Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Ruchir Gupta on how we’re moving toward a true fixed-income market for crypto-native yield.

- Clara García Prieto on bitcoin becoming mainstream collateral, but most are not prepared for its risks.

- Top headlines institutions should pay attention to by Francisco Rodrigues.

- Crypto card volumes hit $140 million record in Chart of the Week.

-Alexandra Levis

Expert Insights

When price stops working, yield starts mattering

- By Ruchir Gupta, co-founder, Gyld Finance

There is a pattern that repeats itself across asset classes. Bull markets are simple: buy risk, ride beta, everything looks like genius. Then conditions shift, leverage unwinds, volumes thin and the question changes from “how much did you make” to “what are you actually earning while you wait.”

Crypto is in that shift right now. Prices have corrected significantly, with bitcoin about 50% below its peak. Speculative positioning has compressed. Perpetual funding rates have normalized. For investors holding digital assets through this, yield has become the cushion that makes staying in the trade worthwhile.

Ether ($ETH) staking, as measured by the benchmark Composite Ether Staking Rate (CESR), returns roughly 2.5% to 4% annualized. Solana (SOL) validator rewards run closer to 6% to 8%. Lending protocols offer variable rates across collateral types. Crypto-native yield is real, diversified across sources and does not require price appreciation to accrue.

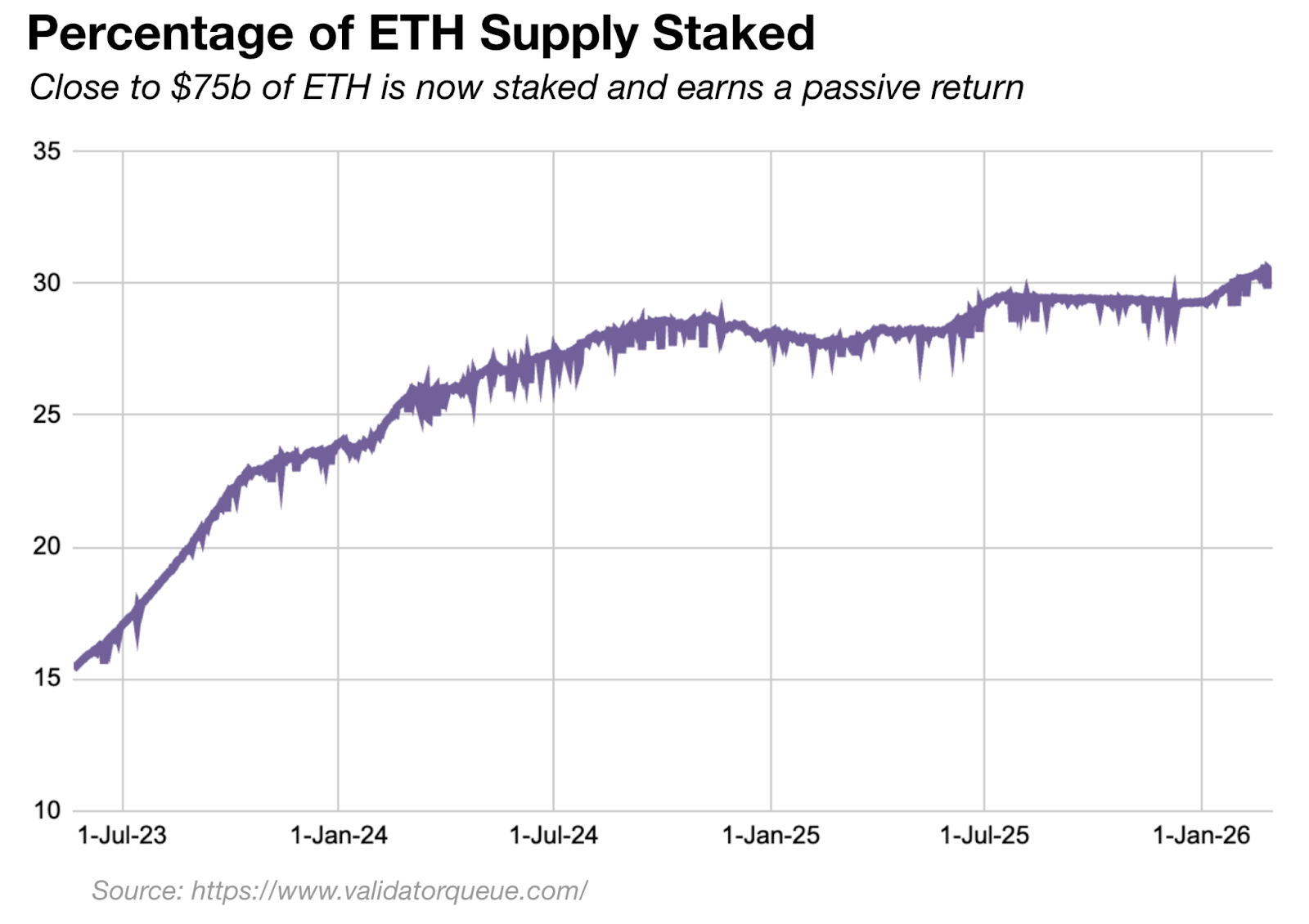

The clearest evidence is in the staking participation data. $ETH staking supply has hit all-time highs, with close to 30% of all $ETH staked now. That growth continued through periods of significant price weakness. Allocators kept staking regardless of what $ETH was doing in spot markets because the yield was there independent of price.

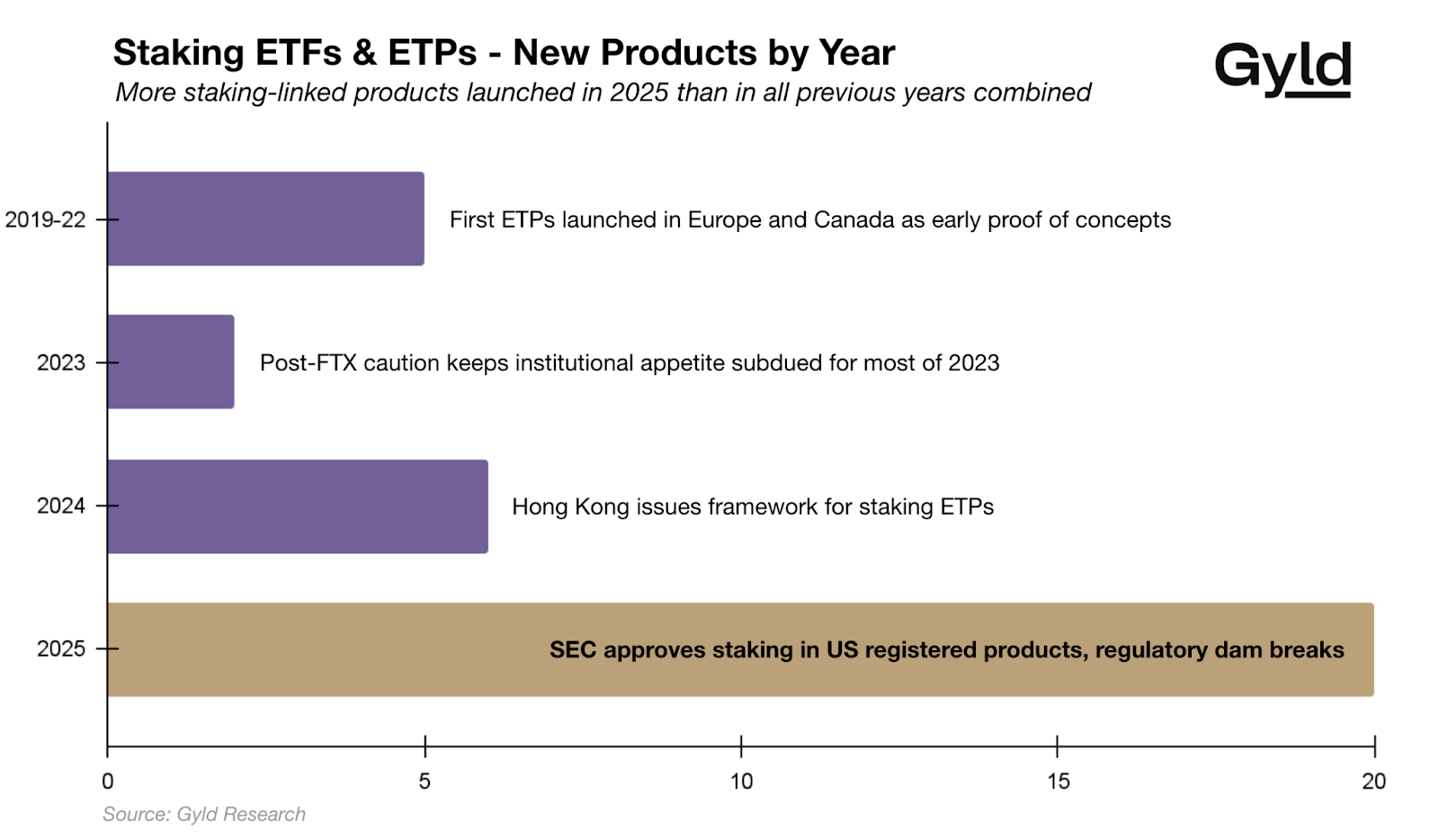

Institutions have noticed. After the SEC provided regulatory clarity around staking in U.S.-registered funds last year, nearly twenty staking-linked ETFs and ETPs have launched or been filed, including BlackRock’s iShares Staked Ethereum Trust and products from VanEck, Grayscale and Fidelity, more than in all previous years combined. Morgan Stanley, which manages roughly $8 trillion in client assets, applied in February for a national trust bank charter from the Office of the Comptroller of the Currency (OCC) to offer crypto custody and staking services to its investment clients.

But every one of these products is, today, a passive fund. You get yield at whatever rate the network happens to be paying, bundled with price exposure, with no ability to manage duration or isolate income from principal. That leaves a lot on the table.

Staking yield has two characteristics that make it particularly interesting as a traded market:

First, rewards are variable and driven by network-level activity. Transaction volumes, validator set size and overall participation all move the rate. Staking rewards behave somewhat like a macro rate: when the network is busy and demand for block space is high, rewards rise; when activity falls, they compress. That variability is not just a risk to be passively absorbed. It is a signal that can be traded.

Second, staking is partly illiquid in a structured way. $ETH's validator entry queue currently runs over two months, meaning capital committed today does not start earning for more than sixty days. That queuing dynamic creates a forward curve. The rate you expect to earn in three months is not the same as the rate available today and the gap between them is something a market should price.

Together, these two features mean staking yield has the ingredients of a proper rates market: a floating benchmark that moves with observable fundamentals, and a term structure created by real illiquidity and expectations of forward network activity. This is exactly the kind of market active managers get paid to navigate.

Capturing that opportunity requires a toolkit that does not yet exist in regulated form: instruments that let you price yield independently of principal, so a buyer can take a view on rate direction without carrying spot exposure; instruments with defined maturities that make the illiquidity premium explicit and tradable; and instruments that separate the income stream from the capital claim entirely, so each can find its natural holder. In traditional fixed income, these are strip bonds, zero coupon instruments and floating-rate notes. They are the building blocks without which you cannot run anything more sophisticated than a passive fund.

Once those instruments exist, the rest follows naturally. The first active staking funds will look like something money market managers do today: rotating across maturities, pricing illiquidity risk and taking views on forward network activity rather than just collecting whatever rate the network is currently paying.

Decentralized finance (DeFi) tackled this problem early, though aimed at a different market and built on different yield sources. Protocols like Pendle Finance have built an elegant yield tokenization engine that separates principal tokens from yield tokens and lets them trade independently. The mechanics work, but the wrapper is unsuitable for institutional capital, as it looks too much like a security in most jurisdictions and lacks regulatory clarity.

What we are moving toward is a genuine fixed income market for crypto-native yield, with term structures, actively managed duration strategies and products that compete on the precision of their yield management rather than simply on access.

Bull markets reward beta. Bear markets reward income. Mature markets reward the ability to manage risk precisely. We are somewhere between the second and third phase, and the infrastructure for that third phase is largely still missing.

Principled Perspectives

Bitcoin as collateral: the shift redefining the financial system

- By Clara García Prieto, founder, BTL

More than five years ago, suggesting that bitcoin could be used as collateral — and that traditional financial institutions might seriously consider it — would have sounded improbable. Today, that scenario is no longer theoretical: bitcoin has entered the financial system and, in doing so, is redefining what we understand as collateral. Bitcoin is not just becoming collateral — it is redefining what collateral means.

As a lawyer, my view is clear: the use of bitcoin as collateral is inevitable, but most participants are not prepared for the risks it entails. In my opinion, this will be the dominant pattern over the next five to ten years.

To understand the magnitude of this shift, it is useful to look at a classic example: a real estate mortgage. In this structure, there is a loan (the principal obligation) and a guarantee (the property) that secures it. Bitcoindoes not fit neatly within the current logic:: it is not tied to a specific jurisdiction, it does not rely on public registries and its control is based on cryptographic keys. This forces us to reinterpret the concept of collateral rather than simply replicate it.

Bitcoin has unique characteristics: it is a digital asset, finite, with a fixed and deterministic supply. Many who hold it — whether individuals or companies — do not to part with it. On the one hand, this is because of its scarcity and potential appreciation; on the other, because of the tax implications of disposing of it. This is where a key shift emerges: obtaining liquidity without selling the asset.

However, there is a structural tension. Bitcoin does not typically depend on intermediaries, but collateralized transactions must depend upon them to some extent. And this is the real critical point.

In centralized models, the primary risk is custody. The user must trust that the entity holding the collateral acts diligently and remains solvent. Translating this to trust to the crypto context is not a minor issue and requires careful analysis of how custody is managed. Traditional financial institutions are already exploring this — for example, by assessing the use of bitcoin ETFs as collateral for institutional clients. The movement has begun, even if we are still only seeing the tip of the iceberg.

In decentralized finance (DeFi), the problem is different. Native bitcoin cannot be used directly, as it requires the use of tokenized representations. This introduces new risks: reliance on smart contracts, protocol risk, potential price discrepancies and the need for active collateral management. Additionally, there may be tax implications, depending on jurisdiction, if the transaction is treated as a taxable event.

At the same time, the use of bitcoin as collateral is beginning to be integrated into corporate treasury strategies. In my view, this will be one of the most relevant developments. Companies with strong liquidity and solid balance sheets can use bitcoin as a strategic asset, reducing their reliance on external financing. Those who adopt it early will have a clear competitive advantage.

That said, bitcoin’s volatility will prevent it from replacing traditional collateral. No financial system can rely exclusively on an asset that can fluctuate significantly over short periods of time, as they require overcollateralization and strict risk management mechanisms.

We are facing a form of collateral with unique characteristics that cannot be ignored. Volatility and the associated risks — custody, counterparty and structural — are real. But so is its potential. The use of bitcoin as collateral is no longer a hypothetical; it will become increasingly common. The question is not whether it will happen, but who is prepared to manage it properly.

Headlines of the Week

- By Francisco Rodrigues

The cryptocurrency industry has kept on slowly maturing over the week, with headlines pointing to the Bitcoin network’s physical resilience, the Ethereum Foundation’s evolution, and further institutionalization of the technology underpinning it.

- Bitcoin can survive 72% of the world's submarine cables being cut: That’s according to a Cambridge study spanning 11 years and 68 verified cable failures. It found Bitcoin’s physical infrastructure is far more resilient than previously thought.

- Ethereum Foundation publishes new mandate defining its role, core principles: In a 38-page document, the Ethereum Foundation outlined its philosophy and role as a steward of the Ethereum network. The document emphasizes Ethereum’s core mission to enable user self-sovereignty, and that it must preserve censorship resistance, open source, privacy and security.

- European Central Bank unveils tokenized finance plan to bolster EU's financial autonomy: The European Central Bank published its Appia roadmap, outlining a long-term plan to build a euro-anchored tokenized wholesale financial system using distributed ledger technology and central bank money settlement.

- Mastercard Launches Global Crypto Partner Program with 85+ Companies: Mastercard unveiled its Crypto Partner Program, bringing together more than 85 companies, including Ripple, Solana, Circle, Binance and other major players, to accelerate real-world blockchain use cases in cross-border payments, settlement and consumer crypto spending.

- Prediction markets get tailored U.S. guidance from former foe CFTC: The agency, which was once a legal opponent of certain activity at prediction markets, is now establishing policy for their oversight, with staff-issued advisory to regulated firms and initial guidance rolling out.

Chart of the Week

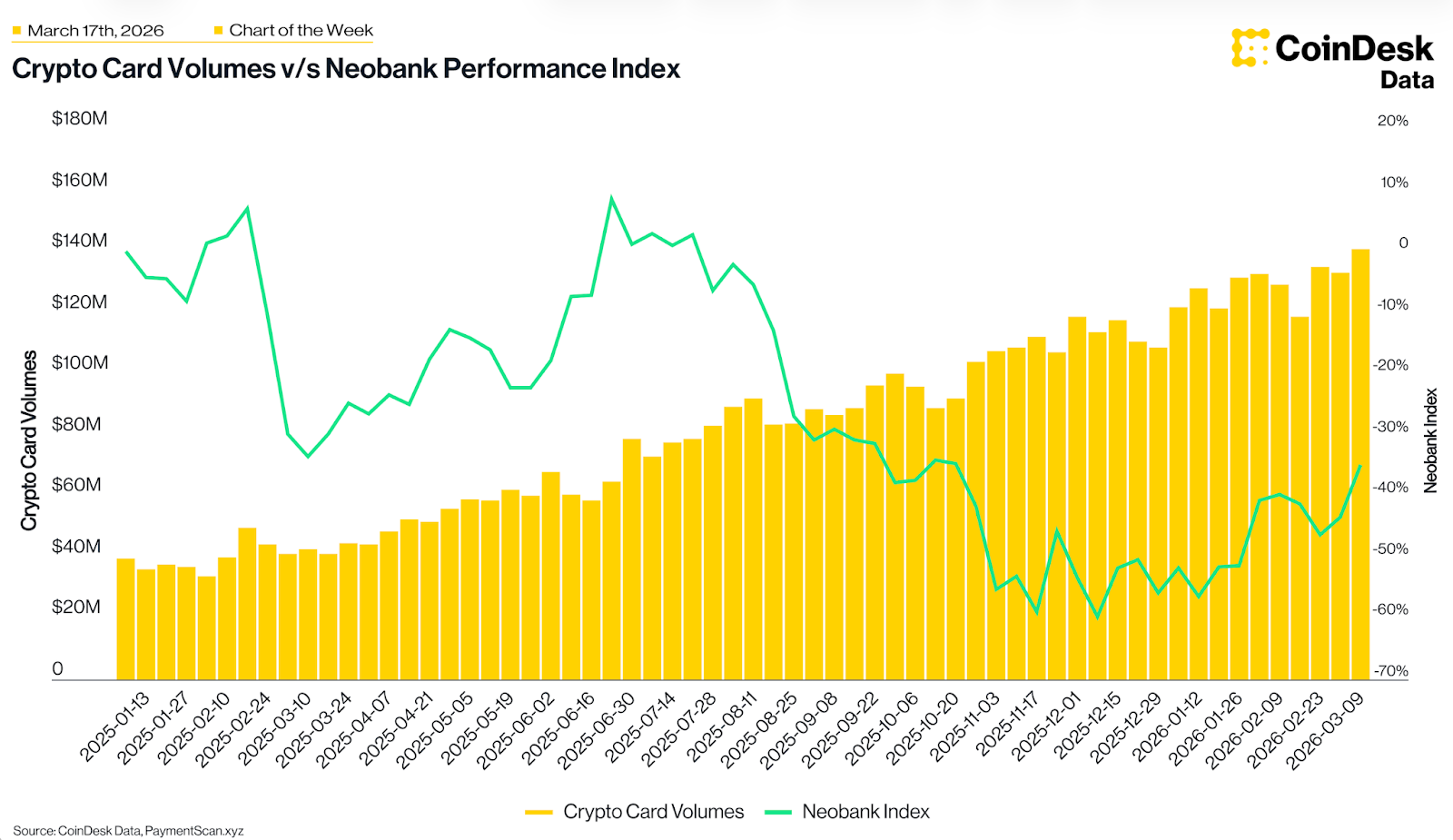

Crypto card volumes hit $140 million record as Neobank tokens lag behind

Weekly crypto card volumes continue their steady uptrend, reaching a new milestone of $140 million this week driven largely by RedotPay’s dominant $91 million contribution. While the broader Neobank Performance Index (including tokens like Avici and ETHFI) remains down 34% since the start of 2025, it has shown signs of a recent turnaround with a 10% recovery month-to-date. This divergence suggests that while asset valuations are still recovering from yearly lows, the actual utility and transaction volume of crypto cards are scaling to all-time highs.

Listen. Read. Watch. Engage.

- Listen: Did you hear? CoinDesk launched a NEW show on the floor of the NYSE! Public Keys with Jennifer Sanasie.

- Read: In Crypto for Advisors, Ganna Vitko, president of the Toronto Chapter of Women in Crypto, takes us through crypto accounting rules and challenges. Then, Aaron Brogan of Brogan Law PLLC answers questions about token issuance and its tax implications.

- Watch: Digital Assets Council of Financial Professionals Founder Ric Edelman joins CoinDesk's Jennifer Sanasie to discuss why “the banks are dead wrong” and the potential passage of the Clarity Act.

- Engage: Consensus Miami is approaching and the agenda is live! View the summits, stages, speakers and networking events.

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions.

Note: The views expressed in this column are those of the author and do not necessarily reflect those of CoinDesk, Inc., CoinDesk Indices or its owners and affiliates.