Today, enjoy the Empire newsletter on Blockworks.co. Tomorrow, get the news delivered directly to your inbox. Subscribe to the Empire newsletter.

It’s ‘Gensler Fall’

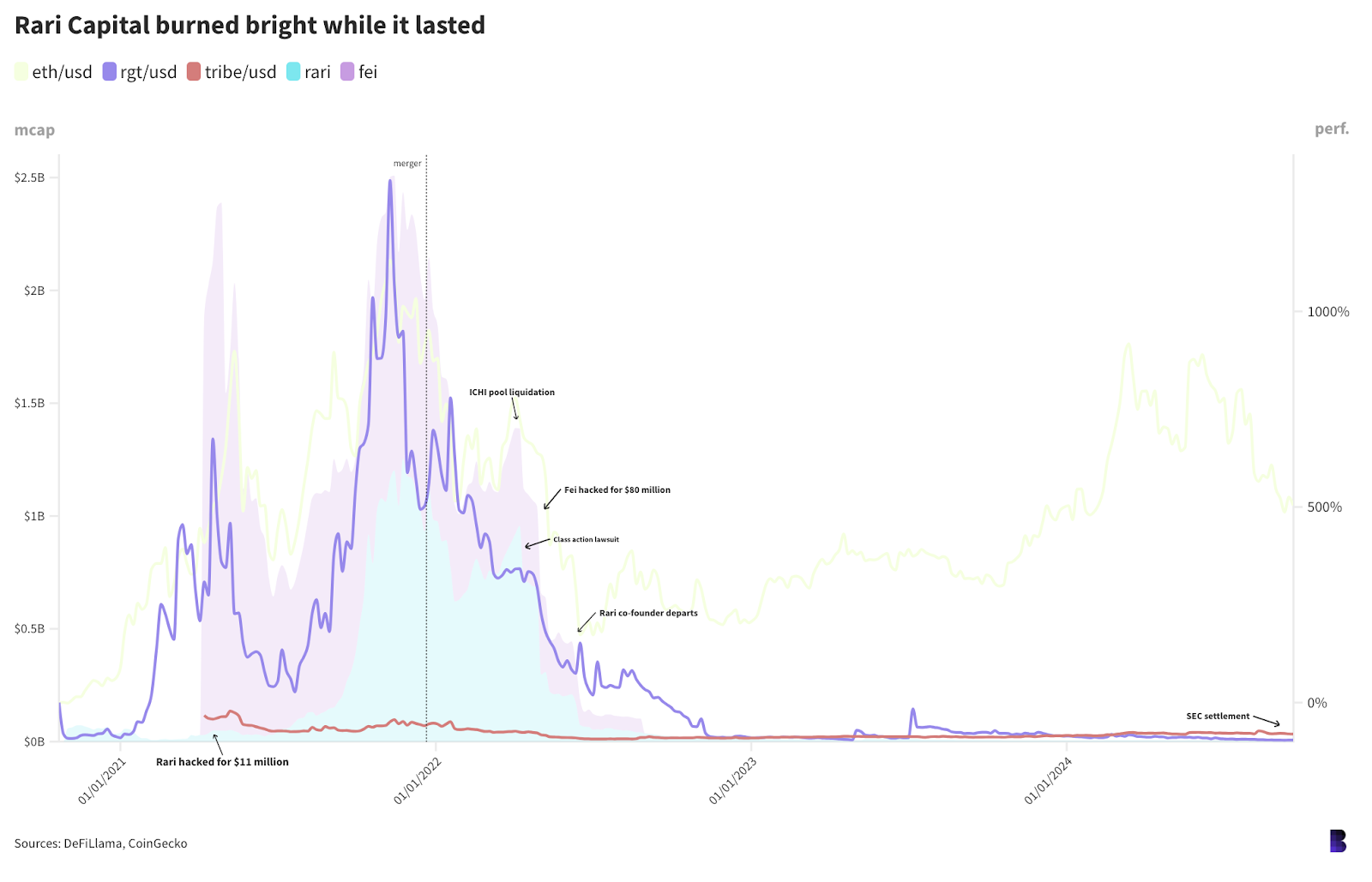

Whatever the cost of innovation, Rari Capital has footed at least some of the bill.

Both it and Fei Protocol debuted in the aftermath of DeFi Summer in 2020 — a precursor to the 2021 bull run. Yield-farming protocols had run wild, paying out hundreds of percent interest and, in many cases, driving token prices sky-high.

With so much token liquidity flowing into all sorts of pools and protocols, a tidal wave of new projects sought to enable new ways of generating yield.

Simultaneously, more centralized lending firms like Celsius, Nexo and BlockFi leveraged those same tools in their own offerings. That entanglement two years later contributed to a mess of settlements, bankruptcies and liquidations, both on and offchain.

Rari Capital embodied DeFi Summer’s scrappy spirit. Even to the point that its founders were teenagers when it was built.

Rari’s lending pools were, in essence, tools intended to remove a lot of the grunt work and anxiety around yield-farming for the regular crypto user. The protocol ran algorithms to find corners of DeFi with the highest yields — such as Curve, Compound and Aave — and deployed the pooled capital appropriately, paying out interest.

The SEC claimed the tokens used by the protocol to manage pool positions represented interest in the pools themselves. Rari’s native governance token was also flagged as a security, so the SEC’s position is that the team should’ve registered the tokens and their offerings with the regulator before they were launched — as if it could’ve launched at all under that premise.

Much of the SEC’s complaint also hinged on Rari Capital itself dogfooding its own protocol — maintaining Fuse pools and marketing the potential returns users would receive.

Although, the SEC alleged that “Rari Capital and its co-founders falsely told investors that the Earn pools would automatically and autonomously rebalance their crypto assets into the highest yield-generating opportunities available when, in reality, the rebalancing mechanism often required manual input, which Rari Capital sometimes failed to initiate.”

The agency further claimed that one-third of Earn users lost money due to network and protocol fees outweighing the yield. So, perhaps, the platform wasn’t perfect, but it was experimental and, even more critically, fairly early.

In any case, Rari Capital has already been through the wringer.

Two hacks, a class action lawsuit, a debilitating forced pool liquidation and the departure of a co-founder in the space of two years. Not to mention an ongoing lawsuit with a former employee over allegedly unpaid vested tokens, with $2.4 million in damages sought.

We don’t know how much money the Rari team forked out as part of its settlement with the SEC.

But it joins at least a dozen crypto-related companies, individuals and entities who have settled cases with regulators and other parties in the past year including Uniswap Labs, eToro, Abra, Silvergate, FalconX, Genesis, OKX, ShapeShift, KuCoin, Coinlist, which altogether paid over $126 million. Binance also settled with the DOJ this past year for $4.2 billion.

There are additional penalties for Rari, particularly five-year officer and director bars for its co-founders.

Is all that just the cost of innovation? It sure looks like it. At a minimum, it’s become the cost of doing business in crypto — at least until the more landmark cases play out in court over the next year or two.

— David Canellis

Data Center

- BTC and ETH have rallied around 6% apiece on the daily following the Fed rate cut and Trump’s bitcoin burger purchase. (BTC: $63,100; ETH: $2,450.)

- Memecoin POPCAT leads the front page with 35% gains, followed by SEI (26%), TAO (22%), TIA (20%) and SUI (17.5%).

- Aave’s total ETH locked is at its highest point August 2022: 7.96 million ETH, up from 4.4 million ETH at the start of the year.

- Ethena USDe has shed almost $1 billion supply since it peaked at over $3.6 billion in July.

- Standard BTC transactions make up 97% of Bitcoin activity right now.

Off to the races

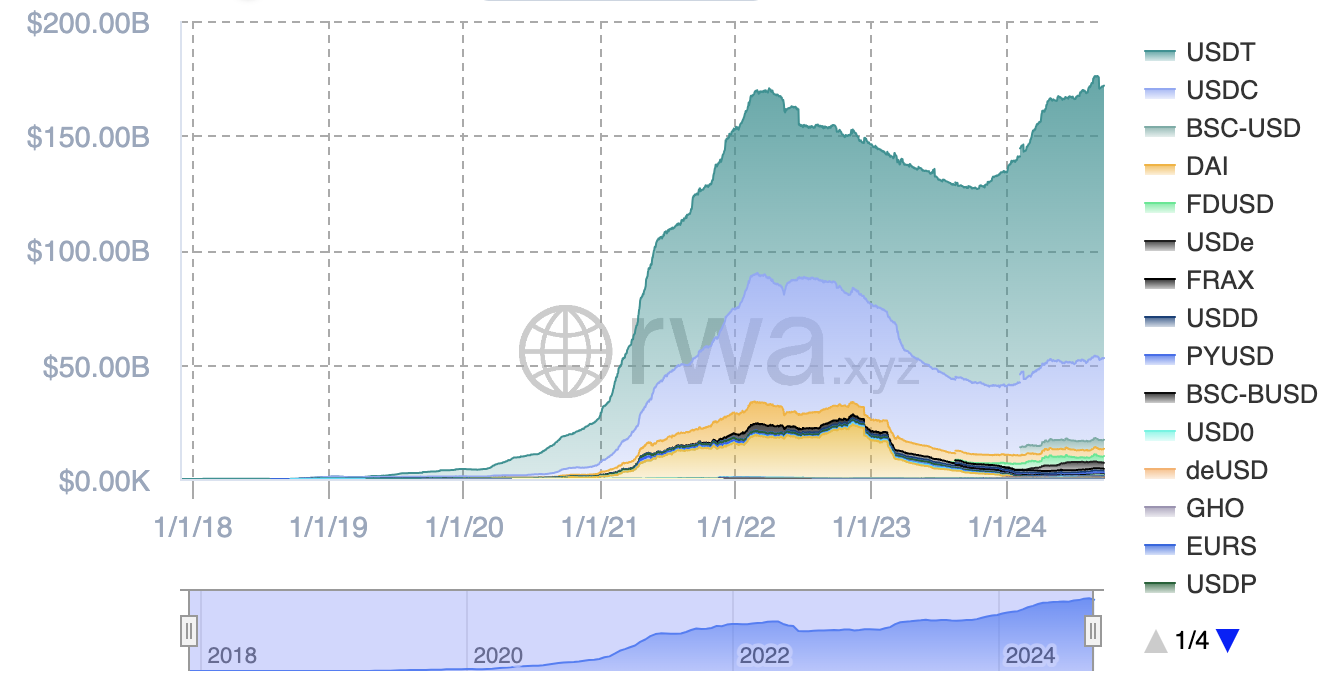

Watch out, we have some new entrants to the stablecoin market.

BitGo announced Wednesday that it planned to launch USDS, a yield-bearing stablecoin backed by Treasury bills, in January of next year. There was also a report that Revolut is plotting its own stablecoin venture, though they declined to comment.

The timing of the launches is interesting, given that we just talked about how successful stablecoins are right now. They’re sitting at a total market cap of $171 billion, slightly down over the past 30 days.

So let’s talk about BitGo.

The press release shows some spice, with BitGo saying they plan to “challenge the existing stablecoin market dynamics, specifically targeting the dominance of single-issuers like Circle and Tether.”

“…USDS introduces a novel reward system that deploys up to 98% of earnings to participants who support the ecosystem. This approach ensures that all eligible institutions, exchanges, liquidity providers, and users are incentivized to support and grow the USDS network, fostering a more inclusive and balanced ecosystem,” the release continued.

To be clear, though, institutions would be the beneficiaries of the yield. But this hits on something Nic Carter of Castle Island Ventures said last week: “…I do think that the interest-bearing stablecoins will out-compete the ordinary ones at the margin with time.”

Tether and Circle are obviously the two heavyweights in the category — shown by the green and blue areas on the chart above — but the BitGo offering would change things slightly. Though, in such a crowded space, there’s no way to tell at this point just how much consumer appetite there is for another stablecoin.

And, if we’re continuing to compare, Tether isn’t US-based, though Circle just announced that it was moving its headquarters to New York as the firm eyes a public offering.

The BitGo New York Trust Company, which is registered under a state trust charter, would issue USDS. Circle’s able to issue USDC through money transmitting licenses while Tether is not regulated here.

There’s also PayPal’s stablecoin, which sits far below both USDT and USDC on the list, but is issued by New York firm Paxos.

Carter also noted last week that he wanted to take his stablecoin study to US lawmakers and push for them to issue stablecoin regulation. Partially due to the fact that, as we noted above, he said that most stablecoin issuers are wary of the SEC to offer interest-bearing stablecoins in the US.

“We have no control or insight into how [stablecoins issuers] operate. And so if you want them to be more legible and accountable, it’d be better if we have a favorable regulatory environment,” he said. “If you want us to really benefit from them, ask some rules so that stablecoin issuers can actually issue here with confidence.”

Bring it on, USDS. Let’s see how this race plays out.

— Katherine Ross

The Works

- Germany’s Commerzbank will begin offering bitcoin and ether trading through Crypto Finance.

- The founder of Inception Capital disappeared before reappearing right as investors voted to wind down the fund, Fortune reported.

- Binance CEO Richard Teng said that the exchange saw growth in institutional and corporate investors this year.

- Bernstein says stablecoins are becoming “systematically important.”

- Former president Donald Trump treated folks to burgers at New York’s Bitcoin bar, Pubkey last night.

The Riff

Q: How historic was Donald Trump’s bitcoin burger purchase?

If we’re just looking at it from the angle of ‘has this been done before,’ then it’s pretty historic.

But I’m ready to die on one hill: We still haven’t seen any actual policy plans. A strategic bitcoin reserve sounds great, but there’s a bit of doubt being shed on the idea and it’s not wholly clear how it would be executed.

Burgers (unfortunately) don’t change a candidate’s thoughts on an issue like crypto. If we want something truly historic, then I’d rather have a presidential candidate lay out their plans to regulate crypto and ensure that the regulation-by-enforcement we’ve seen would come to an end.

In all fairness to the last point, Trump has said that he’d fire SEC Chair Gary Gensler, which is something he could potentially do. We’re hearing crickets from the Harris camp, even as her donors allegedly call for the unseating of both Gensler and FTC Chair Lina Khan.

Maybe I’m jaded, but one bitcoin burger doesn’t a crypto candidate make.

— Katherine Ross

Would’ve been much cooler if Trump actually signed the transaction himself. But he just stood there, watching QR codes being scanned. At least he watched.

Trump didn’t really have to understand what was happening. Had this been an early credit card transaction — via one of those clunky old machines from the sixties — he probably would’ve had the same look of faint bewilderment.

That’s the cool part about technology. Most of the world will only ever have abstract understandings of how it all works. Bitcoin included.

Was it a cheap, pandering photo op? You could look at it like that.

But that anyone at all is still excited about BTC being used as money, over 14 years after the ill-fated Bitcoin Pizza purchase, is a win for crypto.

— David Canellis