After severe boom and bust phases, how can we gauge the importance of blockchain-based assets? Will they interface with daily life or remain on the margins of regulatory containment?

Above all else, one must notice that digital assets represent the next evolutionary step brought about by the internet. The World Wide Web decentralized information sharing, rendering gatekeepers into redundant friction points.

By the same token, blockchain technology decentralized financial assets or is in the process of doing so.

Potential of Blockchain and Digital Assets

From time immemorial, the core problem of finance centered around methods to keep an account of wealth. Either governments or banks have been responsible for maintaining the record of who owns what assets and who transfers those assets to whom.

This methodology became entrenched in the absence of alternatives, making money the subject of manipulation, eroding the potential to save, and forcing consumers to look for alternative mechanisms to save their purchasing power. One of these corrosive manifestations is setting the inflation target at 2% without having the ability to explain the reasoning behind it coherently.

Wow. This clip is amazing.

Powell is asked “why is 2% the inflation target?”

His answer sounds like it was written by Kamala Harris.

pic.twitter.com/lTgi6455En

— Chris Blec (@ChrisBlec) August 10, 2023

Bitcoin broke through this historical barrier as a product of a publicly distributed ledger – blockchain. The combination of a distributed ledger and a peer-to-peer verification/mining network made Bitcoin the vanguard of a truly decentralized, permissionless financial system.

Everything else that followed was built on this concept. At the core, BTC token is a smart contract, interfacing with other smart contracts, their authenticity secured by the blockchain network. In turn, any existing logic can be tokenized and secured on other blockchains using similar authentication techniques:

- Lending and borrowing: Aave, Compound Finance, Maker, Solend

- Asset exchange: Uniswap, Sushiswap, Curve, dYdX

- Play-to-earn gaming: Axie Infinity, Splinterlands, Gods Unchained

- Non-fungible tokens (NFTs): from artworks, real estate and audio albums to ebooks

- Micro-insurance products to the unbanked: Nexus Mutual, Solace, InsurAce

The common theme is that blockchain enables the expression of wealth in tokenized form to be accessed permissionlessly without third-party interception. Alongside the stock market, a permissionless crypto market emerged, with all its benefits and flaws. In the transition between TradFi and DeFi, stablecoins have proved especially popular.

Anchored to fiat currency value, these tokens are poised to become a major demand source for US treasuries – monetized government debt. Already, the largest stablecoins, USD Coin (USDC) and Tether (USDT), back their tokens with billions in short-dated US treasuries. The latest stablecoin newcomer, PayPal USD (PYUSD), does the same.

The value of tokenized wealth then becomes an extension of the existing central banking system, as noted by Federal Reserve Chair Jerome Powell in June 2023:

“We do see payment stablecoins as a form of money, and in all advanced economies, the ultimate source of credibility in money is the central bank.”

Likewise, the testament to the power of smart contracts is expressed through upcoming central bank digital currencies (CBDCs). The question is not whether the blockchain revolution will fizzle out but what form it will take.

As the discourse around the future trajectory of digital assets deepens, many traders find it imperative to manage day trading alongside full-time commitments to stay ahead, highlighting the rapid evolution and depth of today’s financial landscape.

Will decentralized and permissionless digital assets be suppressed in favor of centralized and permissioned digital assets? Will the informal taxation through inflation continue unimpeded? Will smart contracts in CBDC form transmogrify beyond mere payment tools into something else?

This is the current powerplay landscape of global finance. Making the banking system redundant, both central and commercial, cannot go without friction. The present Securities and Exchange Commission (SEC) Chair Gary Gensler best exemplifies that friction.

SEC Chairman Gary Gensler’s Approach

Following the blockchain (r)evolution, two types of frictions emerged:

- Digital asset flood

- TradFi counter-reaction

One friction rubbed against the other, or more precisely, fed into the other.

When something is of a digital nature, permissionless to boot, it becomes effortless to copy. But that copying often came with a deceptive, scammy tweak. In the fog of thousands of altcoins and relentless crypto scams/exploits that followed, a justified narrative emerged:

“This asset class is rife with fraud, scams and abuse in certain applications. We need additional congressional authorities to prevent transactions, products and platforms from falling between regulatory cracks.” – Gary Gensler, SEC Chair, in August 2021

Having been on the job for three months, this set the stage for DeFi’s interface with TradFi. At the Aspen Security Forum that month, Gensler laid the groundwork for counteracting the new digital asset class. Interestingly, he opened his speech by recognizing Satoshi Nakamoto’s historic contribution:

“But Nakamoto had solved two riddles that had dogged these cryptographers and other technology experts for a couple of decades since the dawn of the internet. First was how to move something of value on the internet without a central intermediary…

…And move something of value on the internet without a central intermediary and relatedly, how to prevent what’s called double spending of that valuable digital token.”

Yet, to place the emerging tokenization sector under the federal fold, Gensler framed it as a threat to national security. One that involves “money laundering, tax compliance, sanction”. Gensler’s solution was to exercise the Investment Company Act to designate nearly all cryptocurrencies as securities retroactively.

“Well, it’s basically an anticipation of profits on the efforts of the sponsor or others and so forth. And that is… It depends on the facts and circumstance, but that is the story of a lot of these circumstances.”

Without any crypto legislation, the SEC ruled by enforcement on that basis. Gensler’s framework kicked off with Coinbase. A month after the Aspen speech, Coinbase CEO Brian Armstrong publicly put into question SEC conduct.

The gist is that the SEC’s mission to protect investors, under heightened transparency, turned into obfuscation and selective targeting to set pseudo-crypto law.

Legal Pushback and Congress’ Role

The digital asset space underwent major contraction within two years following Gensler’s pivotal Aspen note. The SEC sanctioned multiple crypto exchanges and digital asset protocols as unregistered securities brokers and clearing houses.

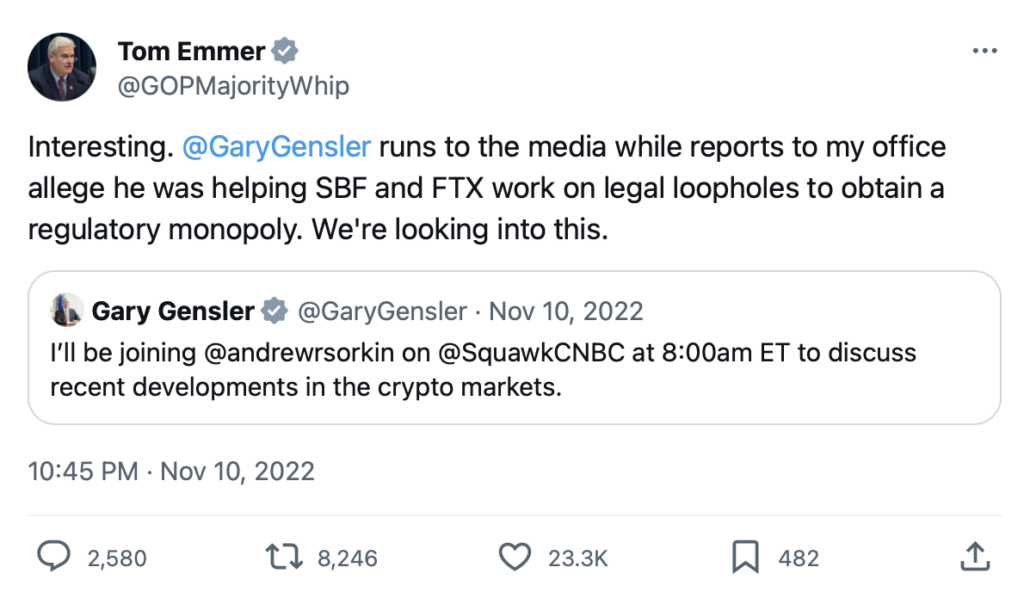

During the period, the SEC’s investor protection mission failed spectacularly, as evidenced by the multi-billion losses of funds in FTX and Celcius, to name a few. Some lawmakers had noticed this pattern, referring to Gary Gensler, SEC Chair:

“This guy in my mind, is a bad-faith regulator. He’s been blindly spraying the crypto community with enforcement actions while completely missing the truly bad actors.” – Congressman Tom Emmer, House Majority Whip

Soon after, together with Warren Davidson, Emmer introduced the “SEC Stabilization Act” in order to remove Gary Gensler following his “long series of abuses”. In addition to displacing Gensler, the act would limit commissioners to only three seats per political party at any given time. Purportedly, this would prevent the infusion of political agendas into SEC’s operations.

In the meantime, as the SEC filled the legislative void, the watchdog agency suffered serious legal pushback. The latest legal defeat comes from the federal judge denying SEC’s appeal in the landmark Ripple Labs case that affirmed XRP as not a security.

If the case had gone into the other direction, the SEC would’ve drastically expanded its leeway to curtail the digital asset class. Moreover, the agency lost the case against Grayscale Investments regarding the refusal to convert Grayscale Bitcoin Trust (GBTC) into an ETF.

The SEC’s refusal to approve a single Bitcoin ETF has been another signal of bad-faith acting. It has been speculated that legitimizing Bitcoin in this manner would open capital floodgates too much before the digital class arena is under firmer federal oversight.

Another such signal came from the historic FTX crypto fraud involving Sam Bankman-Fried (SBF). The incarcerated ex CEO met with Gensler on multiple occasions, yet failed to notice any red flags. Congressman Tom Emmer suggested that this may have been a ploy to place FTX as the designated dominant market maker in the crypto space.

The connection there is circumstantial for the time being, based on Gary Gensler serving as MIT lecturer under the department of Glenn Ellison. He is the father of Caroline Ellison, SBF’s ex partner and Alameda Research CEO.

Alameda served as a slush fund for FTX to funnel customer assets. Caroline Ellison had pleaded guilty to seven counts of fraud in December 2022. It is speculated that her cooperation will secure SBF’s conviction in the upcoming trial.

The Bipartisan Consensus Still to Materialize

Regardless of how one perceives SEC’s behavior so far, the agency acted without any crypto legislation, positive or negative. Therefore, to stabilize the crypto market long term with clear rules of engagement, bipartisan effort needs to take place.

This comes from the Bipartisan Blockchain Innovation Project (BBIP). The non-profit organization is co-chaired by Congressman Tom Emmer (R-MN) and Congressman Darren Soto (D-FL).

BBIP aims to both educate lawmakers and to craft a legislative framework that supports the growth of the blockchain industry in the United States. BBIP’s work has resulted in multiple bill proposals:

- The Token Taxonomy Act (H.R. 7081)

- The Blockchain Research and Development Act (H.R. 5437)

- The Blockchain Regulatory Certainty Act (H.R. 4337)

- The Digital Asset Regulatory Transparency Act (H.R. 4214)

- The Financial CHOICE Act (H.R. 10)

However, as none of the bills have passed as laws, it is unclear if education is the deciding factor in crypto legislation, or is it a matter of timing and politics.

Consequences of Over-Regulation

It is safe to say that US lawmakers have been dragging their feet when it comes to setting the rules for the digital asset ecosystem. As the SEC took the steering wheel, long-standing FinTech hubs, from Singapore and Hong Kong to Abu Dhabi, have taken advantage of this.

This is best exemplified with the US-based stablecoin (USDC) issuer Circle. After the SEC charged Binance for multiple violations in June, including for trading Binance USD (BUSD) stablecoin, Circle CEO Jeremy Allaire argued that stablecoins should be exempt from “nearly everything is a security” SEC onslaught:

“The SEC’s claim that Binance offered and sold its competing stablecoin as an unregistered security raises serious legal questions affecting digital currency and the U.S. economy more broadly.” – Circle’s amicus brief to the SEC

As tokenized dollars, stablecoins are the most popular digital asset for daily global transactions. Yet, the off-shore Tether issuer of USDT enjoys the largest capitalization at $83.4 billion, out of which $72.5 billion is backed by US treasuries. This is more than entire countries hold, from Mexico and Australia to Spain and UAE.

For comparison, the US-based Circle stablecoin issuer of USDC has a modest $25.2 billion market cap.

In other words, an offshore company utilizes the very currency the SEC is indirectly protecting as the arm of the central banking system. Therefore, the SEC created such restrictive conditions that going fully offshore is a better bet than enjoying the SEC’s protection of capital markets.

If this continues, the US is poised to oust the digital asset market via the deadly combo of legislative inaction and regulatory over-action.

Conclusion

Blockchain hype birthed countless scams, yet the foundation stands on firm legs. This is evidenced by blockchain/smart contract application in the central banking system itself – upcoming CBDCs.

Because blockchain (r)evolution came from the private sector, spearheaded by Bitcoin, it took TradFi off guard. Once it became clear that digital assets are only poised for growth, regulatory mechanisms sprung into action.

And they had a good reason to do so, amid regular crypto scams. But there is little evidence for beneficial regulatory protection to be found. If anything, regulatory overreach appears to have designated the US market as too burdensome and risky, further pushing digital assets into the gray zone.

For now, the digital US market is running on fumes of its depth, but how long can this last until advantage is permanently lost?