Disclaimer

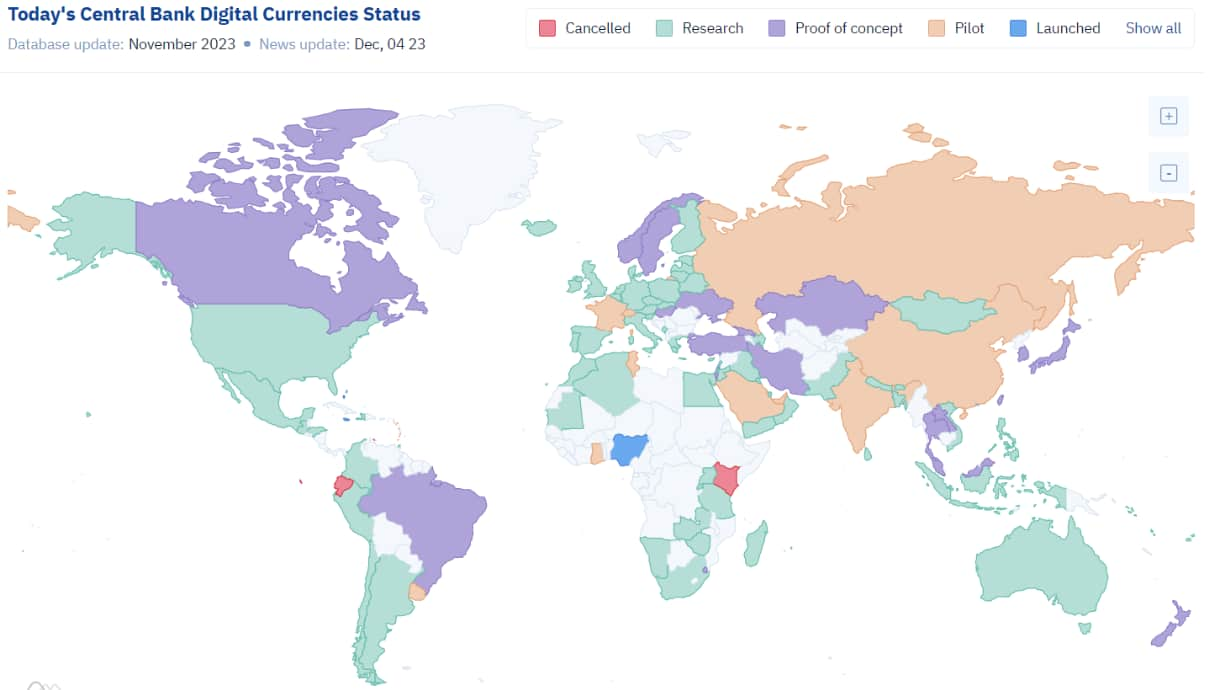

Central Bank Digital Currencies (CBDCs), are one of the major topics this year; not just in the world of traditional finance, but also in the blockchain and cryptocurrency industry, where discussions about upcoming implementations are gaining momentum.

CBDCs, digital iterations of a country’s fiat currency issued by the central bank, are touted by supporters as potential tools for enhancing financial inclusion, security, and stability. And yet, despite ongoing research and pilot programs in numerous countries, concerns persist about their implications concerning breaches into individual freedoms, especially in contrast to privacy coins.

While CBDCs are controlled by central banks and might not offer the privacy one would expect, decentralized privacy coins are using technologies that obfuscate transaction details and can not be traced back.

The International Monetary Fund (IMF) recently urged governments to ‘pick up speed’ regarding CBDC development, suggesting a potential shift toward CBDCs becoming the norm in the medium term. However, alongside the many supposed advantages cited by central banks and governments, there are notable drawbacks, with a primary focus on the extent to which CBDCs safeguard users’ privacy.

Depending on the type and implementation of the CBDC, central banks could gain deeper insights into the spending behaviour of citizens. CBDCs also make it possible to implement spending limits or rules on what exactly they can be spent on.

Different Types of CBDCs

Designed to be the digital counterpart of a country’s fiat currency, CBDCs are to be used as legal tender. Despite being conceived in response to the growing popularity of cryptocurrencies, CBDCs do not inherently rely on a blockchain or consensus mechanism. Make no mistake: Unlike cryptocurrencies, a CBDC will never be decentralized, but always in the control of a central entity.

In general there are three types of CBDCs. First, there are Retail CBDCs, accessible via digital wallets, intended for general public use in daily transactions. Second, Wholesale CBDCs, which are designed for institutional use and are supporting high-volume transactions like interbank transfers. Last but not least, Hybrid CBDCs, a mix between the retail and wholesale type.

It is to be expected that different countries will choose different approaches in the beginning, running pilots for different types, to determine the advantages and disadvantages for each.

CBDCs: Are They A Threat To Financial Privacy?

CBDC critics often mention potential privacy-issues; the risk that central banks gain even more control of the monetary supply, including the ability to monitor accounts and transactions of the citizens. It comes as no surprise then that some people are skeptical, and see through the plans of banks and regulators to destabilize cryptocurrencies as to not have their power monopoly threatened.

For example, CBDCs will have programmability, meaning there could be expiry dates or spending restrictions.

Worldwide usage of retail CBDCs might grow financial surveillance further and further. When the people in charge, such as Christine Lagarde, President of the European Central Bank (ECB) promises you a privacy-respecting digital Euro, what she means is that information is only shared with the central bank, regulators and potentially other intermediaries – so, everyone except the public.

Privacy: Is Bitcoin The Answer To CBDCs?

Financial privacy is essential when it comes to exercising basic fundamental human rights, because in order to practise them, money is needed to pay for goods and services. Take for example:

Freedom of speech: Creating a website, advertising a book, and paying graphic designers.

Freedom of assembly: Paying for train tickets to go to a demonstration, book a hotel room, get a taxi, or a train ticket.

If one is unable to pay for certain goods or services then it means that freedom rights are getting taken away. They are also getting taken away when your name is connected with a specific transaction that, according to your government, is not ‘acceptable’ and could lead to further financial restrictions being imposed.

The original Cypherpunk idea of a decentralized, private digital currency, unfortunately got lost over the past years. While Bitcoin can be called a success in itself, it is not the answer to CBDCs, as it is not anonymous, just pseudonymous. Transactions can be traced back to its origin, through Know Your Customer (KYC) and Anti-Money Laundering (AML) measures that ensure that the wallets can be tied to real identities.

In addressing these concerns, one can argue for the relevance of privacy coins, such as Monero (XMR), which incorporate advanced features like stealth addresses, ring signatures, and RingCT to ensure transaction data remains confidential. This ensures that the identities of all participating actors are dissociated and untraceable, thus protecting the users’ financial privacy far more thoroughly than Bitcoin.

Critics often complain about the use of privacy coins by criminals. However, statistics clearly show that FIAT currencies such as the US dollar play a much greater role in the criminal milieu; the new Binance CEO Richard Teng referred to an analysis according to which the US dollar is used 100 times more for criminal purposes than cryptocurrencies. And privacy coins only account for a fraction of this proportion.

The question for both sides, project teams and regulators/exchanges, is to what extent privacy coins are compliant with regulations. In recent years, several such coins have already been delisted from centralized exchanges.

Conclusion: We Need Privacy Coins

In conclusion, the importance of financial privacy as a fundamental human right cannot be overstated. As the world moves toward dystopian scenarios where all transactions are logged and evaluated, awareness of anonymity-enhancing technologies, especially privacy coins, becomes crucial in preserving the freedom to transact securely and privately.