Banks are increasingly turning to tokenized deposits as they adopt blockchain technology to improve how money moves through the financial system. A new report from Arkham Intelligence says regulated banks are creating digital versions of customer deposits that stay on the banks’ balance sheets while operating on blockchain networks.

This transition helps banks make transactions faster and more automated without disrupting the essential architecture of conventional banking. In contrast to stablecoins, tokenized deposits remain liabilities of the bank and are regulated under banking regulations.

What Tokenized Deposits Actually Do

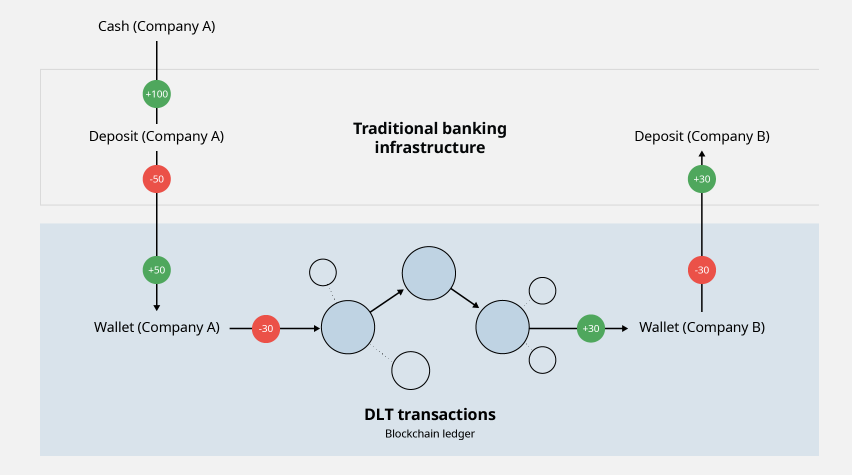

Tokenized deposits are digital versions of bank deposits that run on blockchain networks. While the deposits remain with regulated banks, customers receive digital tokens that represent the same value. This lets banks and businesses move money faster than traditional payment systems, which often depend on banking hours and take longer to settle transactions.

The technology also allows banks to automate payments based on pre-agreed conditions. For example, a company can transfer funds between its subsidiaries at any time or release payments automatically after an invoice is approved or a liquidity target is reached.

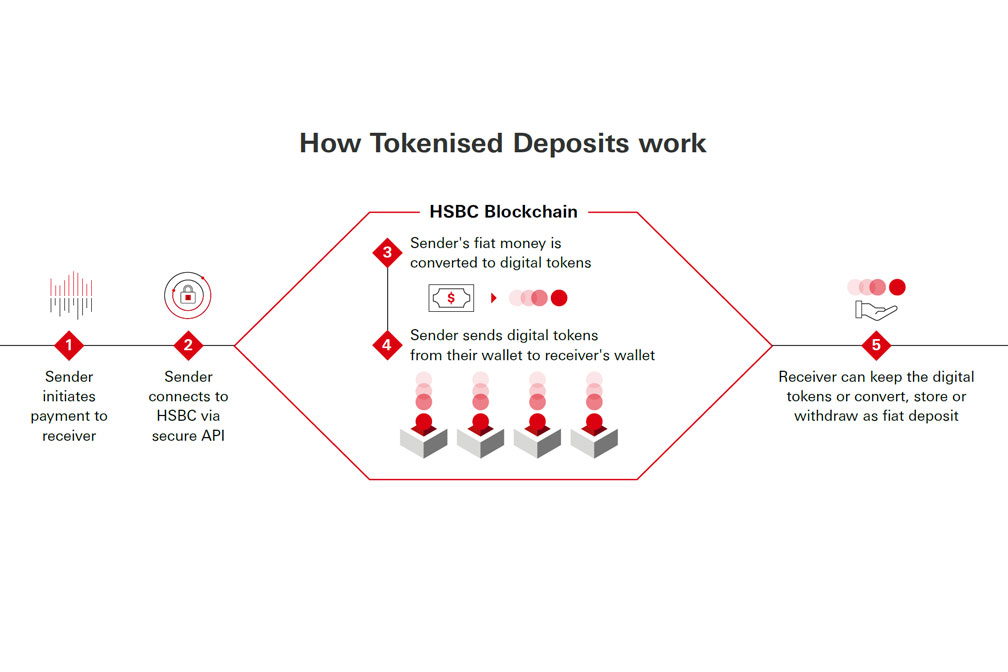

HSBC demonstrated how the technology works in September 2025 when it completed its first cross-border tokenized deposit transaction between Hong Kong and Singapore for Ant International. The transaction reduced delays caused by different time zones and helped the company manage its treasury operations more efficiently.

Why They Differ From Stablecoins

Tokenized deposits are often compared with stablecoins because both use blockchain technology to move digital money. However, Arkham Intelligence said the two work very differently.

Stablecoins such as USDT and USDC are issued by private companies that back their tokens with reserve assets. The total outstanding supply of USD-backed stablecoins so far has climbed to almost $300 billion by mid-2026, according to data from rwa.xyz.

Tokenized deposits, by contrast, are issued by regulated banks and represent customer deposits already held by those institutions. They are also available only to approved clients through permissioned blockchain networks.

A report dated February 2026 by the New York Fed emphasized that stablecoins are intended to function as “safe money,” whereas tokenized deposits will be part of the conventional banking system and help with bank loans.

Major Banks Push Industry Adoption

Big global financial institutions have launched tokenized deposits systems as they continue to adopt blockchain technology. Some of the big players in the industry include JPMorgan via its Kinexys system that was formerly called Onyx. The Kinexys system has conducted more than $7 billion worth of transactions daily with over $3 trillion being processed from its inception.

HSBC has extended its tokenized deposits to the regions of Hong Kong, Singapore, UK, Luxembourg, and US. The system offers support for different currencies and allows for automated payment and settlement of tokenized deposits.

Another player who joined the industry in January 2026 is BNY Mellon with the launch of its tokenized deposits product targeting institutions. It has also invested in blockchain infrastructure while undertaking projects related to tokenized money market funds.

Challenges Still Need Solutions

Despite the growing popularity of tokenized deposits, the technology faces some hurdles. Platforms are currently being run within one bank’s ecosystem, and tokenized deposits cannot be transferred from one financial institution to another without leaving the system. In order to solve this problem, The Clearing House intends to introduce a common network for tokenized deposits by the first half of 2027.

The International Monetary Fund said the impact of tokenization is likely to extend far beyond payments. Tobias Adrian, Director of the IMF’s Monetary and Capital Markets Department, said future policy decisions will determine whether tokenization makes the financial system more efficient or creates new fragmentation.

Related: $60B Tokenized RWA Market Shows No On-Chain Activity, Report Finds