Today, enjoy the Empire newsletter on Blockworks.co. Tomorrow, get the news delivered directly to your inbox. Subscribe to the Empire newsletter.

Let’s BUIDL!

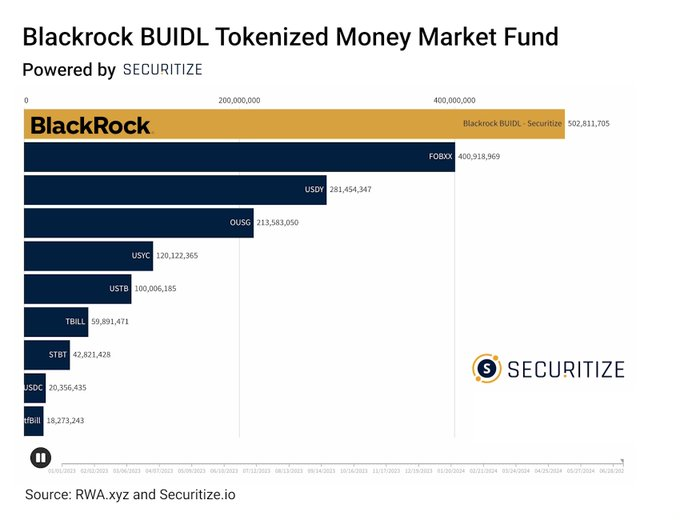

Earlier this week, BlackRock’s BUIDL crossed $500 million — a milestone never before reached by a tokenized money market fund.

Tokenized funds have really taken off in the last few years, Securitize CEO Carlos Domingo told me. We spoke at length about Securitize’s role with BUIDL (basically, qualified investors — meaning those with more than $5 million in assets — can subscribe to the fund through Securitize).

We also chatted about the growth in this particular market and what may have led to that.

Stablecoins taking off is definitely a factor, because it made folks think about what else could be tokenized, Domingo said.

Right now the total value of the tokenized treasurys market, which includes BUIDL, sits at $1.8 billion. Domingo wouldn’t be surprised to see that market cap top $2 billion soon.

While the market is obviously far smaller than the $160 billion stablecoin market, “it’s definitely growing way faster than stablecoins.”

“Keep in mind, stablecoins are easier to purchase and use because they’re permissionless. While tokenized treasuries are securities. So they have some restrictions in terms of who can purchase them, how you can transfer them, etc. So they’re never going to be, in my opinion, as big as stablecoins…but I think they can easily become 10% to 20% of the market of stablecoins,” he said.

I also asked Domingo about the conversations he’s having with others in the space, and what those have been like. He noted that they’ve really picked up since the launch of BUIDL.

“Every single asset manager out there is thinking about how they can participate,” he told me. Which is, perhaps, not surprising given the appetite for BUIDL. But that success isn’t only reserved for BlackRock.

According to rwa.xyz, Franklin Templeton’s fund, FOBXX, which was launched in April of last year, has topped $400 million — a 16% increase over the past 30 days. BUIDL, to put it in perspective, saw a nearly 9% jump in the same time period.

But Domingo thinks that BUIDL’s next $500 million could come even quicker — the fund just launched four months ago. Part of that, he added, may be because of some “new features” he teased. Some of those will be unveiled in just a few weeks.

But there’s also the fact that, because of the nature of the fund, there can be a bit of a delay when trying to subscribe to it.

He added, “In terms of onboarding entities, which, because these are institutions, it takes time to onboard an entity for them to be able to invest in BUIDL but we have a very big pipeline of entities being onboarded that once they’re on board, they will invest, right?”

The success of BUIDL has, as one would expect, led to discussions between BlackRock and Securitize about future projects. Domingo said that both firms are very aware that they’re only four months into BUIDL, so nothing else is coming at this point.

“So things take a longer time that maybe will take if we were working with a startup, which is fine because also you get the credibility of Blackrock…I think that in the next few months, we’re going to focus more on growing BUIDL in terms of the utility of the token, the functionality, and the integration with all the parts of the ecosystem, rather than launching a new” project, he said.

You know what they say: Just keep building, just keep BUIDLing…

— Katherine Ross

Data Center

- The tokenized US treasurys market has grown 50% in three months, from $1.2 billion to $1.81 billion.

- $8.04 billion is in crypto’s private credit markets, converting to 10% growth across the same period. Almost 90% is via Figure.

- BTC is eyeing an attempt at $60,000, a level not seen since July 4. It’s currently at $58,700 and about even for the day.

- TIA and NOT lead the top-100 for weekly gains, up 34% and 31% apiece, per CoinGecko.

- Solana saw its second biggest day for stablecoin inflows on record earlier this week: $261.94 million, only just short of May 2022’s peak of $272.16 million.

Stable relationship

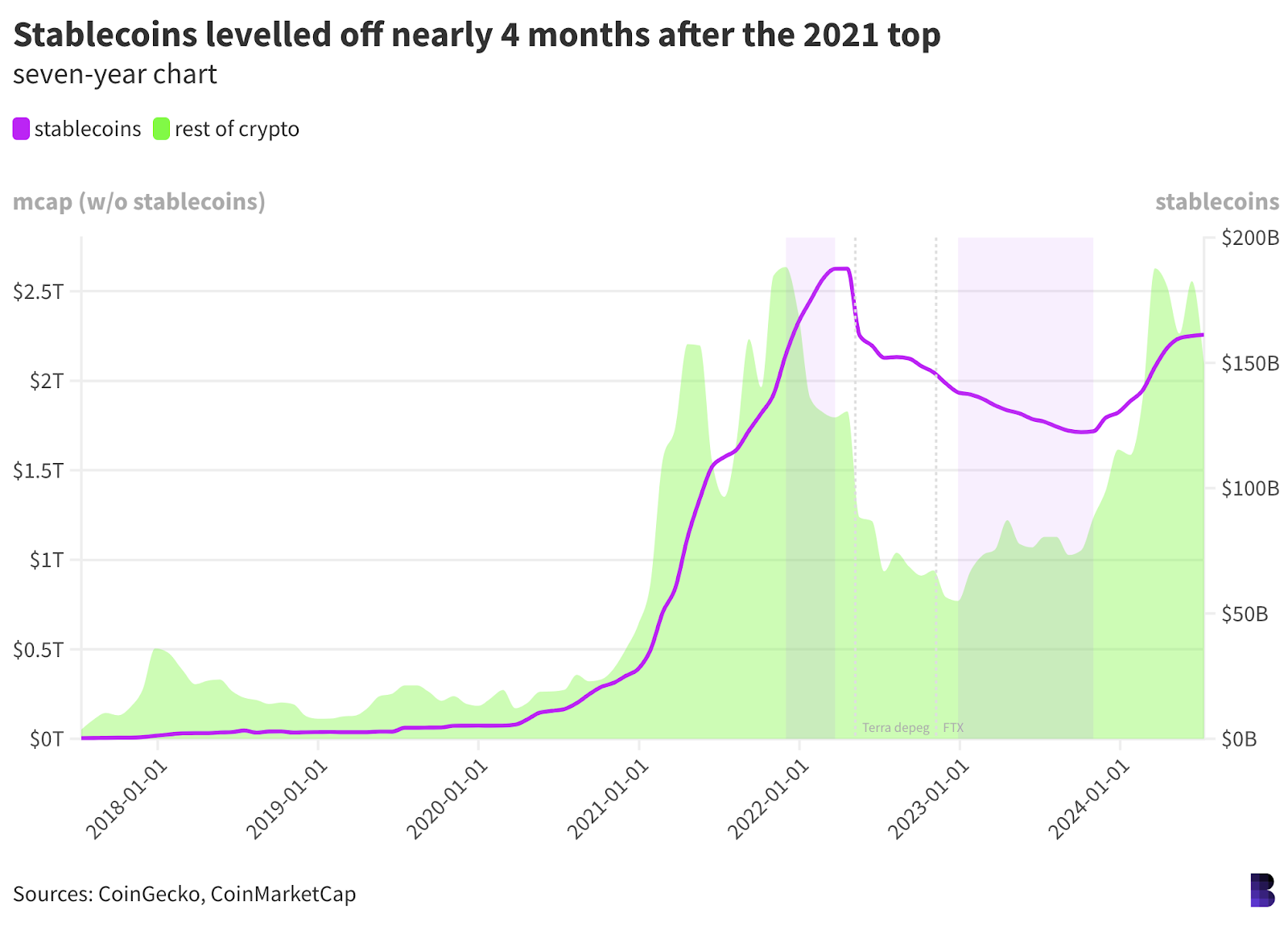

Stablecoins are self-fulfilling prophecies. As markets go up, so do their appetites for crypto dollars.

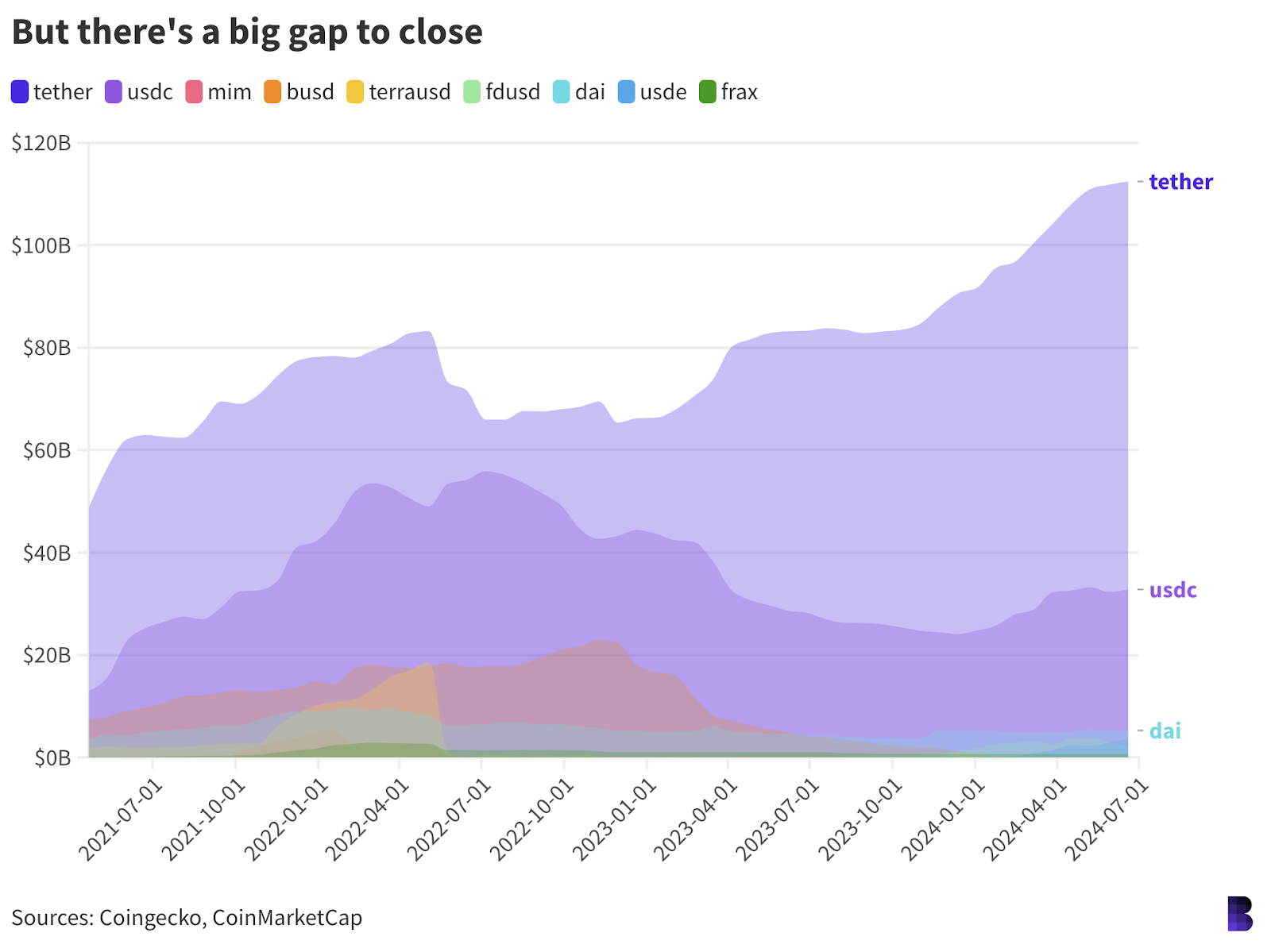

Most stablecoins have systems for minting and burning based on demand. If you saw the price of bitcoin go up and wanted a piece of the action, one might send cold hard cash to Circle in return for USDC.

Circle would mint an equal amount of USDC as dollars I’d sent in and direct them to my crypto wallet.

Likewise, if by the end of the bull market I felt like cashing in my chips, I’d send my USDC back to Circle for redemption, and the firm would pay me out an equivalent amount of US dollars and burn the supply.

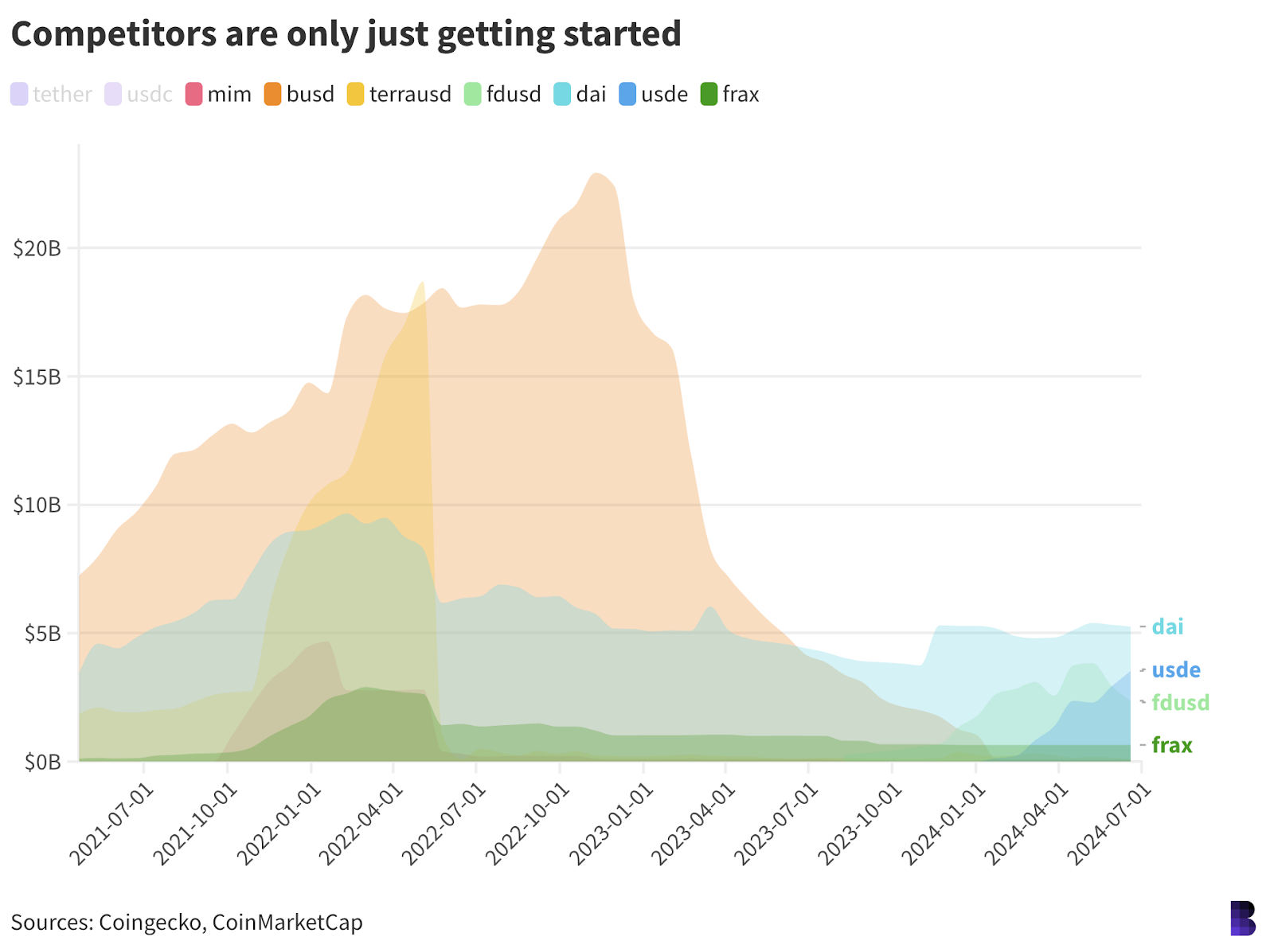

Not all stablecoins follow the same method (some, like DAI, are handled by smart contracts rather than a centralized entity).

Tether, which is still considerably larger than Circle in terms of circulating supply, may opt not to burn the supply, and rather keep to dole out to other customers upon request.

Does that make stablecoin supplies a potential metric for market sentiment? Sometimes.

Take crypto’s major run-up in early 2021. Stablecoin supplies, as shown by the purple line on the chart below, tracked the market cap of the rest of the crypto space almost to a tee.

And even when markets hit their first peak in April — the first top in green around the middle of the chart — stablecoin supplies kept growing even through the correction, indicating belief among stablecoin buyers that the market would continue going up.

Granted, the doomed algorithmic stablecoin TerraUSD was responsible for much of that supply growth around that time, and it would go on to crash spectacularly around four months after crypto hit its cycle top.

But there was still a lag between markets peaking late 2021 and stablecoin supplies reaching their max, just before Terra blew up. Some predicted it would happen while others were blindsided.

The global stablecoin supply shrank from about $156 billion directly following Terra’s demise to $137 billion as crypto bottomed when FTX went kaput six months later, a period which included Tether’s historic $16 billion ‘bank run.’

But as crypto started its recovery — one that eventually transformed into our most recent bull market — stablecoin supplies continued to fall for another year, slipping another 10% to $122 billion.

Meanwhile, crypto’s total market cap had nearly doubled (see the second shaded area on the first chart).

Right now, stablecoin supplies overall are trending sideways, and have so for the last month as crypto consolidates.

What does that say about sentiment?

“Let’s wait and see.”

— David Canellis

The Works

- BitMEX admitted to violating the US Bank Secrecy Act, the Department of Justice said Wednesday.

- A new marketplace heavily used by scammers in South East Asia is tied to Cambodia’s ruling family, Elliptic alleged in a blog post.

- MoonPay is looking to expand in the United Kingdom, Bloomberg reported.

- The bankruptcy estate of FTX is challenging Jump Trading subsidiary Tai Mo Shan’s multi-million dollar claim.

- MicroStrategy announced a 10-for-1 stock split.

The Riff

Born-again crypto enthusiast and presidential contender Donald Trump is headed to the heart of Bitcoinlandia with a speaking appearance at the Bitcoin 2024 conference in Nashville next month.

Whispers that Trump might appear have circulated for some time. It’s the latest step in Trump’s very successful efforts to court the checkbooks — and votes, one assumes — of the American crypto industry.

At this point, one wonders whether the remarks will amount to more than a victory lap. With Joe Biden’s campaign disintegrating mid-air and US crypto companies fully committed to playing the Washington money game, all Trump needs to do is highlight the GOP platform’s pro-crypto section and call it a day.

Still, the moment is undeniably historic. While crypto conferences have for years attracted would-be US presidents, Trump is the first one with an actual shot at the White House (albeit for a second time).

Would Trump be rolling into Nashville were it not for the crypto industry’s enthusiastic support? Who’s to say.

— Michael McSweeney