Daniel Oliver, founder of Myrmikan Capital, discussed in a recent interview what he believes is a decisive turning point in the gold bull market — and a brewing storm in U.S. private credit.

Margin Calls and Maturity Walls: Inside Gold’s New Reality

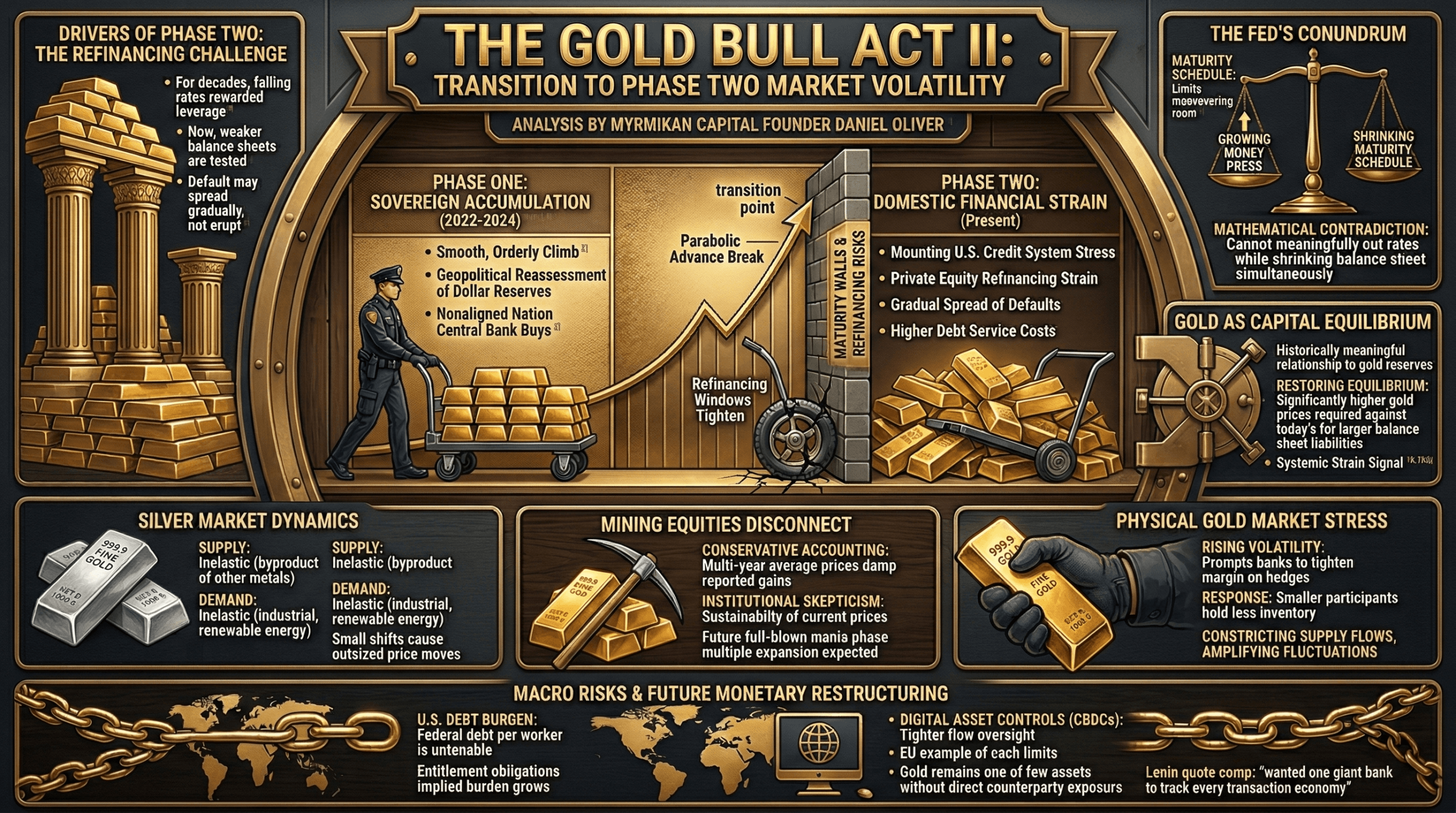

Speaking in an interview with Kitco News anchor Jeremy Szafron, Daniel Oliver contends that the smooth, sovereign-driven accumulation phase that defined gold’s rise since 2022 has officially ended. In its place, he sees a more volatile second stage powered by mounting stress in the U.S. credit system, refinancing risks in private equity, and a Federal Reserve facing a heavy maturity schedule with limited maneuvering room.

According to Oliver, phase one began when geopolitical tensions in 2022 prompted a reassessment of dollar reserves among nonaligned nations. Central banks stepped up gold purchases, largely indifferent to short-term price swings. That steady institutional bid pushed gold into a powerful, orderly climb.

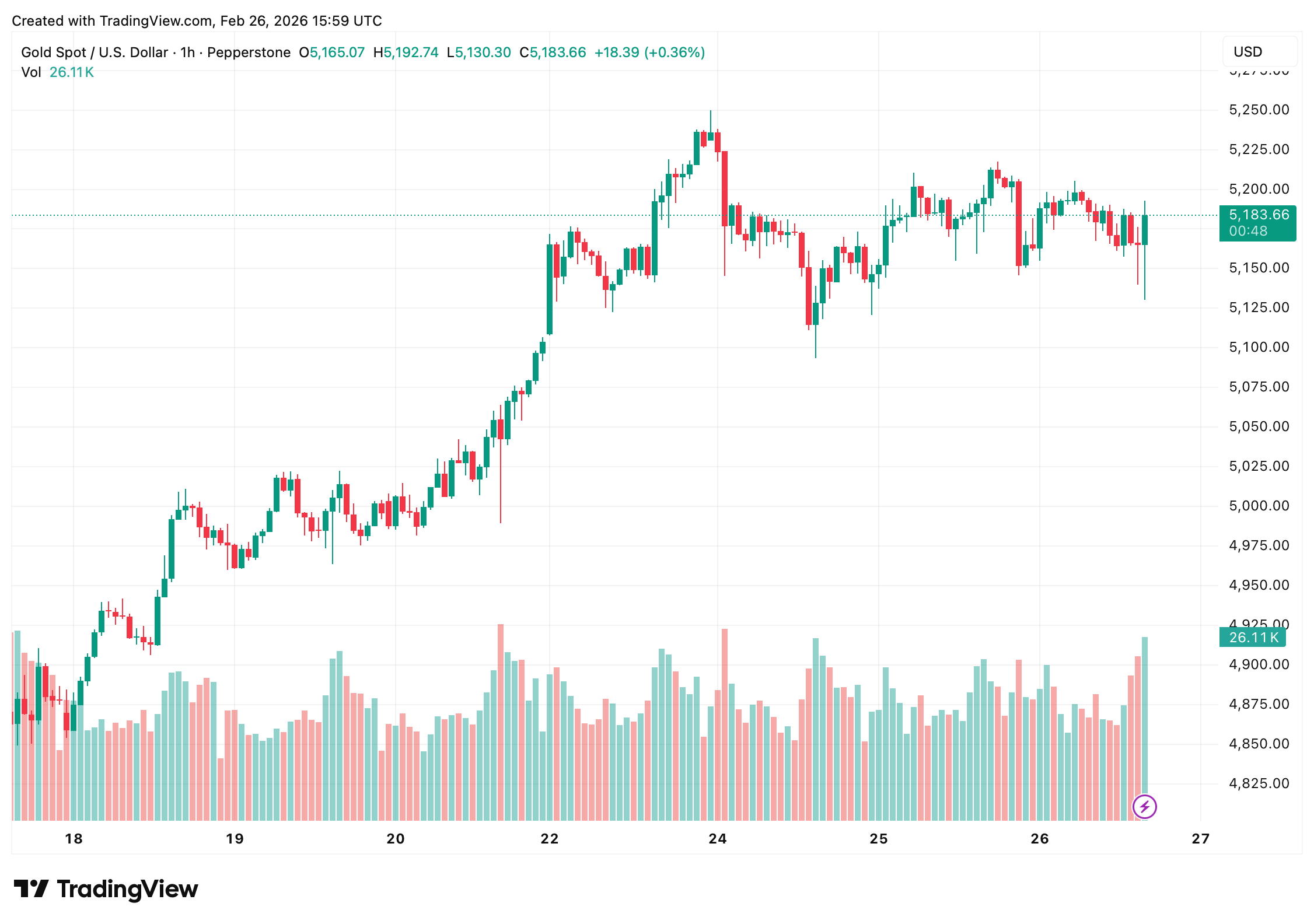

That orderly climb, he says, has fractured. The chart’s parabolic advance has given way to more violent price swings — a signal, in his view, that gold is transitioning into phase two. This stage is defined not by quiet central bank buying, but by domestic financial strain.

Oliver explained:

“If you look at the chart, the gold price painted a very nice parabola until a few weeks ago when that broke, and now we’re in more volatile markets.”

At the center of his thesis is private equity and private credit. For decades, falling interest rates rewarded leverage. Funds borrowed heavily, acquired companies and refinanced at lower costs. Now, with rates elevated and refinancing windows tightening, weaker balance sheets are being tested. Companies that once rolled debt forward with ease may face higher costs or limited access to capital.

Oliver argues that this pressure is just beginning to surface. Defaults may not erupt all at once, as in 2008, but instead spread gradually across industries as debt maturities come due. The effect, he suggests, could be broad and persistent.

The Federal Reserve complicates matters. Oliver questions whether policymakers can meaningfully lower interest rates while shrinking the balance sheet at the same time. In his view, tightening liquidity while attempting to ease financial conditions is mathematically contradictory. If credit markets seize, he expects the Fed will expand its balance sheet rather than risk systemic collapse.

“We know that in a crisis the Fed is going to print a lot more money and grow the balance sheet a lot bigger,” Oliver remarked.

That dynamic feeds directly into his gold outlook. Oliver frames gold as capital — a balancing asset against expanding central bank liabilities. Historically, central bank balance sheets maintained a meaningful relationship to gold reserves. Applied to today’s far larger and more complex Fed balance sheet, he believes significantly higher gold prices would be required to restore equilibrium.

Silver presents a different angle. Much of global silver production is a byproduct of other metals, making supply relatively inflexible. Demand, driven by industrial uses and renewable energy infrastructure, is also difficult to curb. When both supply and demand are inelastic, small shifts can cause outsized price moves — a dynamic Oliver says is already visible.

He also highlighted structural stress within the physical gold market. Traders and refiners typically hedge inventory through futures markets. Rising volatility, however, has prompted banks to tighten margin requirements. Smaller participants may respond by reducing throughput or holding less inventory, constricting supply flows and amplifying price fluctuations.

Despite gold’s strength, mining equities have lagged. Oliver attributes the disconnect to conservative accounting practices and institutional skepticism that current gold prices are sustainable. Large companies often value reserves using multi-year average prices, dampening reported gains. In a full-blown mania phase, he expects valuation multiples to expand sharply as generalist capital enters the sector.

Beyond markets, Oliver paints a sobering fiscal picture. U.S. federal debt, when divided among workers rather than the total population, reaches levels he considers economically untenable. Add in long-term entitlement obligations, and the implied burden grows further. In his assessment, some form of monetary restructuring — whether inflationary, negotiated or otherwise — becomes increasingly likely over time.

He also raised concerns about the digitization of money and potential financial controls. In periods of instability, governments historically move toward tighter oversight of capital flows. Physical gold, he argues, remains one of the few assets without direct counterparty exposure.

“As we [all] know, governments have been working on digital assets,” he said. “The EU keeps dropping the price at which you can use cash … and they talk about digital currencies so that they can track every transaction economy.”

Oliver added:

“I find that amusing because if you read Vladimir Lenin, [he] talked about how banks were great. In fact, he wanted one giant bank to track every transaction in the economy so they could be controlled… and the EU, I’m not sure they know they’re quoting Vladimir Lenin, but that is exactly what they say they want to do.”

For viewers watching the interview, the message was clear: gold’s next phase may not be as smooth as the last. The quiet accumulation by central banks is giving way to a louder, more volatile era shaped by credit stress and policy limits.

Whether that transition results in a slow grind higher or a sharp repricing depends on how the private credit cycle unfolds and how aggressively the Fed responds. In Oliver’s telling, gold is already signaling that the system is under strain — and that the second act of this bull market has begun.

FAQ 🔎

- What does Daniel Oliver mean by gold’s “phase two”?He describes a shift from central bank-driven accumulation to volatility driven by U.S. credit stress and private equity refinancing risk.

- Why does Oliver believe the Federal Reserve is constrained?He argues the Fed cannot cut rates and shrink its balance sheet simultaneously without destabilizing liquidity conditions.

- How could private credit affect gold prices?Rising defaults and refinancing pressure could force monetary easing, which Oliver says gold markets are anticipating.

- Why are gold miners underperforming bullion?Oliver cites conservative accounting practices and institutional skepticism about sustained high gold prices.