NVIDIA dominates the AI chip market. But dominance doesn’t always mean the best risk-reward. With institutional money flow turning cautious, tariff headwinds on Taiwan-made chips, and a valuation demanding 60%+ sustained growth — smart money is looking at other AI stocks.

Here are three AI stocks that could offer a sharper setup, both technical and fundamental, heading into March 2026. And watch out for a high risk, honorary pick, right at the end.

How is Nvidia (NVDA) Looking?

NVIDIA, the largest holding in the Technology sector (XLK) at 15.79% weightage at press time, reports its Q4 FY2026 earnings on February 25, post-market close.

Wall Street expects high numbers, but recent history shows that hasn’t been enough. After Q3’s $57 billion beat, the stock barely moved and has traded sideways since.

NVIDIA EARNINGS: MARKET ON EDGE OVER AI OUTLOOK

— *Walter Bloomberg (@DeItaone) February 25, 2026

Nvidia reports earnings at a pivotal moment, with investors questioning the durability of the AI-driven stock rally.

Strong results are expected, but markets remain uncertain as concerns grow over heavy AI spending and disruption… pic.twitter.com/kqgGtdKfUJ

Despite being up over 50% year-on-year, NVIDIA’s chart has been trading inside a descending channel since late October. At press time, the price appears to be breaking out of this channel — but the breakout needs confirmation.

A sustained hold above $195, followed by a move through $203 and $212, would flip the structure bullish.

However, if the breakout fails, the $190 and $179 zones have acted as near-term support, with deeper downside risk below that.

The Chaikin Money Flow (CMF) — which tracks whether institutional money is flowing into or out of a stock — remains a concern.

The Chaikin Money Flow (CMF) indicator has remained below the zero line since mid-January, indicating net money continues to leave despite the price recovery.

If CMF fails to flip positive (like mid-January), the price recovery loses its institutional backing, and the descending channel could reassert itself.

On the fundamental side, NVIDIA manufactures 100% of its GPUs through TSMC in Taiwan. This fully exposes it to Section 232 semiconductor import tariffs, raising chip costs.

China’s revenue has collapsed under US export restrictions, cutting off the world’s second-largest AI market.

And at 35x EV/EBITDA (a measure of how expensive a stock is relative to its earnings power), NVIDIA needs 60%+ sustained growth just to justify its current price. With these risks in play, three other AI stocks may offer a sharper setup into March.

Taiwan Semiconductor (TSM)

TSMC (TSM), the first stock on the list, is up nearly 100% year-on-year. That outpaces even NVIDIA’s 50% gain and the reason is straightforward. TSMC manufactures over 90% of the world’s most advanced chips.

Every NVIDIA GPU, Broadcom ASIC, and AMD processor runs on TSMC fabrication. It doesn’t matter who wins the AI chip race. TSMC builds for all of them.

$TSM has a monopoly on making the most advanced AI chips by controlling over 90% of production at 3nm, 5nm & 7nm.

— Shay Boloor (@StockSavvyShay) February 14, 2026

That demand shows up in its HPC segment across:

• AI accelerators like $NVDA Blackwell & $GOOGL TPUs

• Data center CPUs like $AMD EPYC & $AMZN AWS Graviton

•… pic.twitter.com/qI7artH84C

Here’s what most investors miss. TSMC controls NVIDIA’s cost structure. It raised prices 10-20% on advanced chips recently. Customers paid without hesitation as no alternative exists.

Intel is generations behind, and Samsung has yield problems. When TSMC raises prices, its margins expand. When NVIDIA pays those prices, its margins shrink.

And unlike NVIDIA, TSMC doesn’t pay import tariffs. Tariffs hit the importer, not the exporter. TSMC exports. NVIDIA imports. Plus, TSMC’s new Arizona fabs produce US-made chips — completely tariff-free.

At 18x EV/EBITDA — a measure of price relative to core earnings — TSMC costs nearly half of NVIDIA’s 35x. Last quarter, 1,945 institutions opened new positions, worth $49 billion, one of the highest inflows among AI stocks.

On the chart, TSM trades inside an ascending channel since mid-December. A breakout, which is almost there, could target $470 — over 20% upside, starting in March itself.

CMF reads 0.21, above zero, confirming steady institutional inflow. A push past 0.28 would strengthen the breakout signal.

On the downside, $386 is critical support. A correction, likely triggered by the Taiwan-specific geopolitical tensions, could test $362 or $346. Only a sustained break below $346 turns the structure neutral.

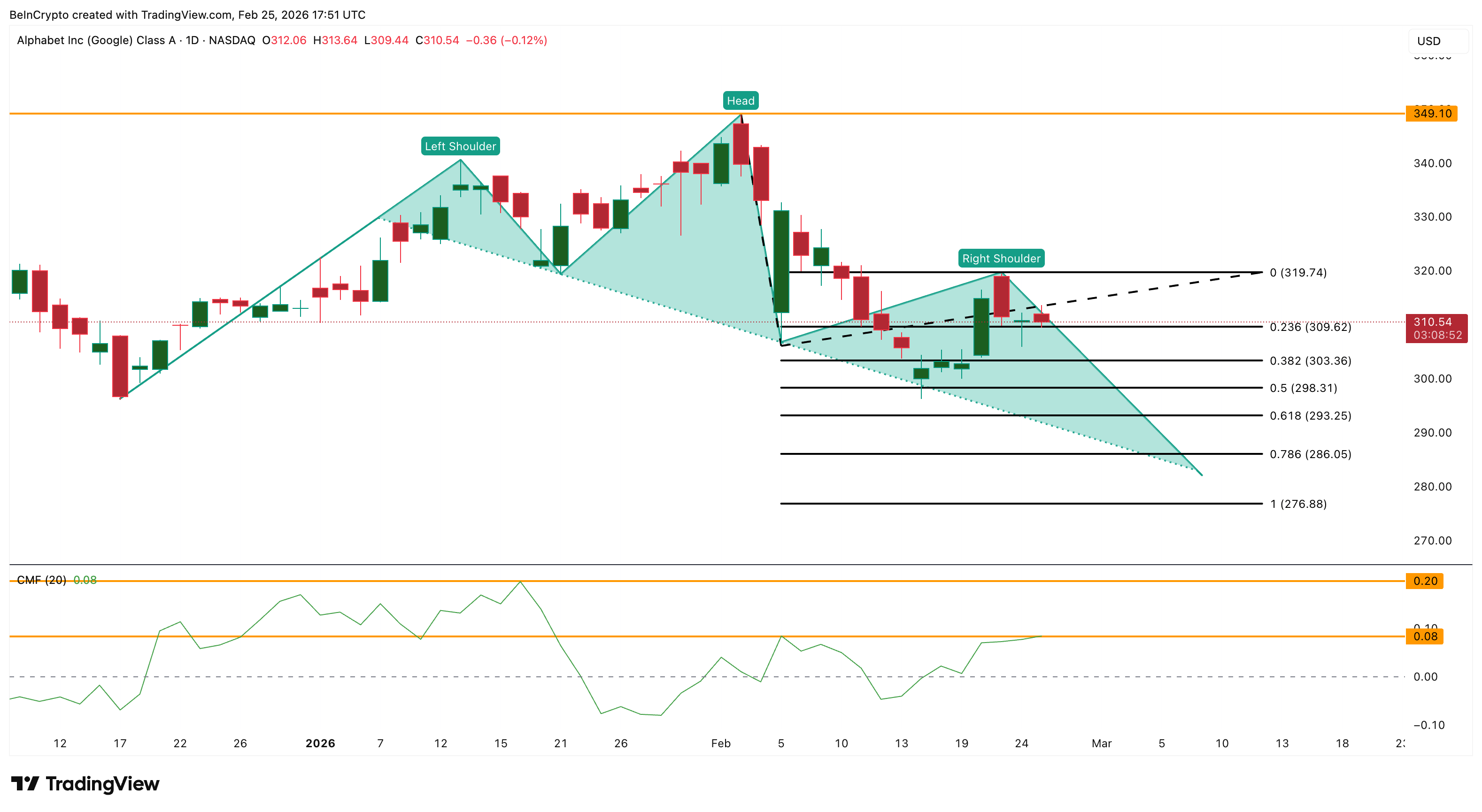

Alphabet (GOOGL)

This AI stock might throw a surprise. On the daily chart, Alphabet looks weak. It’s mostly flat year-to-date. Down 7% over the past month. The price is forming a head and shoulders pattern with a downward sloping neckline. But here’s the interesting part.

Since hitting the right shoulder on February 23, the price has tried to rebound. It now sits near the right shoulder level. A break above $319 would weaken the bearish pattern. It turns the structure neutral.

Above $349, the short-term bearish thesis gets completely invalidated.

The CMF tells a different story than the price. While NVIDIA’s CMF remains negative — showing institutional money leaving — Alphabet’s CMF has turned positive at 0.09.

Similar to TSM, money is flowing in despite the weak price action. A sustained move above 0.19 would confirm institutional accumulation is carrying into Q1 2026.

Even in the last quarter, 520 institutions opened new positions averaging $74 million each.

The fundamental edge is unique. Google doesn’t just use AI — it sells cheaper AI infrastructure to NVIDIA’s own customers. Its Ironwood TPUs cost roughly $15,000. NVIDIA’s GPUs cost $30,000-$40,000.

TPU v7 costs around $15K for Google.

— Zephyr (@zephyr_z9) November 26, 2025

Capital costs for Google are 1/3rd on TPUs compared to Nvidia hardware.

Interconnect bandwidth 600 GB/s (ICI), 1000W, 4.6 PFLOPS fp8, 192GB HBM3E.

Google can squeeze out higher MFU on TPUs due to JAX/XLA compared to Nvidia on GPUs.

(U won't… https://t.co/79Sckgy287

Google Cloud grew 48% last quarter. Operating margin jumped from 17.5% to 30.1% in one year.

$GOOG Alphabet Q4 FY25:

— App Economy Insights (@EconomyApp) February 4, 2026

• Revenue +18% Y/Y to $113.8B ($2.3B beat).

• Operating margin 32% (-1pp Y/Y).

• EPS $2.82 ($0.18 beat).

☁️ Google Cloud:

• Revenue +48% Y/Y to $17.7B.

• Operating margin 30% (+13pp Y/Y).

▶️ YouTube ads +9% to $11.4B. pic.twitter.com/sZ1VUMGzAd

And as a software and services company, Alphabet has zero tariff exposure — unlike NVIDIA’s 100%.

Tariffs generally do not apply to software services exports in the traditional sense, as they are typically imposed on physical goods crossing borders, not intangible services or digital products like software transmitted electronically.

— Navroop Singh (@TheNavroopSingh) April 2, 2025

Under current international trade…

If the price breaks below $286, the bearish pattern confirms. That could push prices toward $276 and lower levels — likely triggered by broader tech selling or disappointing Cloud growth guidance.

But the CMF divergence and institutional flows suggest smart money is positioning for a reversal, not a breakdown.

Broadcom (AVGO)

Last on the list but not the least. This AI stock is up 64% year-on-year but flat over the last seven days.

An inverse head and shoulders pattern is forming now. This is a classic reversal structure, which can change the short-term weakness. The AVGO price is now moving toward the neckline at $350.

A breakout above that level opens the path for a near 20% move — potentially pushing AVGO close to $420. That breakout window aligns with early March, right around its Q1 FY2026 earnings on March 4. A beat-and-raise on March 4 could be the trigger that cracks the neckline of the bullish pattern.

Here’s what makes Broadcom a direct NVIDIA challenger. AI is shifting from the training phase to inference — running models at scale for millions of users. NVIDIA GPUs dominate training. But for inference, custom ASICs are 3-5x more energy-efficient and cost way less.

Broadcom designs these ASICs for Google, Meta, ByteDance, and now OpenAI. As inference scales, Broadcom is positioned for the bigger phase ahead, courtesy of this AI shift.

AI ASIC and Networking Chips

— Jukan (@jukan05) June 2, 2025

Broadcom’s dominance in the AI ASIC market is striking, with over 100 chip designs completed across 7nm, 5nm, 3nm, and 2nm process nodes—firmly securing its No.1 position with over 80% market share. In the high-performance switching and routing chip… pic.twitter.com/8IS31KnCbN

The Money Flow Index (MFI) — which measures buying and selling pressure using both price and volume — confirms accumulation on dips.

Since February 10, while prices trended lower, MFI has trended higher. And that’s a bullish divergence. MFI currently sits around 67, still below the overheated 80 threshold. Room to run. This means, possibly retail is picking up AVGO shares at a clip.

On the downside, $314 is critical. A break below would weaken the bullish setup. Under $295, the inverse head and shoulders invalidates entirely. A broader AI spending slowdown or weaker-than-expected March 4 guidance could trigger that scenario.

Honorable Mention: Palantir Technologies (PLTR) — The Risky Bet

Palantir didn’t make the main list of AI stocks, courtesy of the high valuation risk.

$PLTR – CITRON'S LEFT: PALANTIR 'BEYOND OVERVALUED'

— *Walter Bloomberg (@DeItaone) August 13, 2025

Citron Research's Andrew Left is short Palantir calls the short 'obvious' likes the company and Alex Karp, but thinks it is overpriced.

But the chart is flashing reversal signals worth watching. Between February 5 and 24, the price made a lower low, yet the relative strength index (RSI), a momentum indicator, made a higher low. That’s a classic bullish divergence.

The CMF confirms it. Between February 9 and 25, prices trended down while CMF trended up. Two separate indicators pointing toward bullishness.

If $126 holds as a base, the first target is $143. Beyond that, $170 — a strong resistance from early January — becomes the key level.

Fundamentally, Palantir is one of the few AI companies turning AI into real revenue. Last quarter delivered $1.41 billion — up 70% year-on-year. It carries zero debt, $4 billion in cash, and like the three main picks, zero tariff exposure. Pure software.

Palantir reports Q4 2025 revenue growth of 70% Y/Y, rule of 40 score of 127%; issues FY 2026 revenue guidance of 61% Y/Y growth and U.S. commercial revenue guidance of 115% Y/Y growth, crushing consensus estimates.

— Palantir (@PalantirTech) February 2, 2026

Q4 U.S. commercial revenue grew 137% y/y and adjusted operating… pic.twitter.com/b7a4BVTkRo

Here’s the catch. PLTR trades at over 200x P/E — meaning investors are paying $200 for every $1 the company earns. That’s a price tag that assumes everything goes perfectly.

Any stumble in growth, and the stock could fall hard. Moreover, losing $126 invalidates the entire setup.

The post 3 AI Stocks that Can Outperform Nvidia In March 2026 appeared first on BeInCrypto.