Bitcoin’s second-quarter slide unfolded alongside a rare contraction in the stablecoin market, adding another sign that crypto liquidity weakened beyond spot prices alone.

Bitcoin traded below $60,000 during the quarter, reaching its lowest level since 2024, and fell 14% across Q2. At the same time, total stablecoin supply slipped to $312 billion, down more than $3 billion from the previous quarter, CEX.IO said in a report shared with CryptoSlate.

The decline marked the first quarterly drop in stablecoin supply since the third quarter of 2023. The pullback was small in percentage terms, but it came as the broader crypto market lost 6.2% of its value.

That lifted stablecoins’ share of total crypto market capitalization to 14% from 13%, showing that investors still held a larger portion of the market in dollar-linked tokens even as capital left the sector.

Stablecoins are often treated as crypto’s cash layer. Traders use them to move between exchanges, settle transactions, park funds and access decentralized finance.

Consequently, a decline in their supply does not automatically mean users are abandoning stablecoins, but it indicates fewer digital dollars circulating in the market at a time when trading, transfers, and speculative activity have also weakened.

Yield products turn into a drag

The sharpest change came from yield-bearing stablecoins, which had been one of the stronger parts of the market since mid-2023.

After rising every quarter for nearly three years, the category fell by more than $3.5 billion, or 15%, in Q2. The decline reversed a 19% gain in the first quarter and showed how quickly demand shifted away from crypto-native yield strategies as market conditions worsened.

Ethena’s sUSDe accounted for much of the drop. Its market capitalization fell by 52%, erasing nearly $2 billion in market value. Sky’s sUSDS also declined, losing 16% during the quarter.

Those two assets had helped drive earlier growth in yield-bearing stablecoins, but they became a source of pressure as users reduced exposure.

Conversely, institutional appetite for yield shifted toward products backed by real-world assets (RWAs) and short-term US government debt. BlackRock’s BUIDL tokenized fund grew by 2%, while alternative treasury-backed offerings like USYC and USDY climbed 16% and 66%, respectively.

The bifurcated performance points to a distinct flight to safety within the stablecoin market itself, with capital migrating from algorithmic and synthetic DeFi mechanisms toward regulated, yield-bearing traditional financial instruments.

Layer-2 networks lose stablecoin balances

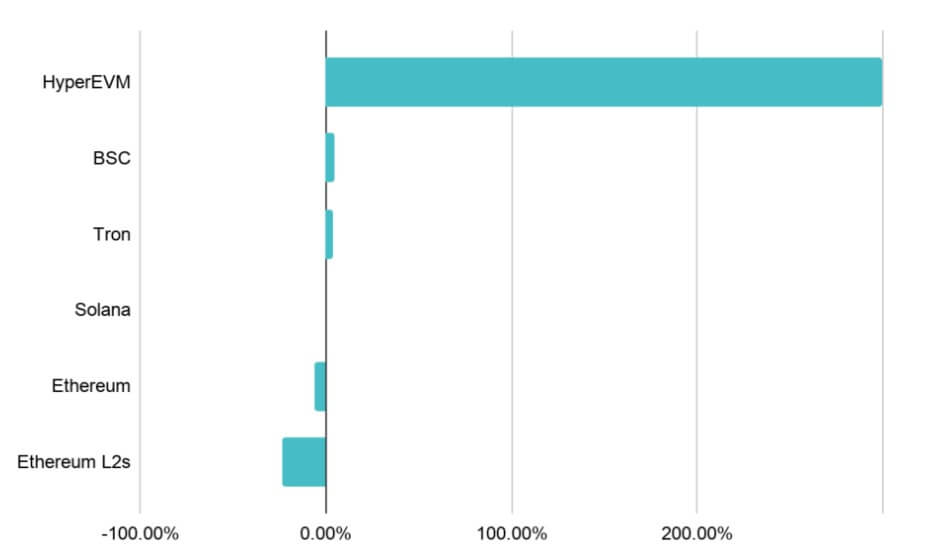

The contraction also showed up across blockchain networks, especially on Ethereum layer-2s.

Stablecoin supply on Ethereum scaling networks fell 24%, or $4.34 billion, in Q2. That was the largest quarterly decline for the segment since the fourth quarter of 2022.

Arbitrum accounted for most of the fall. Its stablecoin supply dropped 45%, losing $3.5 billion during the quarter. The network had previously benefited from its role as a major route into Hyperliquid.

HyperEVM’s own stablecoin supply rose 300% to $5.6 billion, showing that some liquidity shifted away from Arbitrum rather than leaving the market entirely.

Ethereum’s base layer recorded an even larger absolute decline, losing more than $10 billion in stablecoin supply. CEX.IO said that was Ethereum’s steepest quarterly drop since the first quarter of 2023.

Other networks moved in the opposite direction. Tron added $3.4 billion in stablecoin supply, while BNB Chain gained $700 million.

The increase in those chains was largely tied to payment activity, showing that stablecoins used for transfers and settlement remained more resilient than those tied to DeFi and trading flows.

The network-level data points to a market that is not contracting evenly. Some crypto-native liquidity channels weakened sharply, while payment-heavy chains continued to grow.

That difference could shape how quickly the market stabilizes if trading activity remains subdued.

$USDC gains share as trading falls

A clearer confirmation of systemic deceleration appeared in network activity metrics, but $USDC stood out as an exception.

CEX.io stated that total stablecoin trading volume fell 18% to $6.8 trillion. $USDT volume dropped 24%, reflecting a broader decline in crypto trading activity.

On the other hand, $USDC volume rose 34%, making it the only major stablecoin to record absolute trading growth during the quarter. That pushed $USDC’s share of total crypto trading volume to 12.5%, a record high. The previous high was 11%, set in the fourth quarter of 2023.

The shift partly reflects changes in centralized exchange markets, especially in Europe. Tether has not secured authorization under the European Union’s Markets in Crypto-Assets (MiCA) framework, and exchanges have been reducing $USDT support in regulated European venues.

That has created more room for $USDC, which has benefited from Circle’s compliance position in the region.

CEX.IO’s platform data showed a similar pattern. $USDC accounted for 60% of stablecoin-related financial operations on the exchange in Q2, up from 58% in the first quarter and 27% in the first quarter of 2025.

The figures show $USDC gaining ground even as the overall trading environment cooled. That gives Circle’s token a stronger position in regulated exchange activity, while $USDT’s dominance faces more pressure in markets where compliance requirements are tightening.

Transfers show a broader slowdown

Notably, the clearest sign of weaker activity in the stablecoin sector came from transaction data.

Stablecoin transaction counts fell to 4.48 billion in Q2, down 530 million from the previous quarter. CEX.IO said that was the largest absolute quarterly decline on record. The 11% drop was also the steepest percentage decline since the fourth quarter of 2022.

The slowdown remained visible after removing bot, automated, and non-economic activity. Adjusted transaction counts fell to 613 million, down about 11 million from Q1.

The smaller decline in adjusted activity suggests that a large part of the overall drop came from infrastructure-related and automated flows rather than ordinary users alone.

Adjusted transaction volume also fell. Organic stablecoin transfer volume dropped 5.5% to $4.09 trillion, ending a run of 10 consecutive quarterly increases. The reversal followed an 18.3% gain in the first quarter, making the Q2 decline more notable.

Still, smaller transfers held up better. Transfers below $250 rose 5% to $19.39 billion. That increase suggests that retail-sized payments and peer-to-peer movement remained active even as larger transfers slowed.

The difference between small and large transfers is important for the second half of the year. If smaller payments continue to grow while high-value trading and infrastructure flows decline, stablecoins could become less tied to crypto market cycles over time. If larger flows continue to fall, however, the market may face a longer liquidity reset.

Regulation now meets a weaker market

The second-half outlook will depend partly on whether regulation brings new demand quickly enough to offset weaker crypto-native activity.

In Europe, MiCA’s transition period ended July 1, forcing crypto-asset service providers to operate under the bloc’s authorization regime or stop serving EU clients.

That could continue to reshape stablecoin trading pairs, particularly where exchanges move away from $USDT and toward regulated alternatives.

In the US, the GENIUS Act is pushing stablecoin issuers toward clearer reserve, redemption and supervision standards. The CLARITY Act could add a broader market structure framework for digital assets, though its path remains tied to the Senate calendar and unresolved political fights.

Traditional financial firms are also moving deeper into stablecoins. For context, SoFi and MoneyGram have announced plans for stablecoins, while Japan’s three largest banks have advanced work on a joint yen-pegged token.

Those efforts suggest that institutional interest has not disappeared, even as crypto-native demand weakened in Q2.

The question is whether new payment, banking, and real-world asset use cases can offset the pressure from declining trading activity.

During the 2022-2023 downturn, stablecoin supply took about a year to return to sustained growth.

However, the current cycle may not follow that timing because the market is more diversified than it was three years ago.