The total crypto market capitalization rejected at $1.13 trillion on Feb. 16, but there was no change in the month-long ascending channel structure. More importantly, this level represents a 43% gain in 2023, which is far from the $3 trillion level achieved in Nov. 2021. Still, the current recovery is notable.

As shown above, the ascending channel initiated in mid-January has left some room for a 10% correction down to $1 trillion without breaking the bullish formation.

Investors reacted positively to the 5.6% year-on-year U.S. CPI inflation increase on Feb. 14 and the 3% retail sales monthly growth on Feb. 15. Bitcoin (BTC) had the biggest positive impact on the total crypto capitalization as its price gained 12.5% on the week.

One area of concern is a Feb. 16 story on Binance.US financial transactions to Merit Peak, a trading firm managed by CEO Changpeng Zhao. Interestingly, Reuters reported that a Binance.US spokesperson said Merit Peak was neither trading nor providing any kind of services on the Binance.US platform.

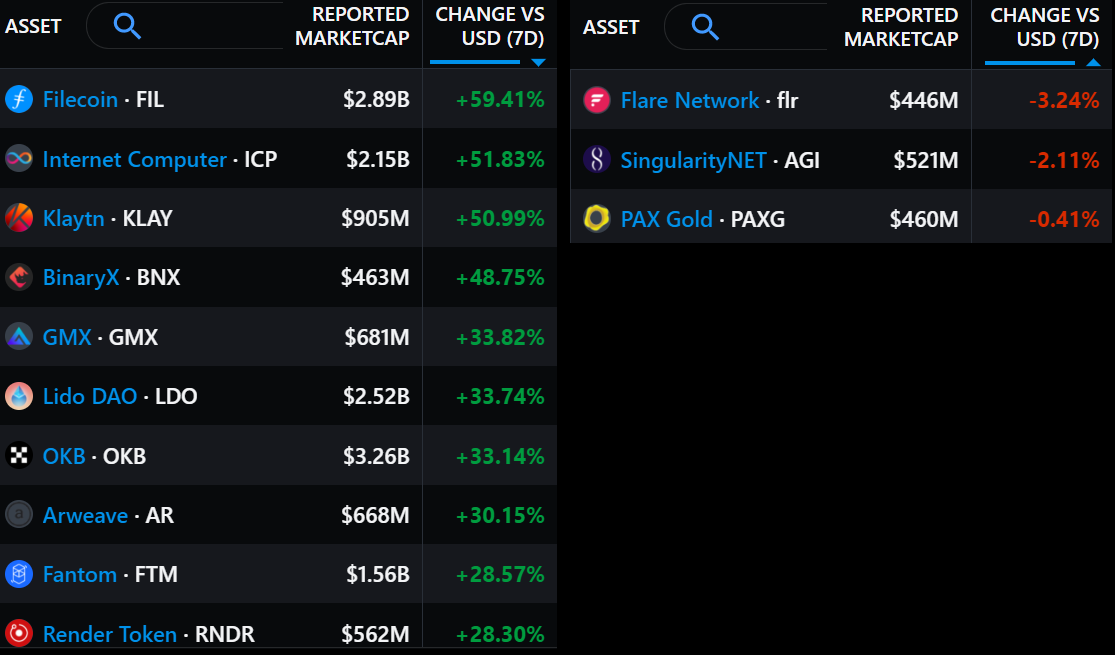

The 10.1% weekly increase in total market capitalization was held back by the modest 1.8% gains from BNB and the XRP 2.5% price increase. On the other hand, only 3 out of the top 80 cryptocurrencies finished the week with negative performances.

Decentralized storage solutions Filecoin (FIL) gained 59% and Internet Computer (ICP) soared 52% as Bitcoin blockchain demand for NFT inscription vastly increased the block space.

GMX rallied 34% as the protocol received $5 million in transaction fees on a single day.

Lido DAO (LDO) gained 34% as stakers evaluated proposals to manage the 20,300 ETH held by the corporate treasury.

Leverage demand is balanced despite the generalized rally

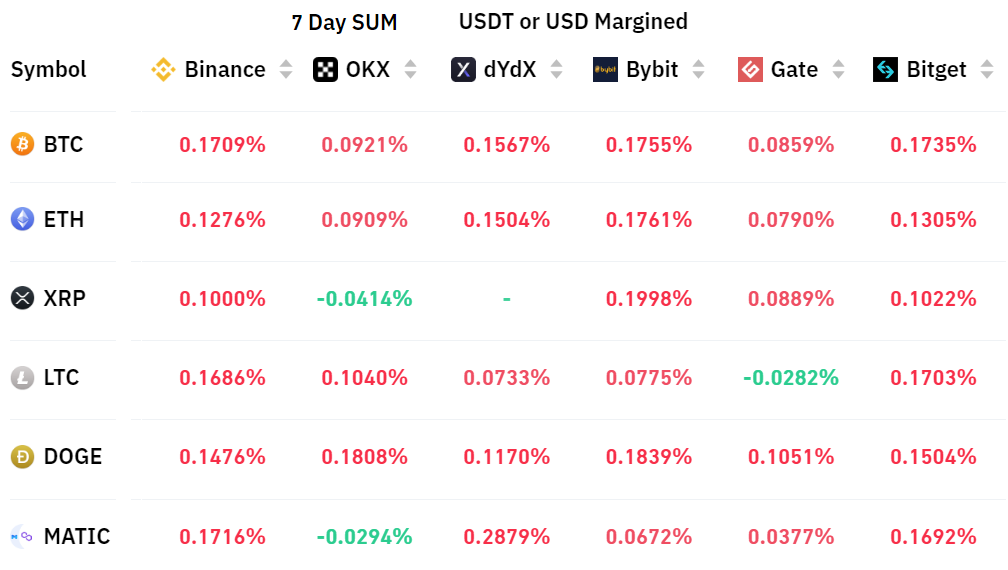

Perpetual contracts, also known as inverse swaps, have an embedded rate that is usually charged every eight hours. Exchanges use this fee to avoid exchange risk imbalances.

A positive funding rate indicates that longs (buyers) demand more leverage. However, the opposite situation occurs when shorts (sellers) require additional leverage, causing the funding rate to turn negative.

The 7-day funding rate was close to zero for Bitcoin and Ethereum, meaning the data points to a balanced demand between leverage longs (buyers) and shorts (sellers).

Interestingly, BNB is no longer a top-6 cryptocurrency ranked by futures open interest as investors' demand for Polygon (MATIC) markets increased by 70% in February.

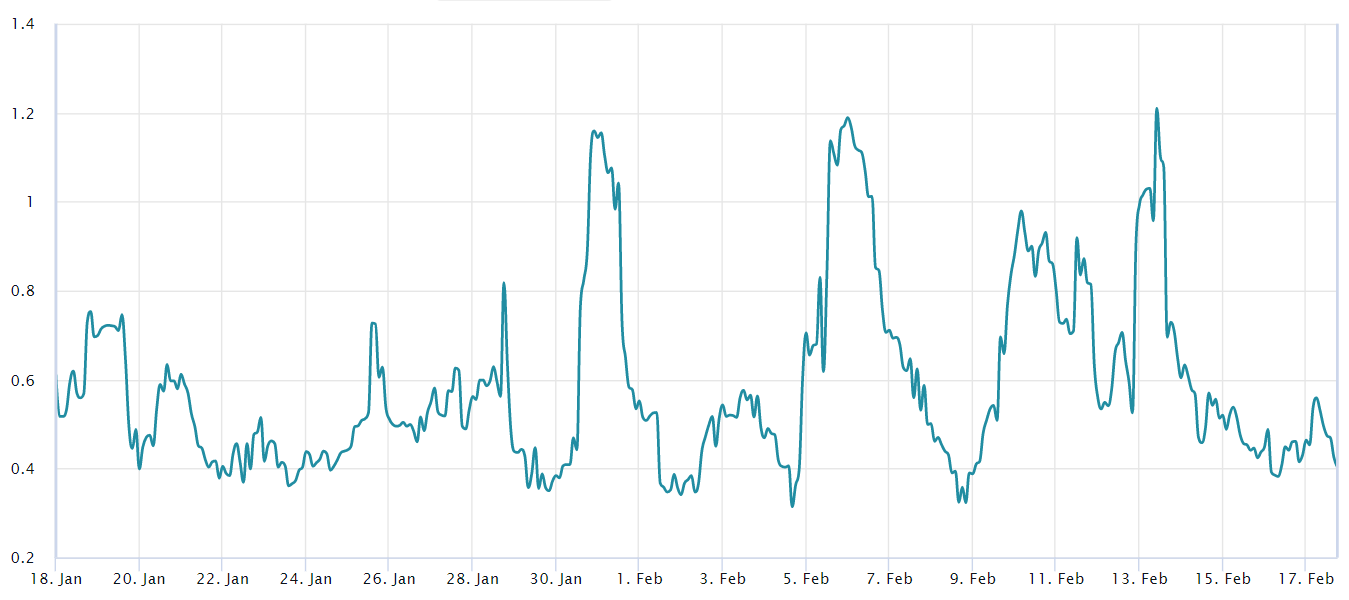

The options put/call ratio remains optimistic

Traders can gauge the market's overall sentiment by measuring whether more activity is going through call (buy) options or put (sell) options. Generally speaking, call options are used for bullish strategies, whereas put options are for bearish ones.

A 0.70 put-to-call ratio indicates that put options open interest lag the more bullish calls by 30% and is therefore bullish. In contrast, a 1.40 indicator favors put options by 40%, which can be deemed bearish.

Related:Bitcoin price derivatives look a bit overheated, but data suggests bears are outnumbered

Even though Bitcoin's price failed to break the $25,000 resistance, the demand for bullish call options has exceeded the neutral-to-bearish puts since Feb. 14.

Presently, the put-to-call volume ratio nears 0.40 as the options market is more strongly populated by neutral-to-bullish strategies, favoring call (buy) options by 2 times.

From a derivatives market perspective, there are no signs of demand from short sellers, while leverage indicators show bulls are not using excessive leverage. Ultimately, the odds favor those betting that the $1.13 trillion total market cap resistance will break, opening room for further gains.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

The views, thoughts and opinions expressed here are the authors’ alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.