Bitcoin is entering a period where macro sequencing matters more than narrative.

Equity markets are trading near record valuations, real yields remain elevated, and credit markets are expanding into increasingly opaque corners of the financial system. None of these conditions guarantees an imminent break. But together they form the backdrop for what could become a high-volatility window for risk assets.

For Bitcoin, the key question centers on whether stress emerges in the financial plumbing beneath elevated asset valuations and how quickly policymakers move to contain it.

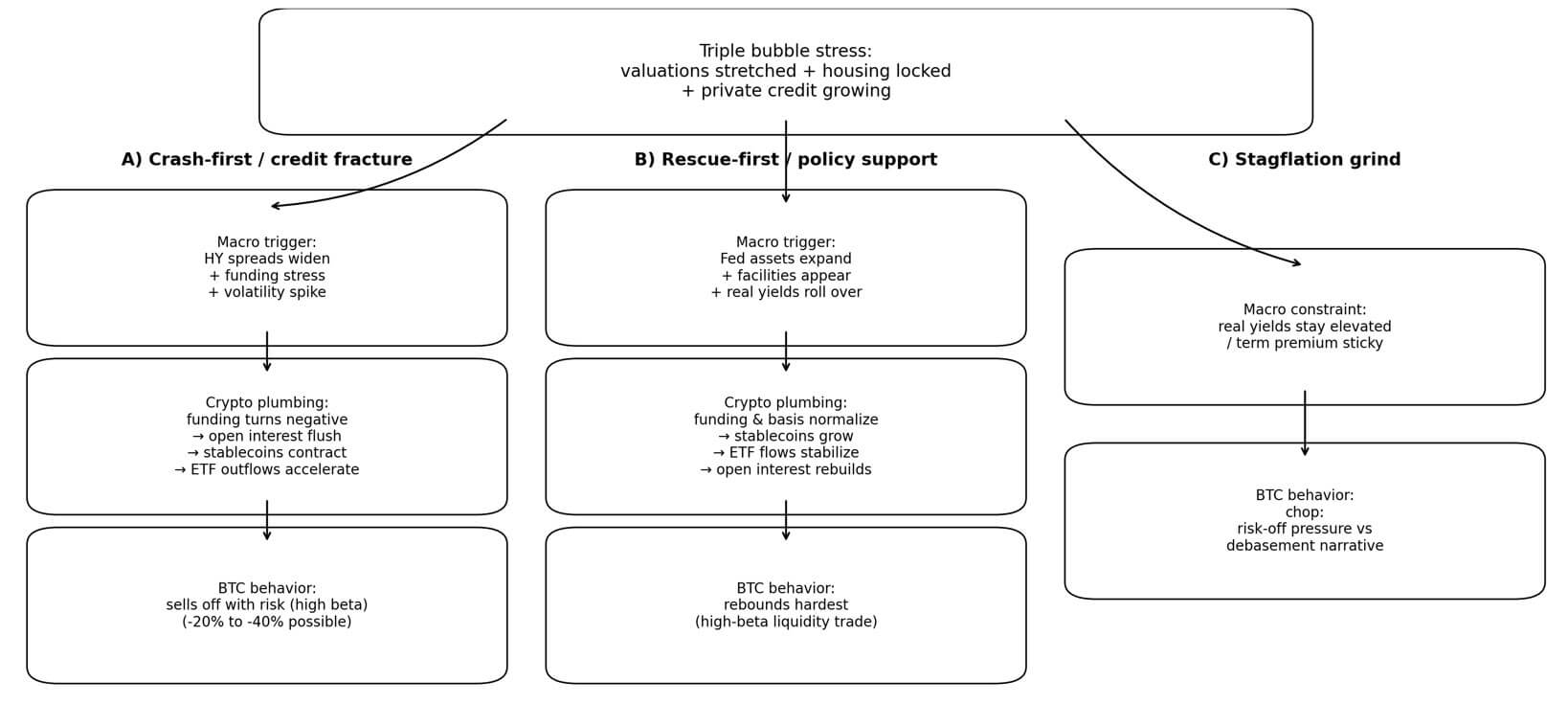

Macro strategist Michael Pento describes the current setup as a “triple bubble”: equities priced near historic extremes, housing constrained by mortgage rates near 6%, and private credit racing toward $2 trillion in assets under management. The label is provocative, but the framework is useful because it emphasizes sequencing.

If credit fractures first, liquidity evaporates, and Bitcoin likely sells off alongside everything else. If policy support arrives before a fracture spreads, Bitcoin may instead behave as a high-beta liquidity trade, rebounding faster than traditional risk assets.

The system rarely breaks because valuations look stretched. It breaks when credit and bond plumbing force selling, and Bitcoin’s 24/7 liquidity means it trades both the panic and the rescue harder than almost anything else.

Recent data shows stress signals accumulating without yet tripping a fracture.

The ICE BofA US High Yield option-adjusted spread registered 2.95% on Feb. 23, still tight relative to crisis regimes.

The Federal Reserve's balance sheet stood at $6.613 trillion on Feb. 18, up roughly $28.8 billion over four weeks, a modest expansion that doesn't signal emergency liquidity.

Real yields, measured by the 10-year TIPS yield, hovered around 1.80% on Feb. 20, elevated enough to pressure non-yielding assets. Stablecoin market capitalization sat at approximately $308.8 billion with a 30-day change of -0.18%, essentially flat.

Spot Bitcoin ETFs recorded roughly $2.6 billion in combined outflows since the start of 2026, with around $4.3 billion exiting over five weeks.

Bitcoin sells off first, questions later

A deflationary liquidation begins in credit markets, not equity indices.

High-yield spreads widen sharply, funding markets show stress, volatility spikes, and cash becomes the only position anyone wants.

Bitcoin's behavior in these windows is predictable: perpetual funding rates flip negative, open interest dumps as leveraged positions unwind, stablecoin supply contracts as liquidity exits the system, and ETF outflows accelerate.

March 2020 offers a clean historical anchor. Bitcoin collapsed nearly 40% on Mar. 12 during the global liquidity shock, selling off alongside equities, credit, and commodities as participants scrambled for dollar liquidity.

A credit-driven liquidation can easily produce -20% to -40% moves in Bitcoin within days.

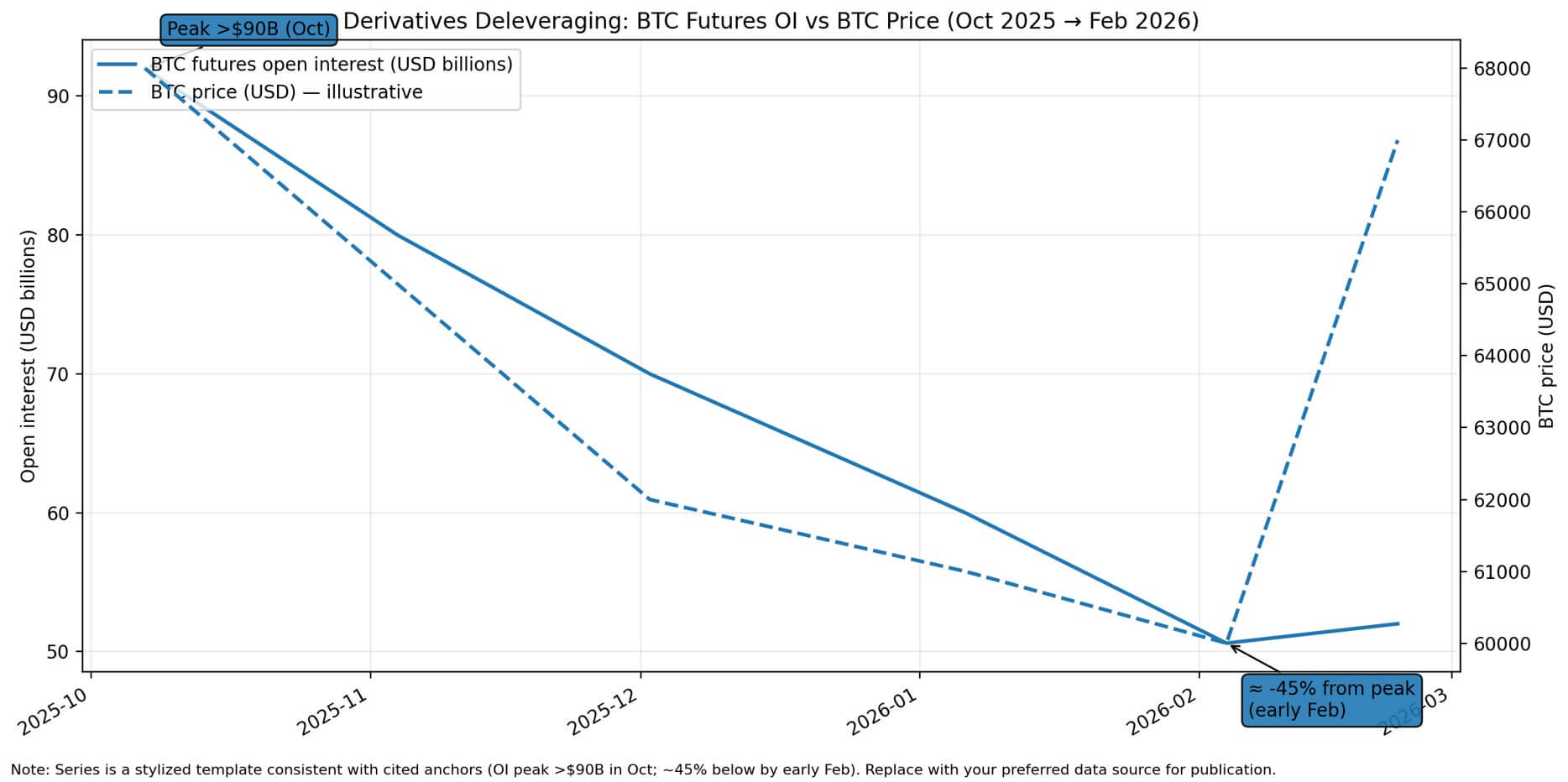

VanEck noted in early February 2026 that Bitcoin futures open interest peaked above $90 billion in October, and the market has since shed more than 45% of peak leverage, leaving room for further forced selling if credit stress materializes.

Moody's expects private credit assets under management to surpass $2 trillion in 2026 and approach $4 trillion by 2030, with Reuters reporting that Bank of America has committed $25 billion to the space.

The growth concentrates credit risk in less-transparent structures with longer lockups and weaker covenant protections.

If a credit event triggers forced asset sales in private credit portfolios, the ripple hits public markets through collateral calls and margin pressure. And Bitcoin, as the most liquid 24/7 risk asset, absorbs selling disproportionately.

Bitcoin front-runs the policy response

The opposite sequence begins with visible policy support.

The Fed's balance sheet expands, emergency facilities appear, and real yields fall. Bitcoin's response in these regimes is equally predictable: funding and basis normalize, stablecoin supply rises as liquidity returns, ETF flows stabilize or flip positive, and open interest rebuilds.

In a visible rescue regime, Bitcoin often behaves like a high-beta liquidity trade, recovering faster than traditional risk assets because it carries no credit risk, no earnings to disappoint. It acts as a liquid claim on a fixed-supply monetary asset that benefits when real yields fall.

March 2023 banking turmoil provides the template. Bitcoin rose 26% in a week and roughly 40% in 10 days as banking stress shifted expectations toward easier policy, front-running the Fed's eventual liquidity support.

In February 2026, Bitcoin whipped from around $60,000 to above $70,000 in a single day, its largest one-day rise since March 2023, highlighting how macro risk sentiment remains the dominant driver during stress windows.

March 2020 saw Bitcoin collapse alongside everything else, but it also saw the Fed cut rates to zero, launch unlimited quantitative easing, and establish emergency lending facilities within weeks.

Bitcoin recovered from its Mar. 12 low and quintupled over the next year as real yields stayed deeply negative and fiscal spending exploded.

The lesson is that Bitcoin trades the liquidity cycle with a higher beta than almost any other asset, and timing matters more than narrative.

When neither path dominates

The messiest scenario is one in which inflation remains sticky, bond markets demand higher term premiums, and real yields remain elevated, limiting policymakers' ability to deliver a swift rescue without reigniting inflation concerns.

In this regime, Bitcoin chops. Risk-off pressure competes with debasement-hedge narratives. Rallies fade when real yields prove sticky, or policy support disappoints.

The 10-year TIPS yield at 1.80% sits well above the zero-to-negative real yields that characterized Bitcoin's strongest periods.

Freddie Mac's 30-year fixed mortgage rate averaged 6.01% as of Feb. 19.

The Buffett indicator, around 206%, the highest level in the series' history according to Advisor Perspectives, suggests equity valuations leave little room for multiple expansion without earnings growth or falling discount rates.

If credit stress arrives without a rapid policy pivot, Bitcoin faces a regime in which neither the liquidation nor the rescue path dominates.

Tracking the transition

A simple framework for tracking which regime is active combines four inputs refreshed weekly: the change in Fed total assets over four to eight weeks, the change in stablecoin market capitalization over 30 days, the change in high-yield spreads over two to four weeks, and the change in 10-year real yields over two to four weeks.

When the score plunges, Bitcoin tends to trade like a high-beta asset during a liquidity event. When the score turns up, Bitcoin tends to outperform as reflation expectations build.

Current readings suggest a neutral-to-negative liquidity backdrop.

The Fed's balance sheet is up modestly but not surging. Stablecoin supply is flat to slightly down. Credit spreads remain tight. Real yields are elevated and sticky. Bitcoin spot ETFs are seeing sustained outflows, and derivatives open interest has fallen by nearly half from its peak.

The setup resembles a market waiting for a catalyst, either credit stress that forces liquidation or policy support that reignites the liquidity trade.

| Indicator | Latest reading (date) | Direction (↑/↓ + timeframe) | Interpretation (Liquidation / Rescue / Neutral) |

|---|---|---|---|

| ICE BofA US High Yield OAS | 2.95% (Feb 23) | → tight / not widening (snapshot) | Neutral (no credit fracture signal yet) |

| Fed total assets (WALCL) | $6.613T (Feb 18) | ↑ +$28.8B / 4w | Neutral → Rescue (mild) (modest expansion, not emergency) |

| 10y TIPS real yield | ~1.80% (Feb 20) | → elevated / sticky (recent weeks) | Neutral → Liquidation (tight) (higher real yields pressure risk assets) |

| Stablecoin market cap | $308.8B (latest) | ↓ -0.18% / 30d | Neutral → Liquidation (mild) (liquidity not expanding) |

| Spot $BTC ETF flows | -$2.6B YTD; -$4.3B / 5w | ↓ outflows (YTD + 5-week streak) | Liquidation (risk-off positioning) |

| $BTC futures open interest | Peak >$90B (Oct); ~-45% from peak | ↓ deleveraging since Oct | Neutral → Liquidation (less leverage, but reflects ongoing risk-off) |

| 30y fixed mortgage rate (Freddie Mac) | 6.01% (Feb 19) | → elevated (recent weeks) | Neutral (tight housing finance; stress backdrop, not a trigger alone) |

| Buffett indicator (market cap/GDP proxy) | ~206% (Jan 2026) | ↑ elevated (structural) | Neutral (setup) (valuation risk amplifier, not the plumbing trigger) |

| Private credit AUM + bank commitment | >$2T (2026); ~ $4T (2030); BofA $25B | ↑ structural growth (multi-year) | Neutral → Liquidation risk (setup) (opacity/lockups can amplify a credit shock) |

The tells arrive in credit plumbing

The actionable monitoring framework focuses on credit and crypto plumbing. High-yield spreads inflecting higher from tight levels signal credit market confidence eroding.

Treasury volatility and term premium pressure reveal whether bond markets are pricing policy flexibility or constraint. A Fed balance sheet that stays flat or declines while spreads widen confirms the absence of a backstop.

On the crypto side, sharply falling open interest indicates forced selling. Contracting stablecoin market capitalization shows liquidity leaving the system. Persisting ETF outflows confirm institutional risk-off positioning.

Rescue confirmation arrives through different channels.

Fed total assets rising meaningfully week over week signals active liquidity provision. The 10-year TIPS yield rolling over shows real yields falling. Stablecoin supply growing alongside normalizing derivatives funding confirms liquidity returning to crypto markets.

The transition from liquidation to rescue often happens fast, as March 2020 saw Bitcoin collapse and rebound within weeks as policy support materialized.

The triple bubble thesis is most useful not as a prediction but as a sequencing framework.

Credit fractures force liquidations, during which Bitcoin trades for pennies on the dollar. Policy rescues create liquidity surges, with Bitcoin front-running traditional assets.

The current macro setup, consisting of stretched valuations, elevated real yields, tight credit spreads, flat stablecoin supply, and persistent ETF outflows, suggests markets are positioned for stress but haven't yet experienced the credit plumbing failure that forces selling.

Bitcoin's next major move depends less on whether a bubble exists and more on whether credit breaks before the Fed rescues it.