Executive Summary

Stablecoins – digital currencies pegged to traditional assets – have driven crypto adoption by mitigating volatility and facilitating access to digital assets. Representing 11% of the crypto market, leading stablecoins USDT, USDC, and BUSD have remained stable over the long term, despite the downfall of some algorithmic stablecoins.

| Stablecoins | Highest Rate (and where) | Lowest Rate (and where) |

| USDT | 157.88% (Kucoin) | 0.78% (Vesper) |

| USDC | 12.40% (Vesper) | 1.40% (Aave) |

| DAI | 8.20% (Coinloan) | 1.02% (Aave) |

| BUSD | 8.20% (Coinloan) | 2.54% (Binance) |

| USD Savings | Highest Rate (and where) | Lowest Rate (and where) |

| 1-Year CD | 5.15% (Limelight) | 0.02% (Industrial Bank) |

| 3-Year CD | 5.39% (Merchants Bank of Indiana) | 0.04% (PNC Bank) |

| 5-Year CD | 5.00% (All in Credit Union) | 0.03% (Bank of America) |

| Bank Savings | 5.05% (Customers Bank) | 0.01% (Webster Bank) |

| Money Market | 5.02% (CFG Bank) | 0.01% (PNC Bank) |

Acting as a vital link between traditional finance and the crypto space, stablecoins have fueled the expansion of the decentralized finance (DeFi) sector. Although stablecoins and fiat currencies have distinct roles, their combined use fosters a more versatile and interconnected global financial landscape.

In this analysis, we explore the impact and significance of stablecoins in the evolving financial landscape, comparing them to traditional fiat currencies. We also discuss their potential role as a global reserve currency and examine how they contribute to a more diverse and technology-oriented global financial ecosystem.

A Brief History of Stablecoins

Stablecoins are blockchain-based digital currencies or tokens designed to have their value linked to a traditional fiat currency, commodity, or collection of assets.

In most instances, a stablecoin mirrors the value of a particular fiat currency, with the US dollar being by far the most prevalent. Generally, stablecoins maintain a 1:1 backing ratio with their corresponding fiat. The main goal of these tokens was initially to mitigate the high volatility of cryptocurrencies, though they’ve taken on a number of other important roles.

Stablecoins have significantly contributed to the adoption of crypto assets among institutional and retail investors due to their near-elimination of volatility while offering effortless access to various digital currencies and assets. They have served as a connecting point or gateway between traditional finance and the crypto ecosystem, facilitating seamless on-ramp and off-ramp systems for investors.

Also, they have been the driving force behind the exponential growth of decentralized finance (DeFi), one of the most important trends in blockchain.

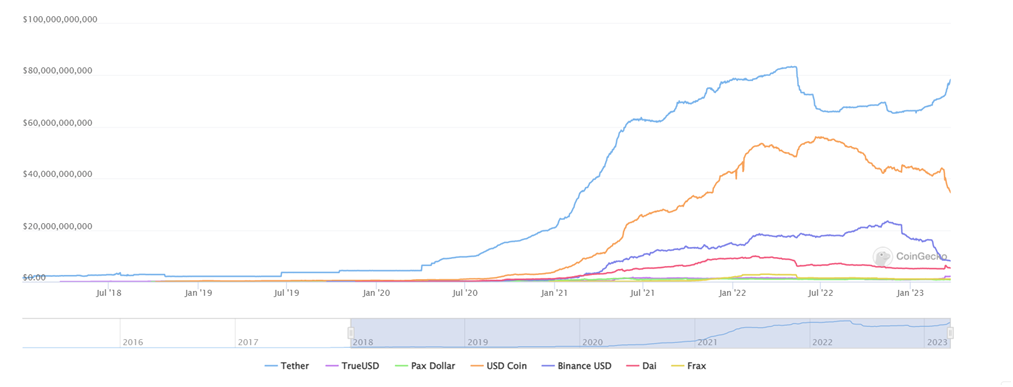

As of this writing, the top three stablecoins by market cap are USDT, USDC, and BUSD. These three stablecoins rank among the top 15 largest cryptocurrencies, collectively representing about 11% of the entire crypto market, with a total market cap exceeding $120 billion as of this writing.

The stablecoin boom came in 2020-2021, along with the DeFi craze, when the combined market cap increased from less than $7 billion in March 2020 to over $60 billion in March 2021. It exceeded the $180 billion mark in March 2022, surging 2,500% in 2 years.

The success of stablecoins lies in their ability to combine the stability and liquidity of traditional currencies with the distinctive characteristics of blockchain technology, such as decentralization, security, speed, and transparency. These tokens can be integrated into conventional finance use cases like payments, international transactions, and remittances.

While the dramatic collapse of several algorithmic stablecoins, like Terra USD (UST), has cast a negative light on the crypto market, fiat-collateralized and crypto-collateralized stablecoins have demonstrated their resilience despite the recent crisis of USDC.

Stablecoin Pros and Cons

| Pros/Benefits | Cons/Risks |

| Stablecoins nearly eliminate volatility, which has been a major problem for the crypto market. | Algorithmic stablecoins rely on smart contracts to manage their peg and are prone to smart contract bugs, hacks, or market manipulation. The collapse of UST is a relevant example of how algorithmic stablecoins can fail. |

| They provide liquidity in the crypto market, facilitating easier trading, investing, and conversion between digital currencies and fiat. | Fiat-collateralized stablecoins rely on centralized entities to maintain their peg, which contradicts the decentralization principle of cryptocurrencies. |

| Stablecoins act as a bridge between traditional finance and the crypto ecosystem, enabling seamless on-ramp and off-ramp systems for investors. | There is still a regulatory vagueness in many jurisdictions regarding stablecoins. |

| Stablecoins offer faster and cheaper cross-border transactions compared to traditional financial systems. |

Fiat Currencies

Fiat currencies are government-issued legal tender that is not backed by a physical commodity like gold or silver. Instead, their value is derived from the trust and confidence people have in the stability of the issuing government and its economy. The US Dollar (USD), Euro (EUR), Japanese Yen (JPY), and British Pound (GBP) are examples of fiat currencies. They are predominantly used as a medium of exchange for goods and services, a store of value, and a unit of account.

Fiat currencies play a crucial role in the global economy, as they facilitate trade and commerce both domestically and internationally. They are used in everyday transactions, such as buying groceries, paying bills, or settling debts, as well as in more complex financial transactions, like investing, lending, and borrowing.

Central banks are responsible for issuing and regulating fiat currencies. They rely on monetary policy tools, such as interest rates and open market operations, to control the money supply and maintain price stability within their respective economies.

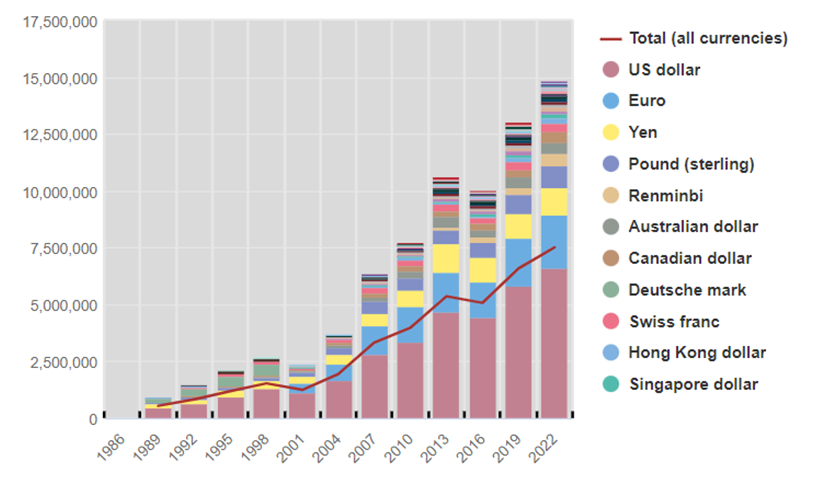

In recent years, digital payment methods have become omnipresent, leading to a decline in the use of physical cash. For a better perspective, the M0 supply, which includes banknotes, coins, and bank reserves, was $5.3 trillion as of January 2023 versus M2’s $21 trillion, which also includes marketable securities and other bank deposits.

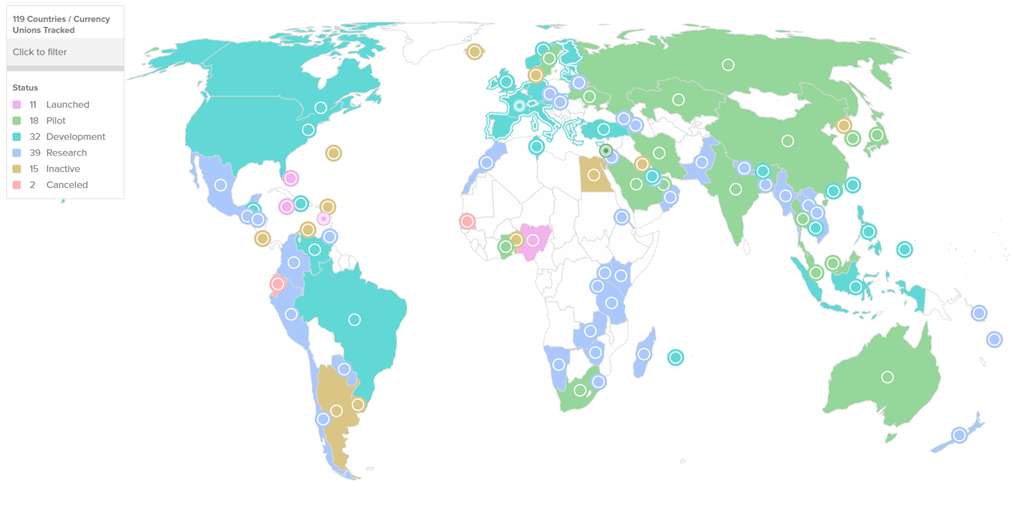

The shift towards digitization has prompted central banks to explore the development of so-called Central Bank Digital Currencies (CBDCs) inspired by stablecoins. CBDCs are digital forms of fiat money issued on a permissioned blockchain, i.e., on a private network controlled by central bank members.

CBDCs aim to provide a secure, efficient, and cost-effective alternative to existing payment systems while maintaining the stability and trust associated with fiat currencies. However, many economists are worried about privacy issues and the fact that CBDCs make banks unnecessary, leading to the centralization of the economy.

As of today, over 100 countries are exploring the benefits and features of CBDCs, including the US.

CBDCs have the potential to transform the financial landscape by offering several benefits, such as faster and cheaper cross-border transactions, increased financial inclusion, and improved monetary policy implementation.

Fiat Currency Pros and Cons

| Pros/Benefits | Cons/Risks |

| Fiat currencies are universally accepted for transactions, making them the default medium of exchange. | The value of fiat currencies can be eroded over time due to inflation, resulting in a decrease in purchasing power. This drawback is spilled over to stablecoins as well, due to the 1:1 peg. |

| Fiat currencies are available in physical form, which can be convenient for in-person transactions. | Fiat currencies are controlled by central banks, which may lead to the potential for misuse, corruption, or political interference. |

| Fiat currencies are issued and regulated by governments, providing a sense of trust and security to users. | Fiat currencies are vulnerable to counterfeiting, which can undermine their value and trustworthiness. Also, storing and handling physical currency can be cumbersome. |

Stablecoins vs. Fiat Currencies: Investor Use Cases

Investors can use stablecoins in several ways to take advantage of the unique opportunities offered by the crypto space.

- Stablecoins are a gateway to the blockchain world, acting as a bridge between the traditional financial system and cryptocurrencies.

- They enable investors to increase or reduce exposure to crypto coins like bitcoin without fiat interaction. This allows investors to speculate on the price of cryptocurrencies while leveraging the risk management benefits of stablecoins.

- Stablecoins have become an integral part of the rapidly growing DeFi ecosystem, where investors can access various financial services, such as lending and borrowing, without intermediaries like banks.

- Blockchain lending platforms enable users to lend their stablecoins to earn interest or borrow against their existing crypto holdings. The interest is usually higher than the yield offered by traditional savings accounts.

U.S. Dollar: The Global Reserve Currency

The US dollar has enjoyed its status as a global reserve currency since the Bretton Woods agreement in 1944, when 44 countries agreed to form a new foreign exchange system centered around the USD, which was linked to gold.

Even after the USD lost its gold peg in 1971 and became a floating currency, the greenback has maintained its global reserve status thanks to US foreign policy initiatives, such as convincing Saudi Arabia and eventually other oil-producing countries to sell their oil exclusively for USD.

According to data from the Bank for International Settlements (BIS), the USD has been involved in about 88% of all foreign exchange transactions during the last decade.

Could a Stablecoin Become a Global Reserve Currency?

Today’s tectonic geopolitical changes increase the possibility of the US dollar gradually losing its reserve status, especially as Russia and China are planning to dethrone it.

Can a stablecoin manage to replace the USD as the next global reserve currency? Unlikely. Such claims were popular at the peak of UST, but its collapse has silenced such ambitions.

The more likely scenario is that another fiat, a CBDC, or a basket of fiat or CBDCs become the next standard of global reserves.

Investor Takeaway

Stablecoins and fiat currencies are complementary financial instruments, each serving a distinct purpose in the world of finance. Stablecoins, with their near-elimination of volatility, act as a gateway to the crypto ecosystem, enabling seamless on-ramp and off-ramp systems for investors. They have been instrumental in driving the growth of decentralized finance (DeFi), crypto payment systems, and other use cases.

On the other hand, fiat currencies are universally accepted and regulated by governments, providing trust and security in everyday transactions. The emergence of Central Bank Digital Currencies (CBDCs) highlights the ongoing convergence between traditional finance and the digital realm, offering potential improvements to cross-border transactions and monetary policy implementation.

Stablecoins and fiat currencies serve different purposes, but together they contribute to a more diverse and interconnected global financial ecosystem.

FAQs

Some questions you may want to consider before adding stablecoins to your own portfolio:

Where to buy, sell and exchange stablecoins?

Stablecoins can be traded on centralized exchanges, such as Coinbase or Binance, as well as decentralized exchanges (DEXs), such as Uniswap or Curve.

How often are the reserves audited and how transparent is the reporting?

It differs by issuer. For example, Circle, the entity behind USDC, has its reserves audited by a third party on a monthly basis. The company switched from Grant Thornton to Deloitte in January 2023.

What’s the market cap and circulating supply?

The market cap of about 100 stablecoins tracked by DeFi Llama is over $133 billion as of this writing.