of value to friends and family, to enable quick cross-border payments, and to make it easier for brands to start accepting crypto payments. For PayPal itself, the benefits are obvious: it can now settle all accounts on its own immutable ledger and facilitate feeless transactions, effectively creating greater security at lower costs.

The PayPal stablecoin is a case study of what blockchain does best: supporting and empowering communities. It grants builders the ability to create tokenized, verifiable on-chain communities of users with the ability to securely retain value and information without compromising data sovereignty. And if the builders so choose, blockchain also enables members to invest in the community they are participating in.

Blockchain powers customizable community ecosystems

Even if you’re not PayPal, stablecoins and other blockchain infrastructure offer benefits not available through any other current tech. Decentralized apps, layer 3 chains, and other unique blockchain solutions let their users create “in-house” ecosystems that exactly fit their own needs.

Retailers can launch stablecoins that provide blockchain-based rewards for their users; universities can launch ID systems that track academic credentials. And in the gaming world — where I am a builder — devs can build blockchain ID systems and launch crypto tokens usable interoperably across multiple games, or launch stablecoins that facilitate crypto-to-fiat payments across gaming hubs.

And crucially, while launching a token or building a blockchain once required millions of dollars and months of work, it is now possible to do both in just a few days without crippling costs. Many blockchain networks now feature tools that can help, such as Offchain Labs’s dedicated “tooling” that helps developers construct their own Layer 3 blockchains with the Orbit software stack on Arbitrum. Cosmos, Polkadot, and Avalanche offer similar capabilities.

Large-scale blockchain adoption is here

People may be interacting with blockchain without even knowing it: while big brands’ experiments with blockchain have not historically involved end users interacting with blockchain elements, consumers in a host of industries come face-to-face with blockchain-powered systems, whether they know it or not.

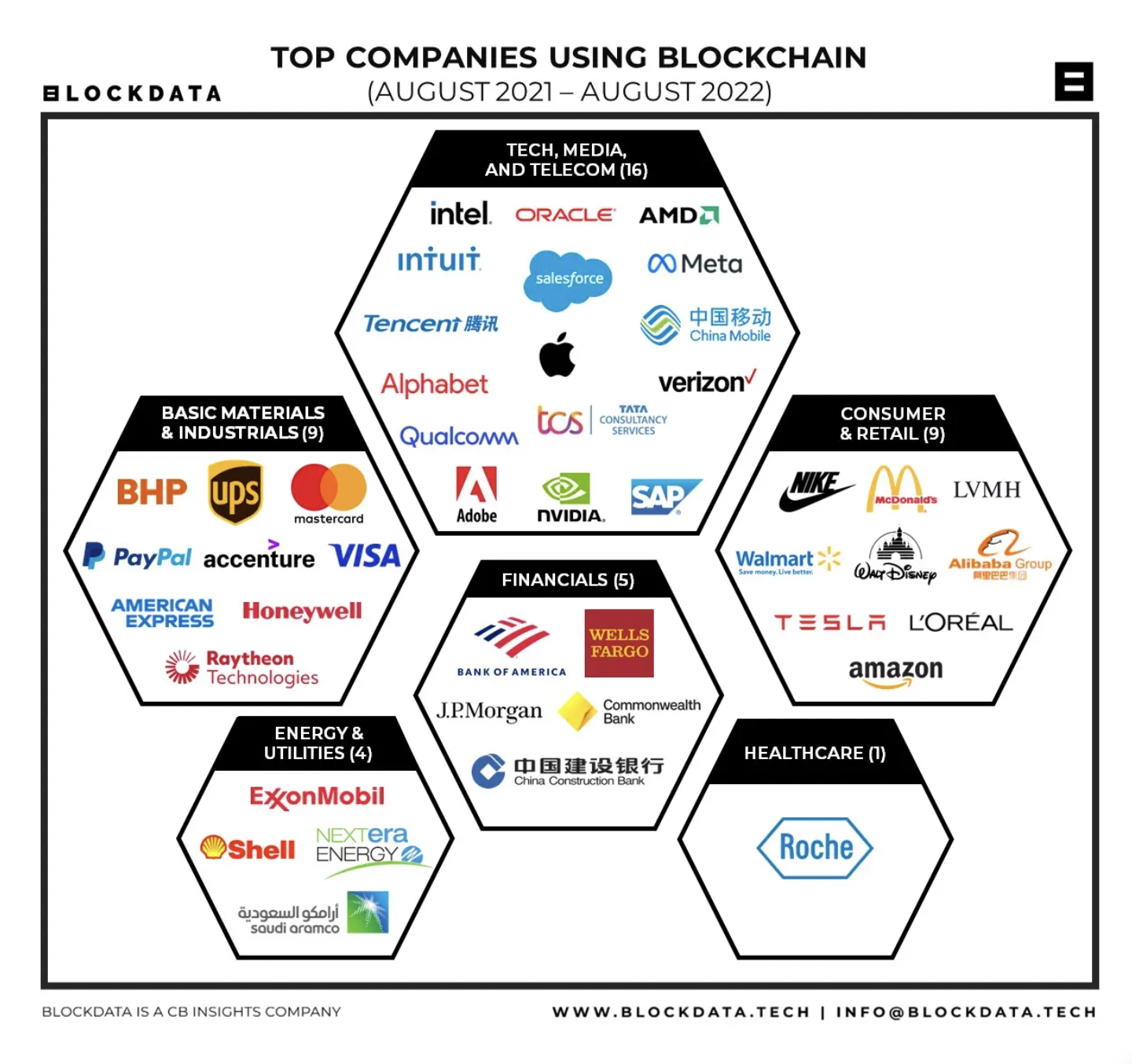

Top companies using blockchain between August 2021 – August 2022 | Source: Blockdata

For instance, PYUSD users interface with blockchain directly — but the tech is integrated so seamlessly into the PayPal platform that there’s no need for an external wallet, private key management, or other accouterments typically associated with crypto transactions.

Fulfilling early evangelists’ prophecies

Of course, there are still plenty of areas in which the application of blockchain may make UX more clunky or cumbersome rather than less. But the advances in technology that have made blockchain more accessible and usable have also brought it much closer to the ideal that early blockchain evangelists envisioned: a “magic” layer of the internet that anyone can use to create ecosystems of value.

Read more: PayPal’s stablecoin: potential impact and user reactions

Corey Wilton is the co-founder and CEO of Mirai Labs, an international Web3 gaming studio headquartered in Vietnam. Mirai Labs’ first release, Pegaxy, was recognized as the second-most popular crypto project in the Philippines in 2022, outperforming the likes of Ethereum, Bitcoin, and other major cryptocurrencies. A renowned speaker and play-to-earn thought leader, he began his first company within crypto in 2018, a customer support company designed to assist initial coin offering companies with their customer service.