This is a segment from the 0xResearch newsletter. To read full editions, subscribe.

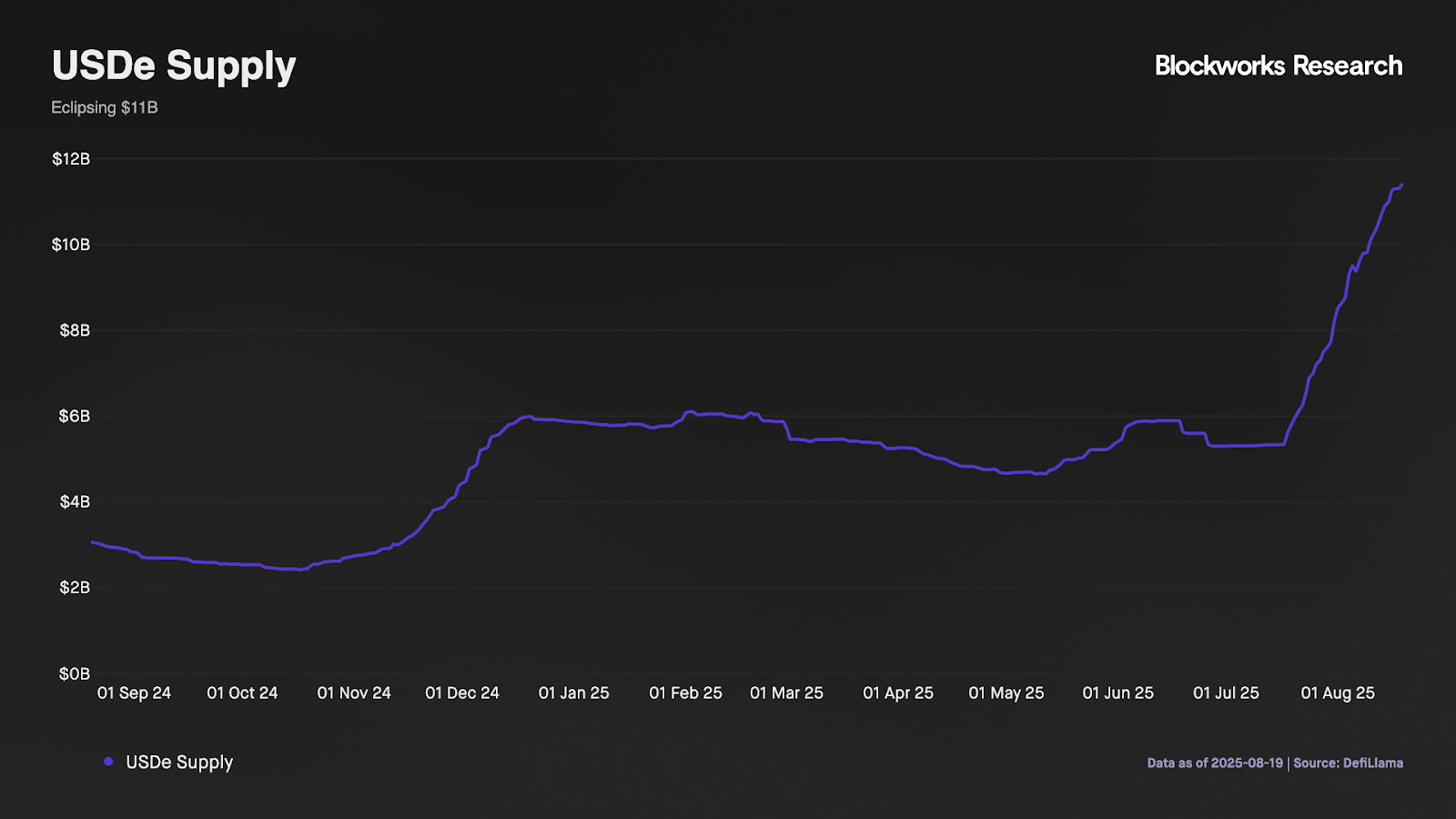

We’ve all seen the $USDe chart as of late. It’s up and to the right, now crossing $11.4 billion in circulating supply. There are a few key reasons behind this, which aren’t fully reconciled with sUSDe’s 6-9% APY.

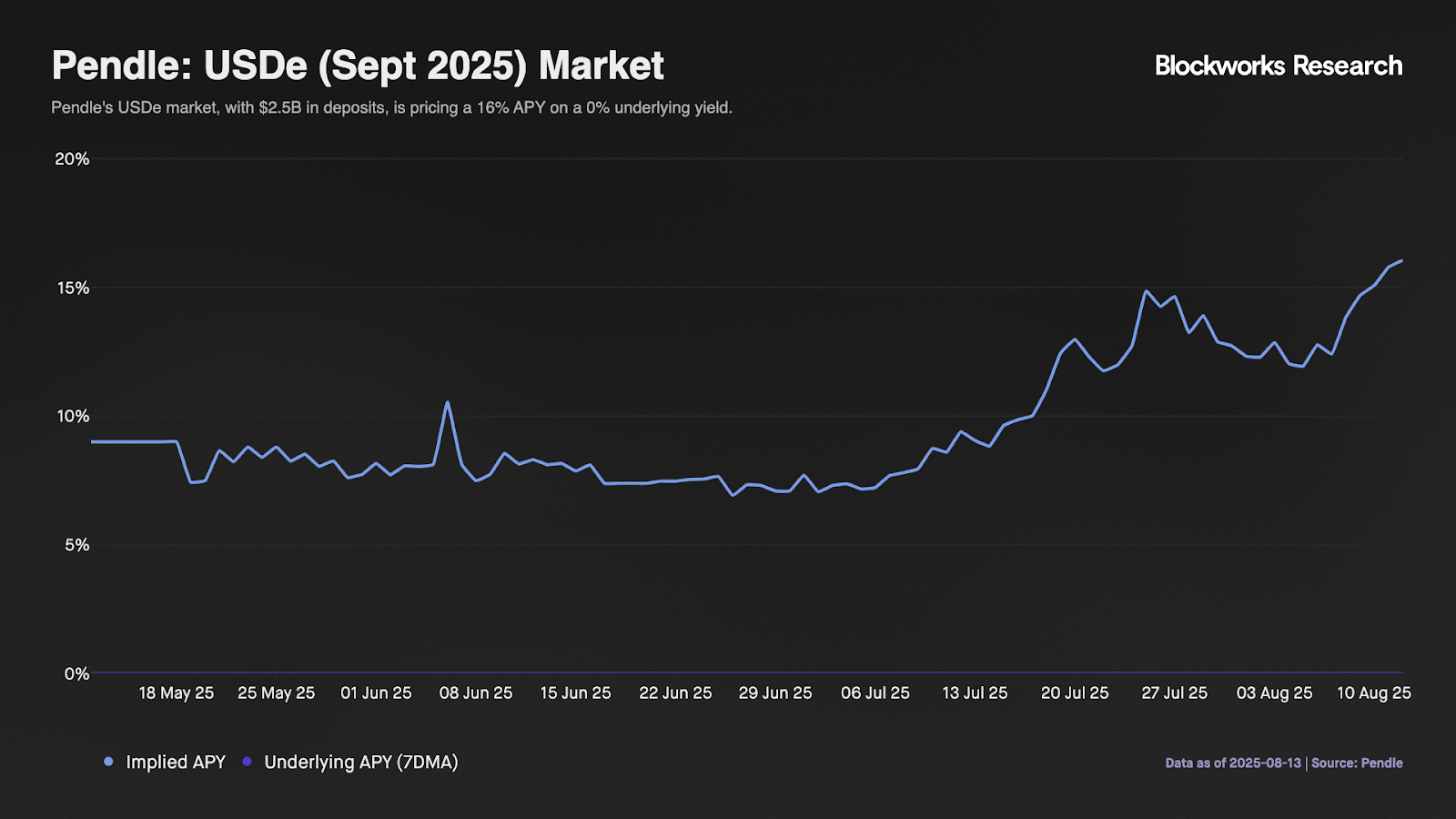

Looking under the hood, the $USDe market on Pendle for the September maturity now accounts for over $3.4 billion in $USDe, 30% of $USDe’s circulating supply.

Unlike sUSDe, $USDe itself is not natively yield-bearing, and is intended to represent the value of $1. On this Pendle market, however, $USDe liquidity receives a 70x sats boost from Ethena’s points campaign, and the YT buyers on this market are pricing the value of these sats at an implied APY of ~14%, a steep premium to the underlying APY of 0% and the benchmark yields provided by sUSDe or USDC supplied on Aave. As the price of $ENA has risen from $0.25 at the start of July to $0.67 today, the expected value of $ENA distributions from sats has risen along with this.

Herein lies the flywheel-points farming. Spend on growth with “points”, making $USDe more attractive on Pendle. The $USDe supply grows, accelerating top line metrics for Ethena. The growth in the top line leads the liquid markets to price $ENA higher, raising the expected value of $ENA distributions through points. As the market raises the implied valuation on points, the $USDe supply continues to grow to crowd out this now 14%-16% implied yield, continuing the flywheel. Over $1 billion of $USDe has been added to this market since last week.

Going one level further — as the market raises the implied valuation of the points, the fixed yield on the $USDe-type PTs is lifted as well, making them more attractive for looping. As discussed last week, these instruments have shown profound utilization rates on Aave, which now holds over $4 billion in PTs, with borrow capacity and LTVs completely maxed out. As leverage across these instruments is continually dialed up, risks of an unwind continue to amplify.