Institutional crypto now centers on controlled access. Large financial firms are using on-chain systems for repo, treasury activity, and cash management inside environments built around compliance and permissions. Meanwhile, public DeFi still offers liquidity, continuous markets, and programmable finance. In 2026, these two systems are starting to connect.

This setup is producing an on-chain market with different users, tools, and priorities. Whereas permissioned networks give institutions governance and oversight, public chains offer the liquidity and applications institutions still want to reach.

Tokenized treasuries are also gaining ground as a low-risk asset for compliant capital, while cross-border settlement still depends on whether legal and compliance systems can work across jurisdictions. Retail users are entering through fintech apps with accumulation in mind, while earlier crypto holders are focusing more on preservation.

To explore where this is all heading, BeInCrypto spoke exclusively with Federico Variola, CEO of Phemex, Fernando Lillo Aranda, Marketing Director at Zoomex, and Pauline Shangett, CSO at ChangeNOW.

Permissioned Chains Still Need Public Liquidity

TradFi’s connection to public DeFi is forming through controlled gateways. Institutions want access to on-chain liquidity and settlement, but they also need identity checks, permissions, and compliance controls. As a result, the market is developing systems where regulated participants can operate in gated environments and still connect to public chains.

Shangett says the divide between private institutional networks and open DeFi is already giving way to a more connected model. She says”

“For years, people acted like permissioned institutional chains and public DeFi were oil and water. One for compliance, the other for actual liquidity. What they’re doing is building tubing, not just mixing.”

Avalanche is one example. Its Evergreen work around Spruce has been used in tokenization testing, while Avalanche Warp Messaging allows communication between Avalanche-based environments. ZKsync is pursuing a similar idea through enterprise-focused systems tied to Ethereum.

The result is a market where institutions can connect to public crypto without giving up control over access, counterparties, and governance.

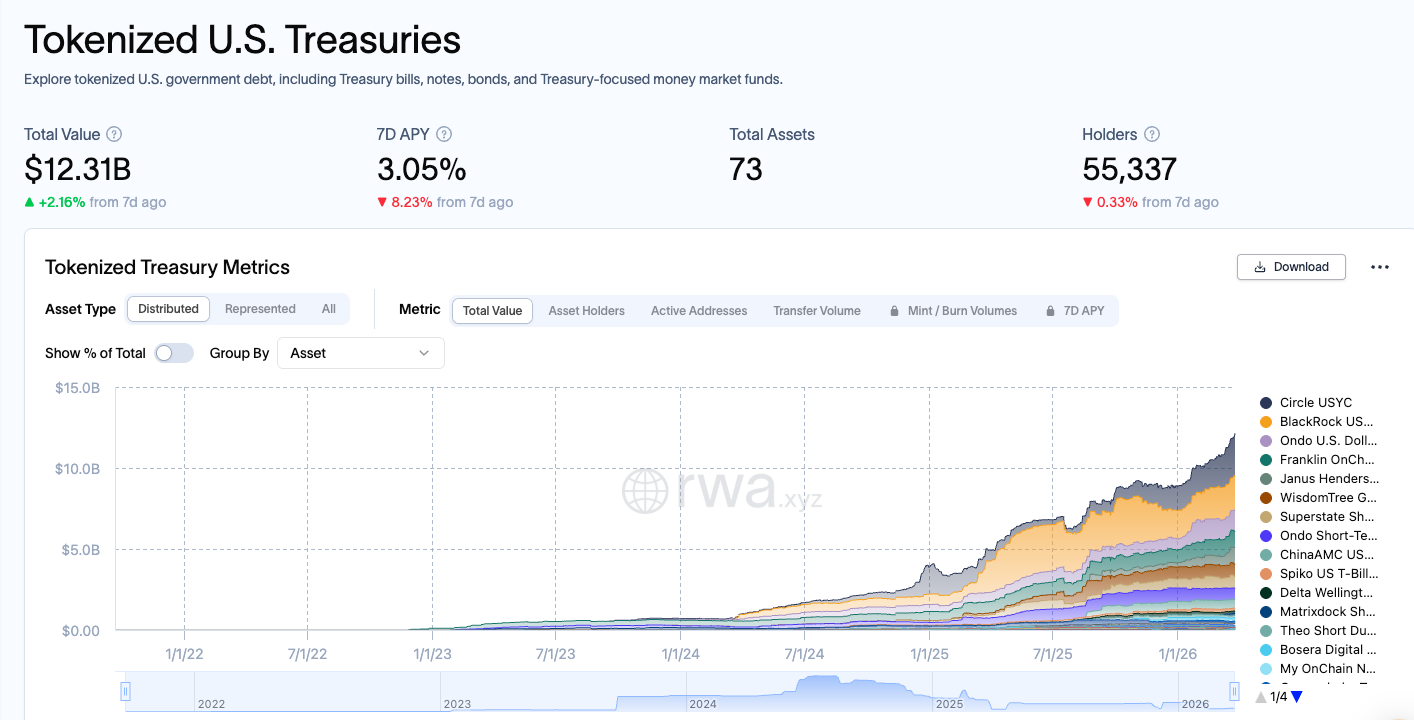

Tokenized Treasuries Are Becoming the Benchmark, But Not for Everyone

Tokenized T-bills and government bonds are becoming a benchmark asset for compliant on-chain capital. By late March 2026, the tokenized U.S. Treasuries market stood at about $12.31 billion, giving the category real weight in digital asset markets.

Variola sees this as a strong sign of DeFi’s development:

“Yes, the tokenization of T-bills and government bonds is probably one of the clearest signs of maturity for the DeFi ecosystem. The larger this market becomes, the more mature I would consider the DeFi space to be. It would also signal that participants in the DeFi ecosystem are gradually moving away from purely risk-prone trades toward more risk-averse capital preservation strategies.”

“In that sense, it could mark a transition where the on-chain economy begins moving from pure speculation toward something closer to traditional finance, but with the advantages of simpler cross-border settlement and more efficient international money transfers.”

For funds, treasuries, and other compliant investors, tokenized government debt offers a familiar low-risk asset with yield and transferability.

Shangett agrees, but says this benchmark serves a specific part of the market:

“Look, the numbers don’t lie. Tokenized T-bills and government bonds are now a $10+ billion market, up from basically nothing 18 months ago. BlackRock’s BUIDL alone is sitting at $2.5 billion, and they’re moving it across Solana, Arbitrum, BNB Chain, basically wherever institutions want to park cash. Ondo’s OUSG and USDY are doing the same thing with slightly different compliance wrappers.”

“So yes, on-chain treasuries are real, and for the KYC’d, accredited, ‘we-have-a-compliance-team’ crowd, they are absolutely becoming the risk-free benchmark.”

In her view, tokenized treasuries are becoming the benchmark for regulated capital, while retail DeFi users still rely more on stablecoin lending rates and permissionless money markets.

The Hard Problem Is Legal Certainty

Cross-border settlement still runs into the same issue every time capital moves between jurisdictions. Tokens can move instantly, but legal and operational conditions do not. Different countries apply different rules on custody, disclosure, transfer restrictions, and compliance, so technical settlement and legal finality do not always arrive together.

Lillo Aranda says the real challenge sits outside blockchain speed:

“The biggest hurdle is not tokenization itself – it’s interoperability between legal, technical, and operational systems that were never designed to move at the same speed.”

“From a technical perspective, 24/7 settlement requires synchronized standards around identity, messaging, collateral recognition, finality, and compliance automation. A token can move instantly, but that doesn’t mean the surrounding regulatory obligations settle instantly with it.”

“Different jurisdictions will also define asset classification, custody, disclosure, and transfer restrictions differently. So the real bottleneck is not blockchain throughput – it is the fragmentation of regulatory logic across borders.”

“In other words, we already know how to move value globally in real time. The challenge is making that movement legally interoperable, auditable, and institutionally acceptable across multiple regimes at once.”

His point gets to the core issue. The technology is ready for continuous settlement, but the operating environment still depends on national rulebooks and fragmented standards.

Shangett makes a similar point. In her view, the hardest part is getting countries and financial systems to accept compatible rules at the same time.

For on-chain finance, this leaves cross-border settlement in an awkward position. Continuous transfer is possible. Continuous regulated settlement across multiple jurisdictions is still much harder to run.

Retail Is Accumulating While OGs Are Preserving

Retail crypto users are entering the market with a different mindset from the first generation of holders. The earlier cycle rewarded conviction and volatility tolerance, while the current one breeds steady portfolio building through fintech apps, recurring buys, and accessible yield products.

Shangett says the split comes down to incentives”

“I guess the difference isn’t age or wealth. It’s when you entered and what you’re trying to do. There are two groups operating in parallel realities… one is in accumulation mode, the other in preservation mode.”

“Wealth accumulation (Robinhood/Revolut crowd). This is the grind phase. They’re not waiting for one 100x moonshot. They’re DCA-ing into 10+ assets, chasing 5-15% staking yields, and using apps that now let them buy into private tech deals like Databricks alongside their crypto. It’s systematic, yield-aware, and boring by design. The goal is to stack consistently, not hit a lottery.”

“Wealth preservation (early adopters). These people bought BTC at $500 or farmed ARB airdrops. They’re not trying to 10x anymore, they’re trying not to lose what they already have. That means rotating out of speculative bags into productive assets like staking, tokenized T-bills, lending on Morpho. They’re also exiting the casino early because token supply per user has exploded 24x since 2021. Their cold storage holds the core stack; exchanges are just for yield and tax efficiency.”

“So one group is building a kingdom with grind and diversification. The other already has one and is just trying to keep the walls from falling down.”

One group is building positions gradually through mainstream apps. The other is focused on protecting wealth and reducing volatility. In 2026, retail crypto is divided between accumulation and preservation.

Final Thoughts

Institutions want controlled access to public liquidity. Tokenized treasuries are becoming a benchmark asset for compliant capital, while cross-border settlement still depends on whether legal and operational systems can work across jurisdictions on a continuous basis.

The experts in this piece point to the same conclusion from different angles.

- Federico Variola sees tokenized government debt as evidence of a more mature DeFi market built around preservation as well as return.

- Fernando Lillo Aranda identifies the key challenge in cross-border finance as legal and operational interoperability rather than blockchain speed.

- Pauline Shangett describes a market where permissioned networks and public DeFi are connecting through controlled access, while institutional and retail users continue to follow different paths.

What is emerging in 2026 is an on-chain financial system serving different kinds of capital in different ways.

Public crypto provides liquidity and composability. Regulated finance brings governance, compliance, and familiar low-risk assets. The point of convergence sits in the connections between them.