The evolution of DeFi’s most valuable project has trended towards centralization. Whether it be the small number of users who hold its governance token, MKR, or collateralizing centralized digital assets, Maker has had to make some ideological concessions to stay afloat.

This, however, shouldn’t be the project’s primary concern, said CEO Rune Christensen.

Maker Hedges Include Centralization Risk

In an interview with Crypto Briefing, Christensen explained why the world’s first decentralized bank added a centralized asset like Circle’s stablecoin, USDC.

“We want to spread the risk of liquidation across a variety of assets,” he said. “It’s a balancing act between centralization and black swan events.”

Using Ethereum’s native asset, Ether, for instance, means that Maker exposes itself to volatility risk. On Mar. 12, during a massive drop in the crypto markets, a tumbling ETH price created a mass of liquidations on the Maker platform.

This, according to many in the crypto space, was a black swan event. One way to fix this and prevent future liquidations, at least for Maker, has been to collateralize a stablecoin like USDC.

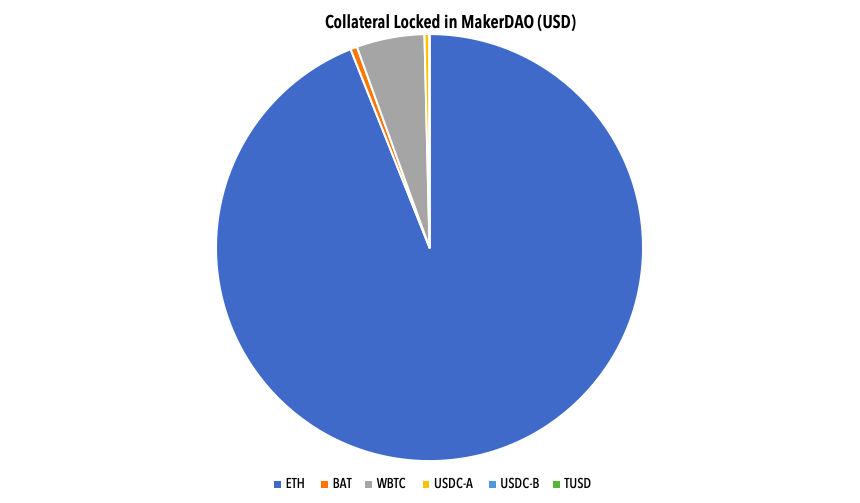

Collateral assets on Maker allow users to “lock-up” these assets in exchange for the platform’s stablecoin, DAI. At the time of press, users can lock up Brave’s Basic Attention Token (BAT), Ether (ETH), USDC, TrustToken’s TUSD, and wrapped Bitcoin (wBTC).

Integrating USDC was met with backlash from the community as the token is centralized in the hands of Circle. According to Circle, “a global blacklist is maintained by the USDC smart contract, and this was implemented to comply with legal requirements such as a court order or global sanctions restriction.”

How to throw away your product market fit after working on it for literally years (see below).

I feel sorry for the people who helped build Maker to what it before today – only for USDC to be added as collateral. https://t.co/aUZ6ThFn2X

— $KERMAN (@kermankohli) March 17, 2020

In integrating Ether, Maker onboards volatility risk. “In the case of USDC, we risk getting blacklisted,” said Christensen.

It is in these minor concessions, when spread across the decentralized bank’s portfolio, that Maker hopes to withstand just about any event without collapsing entirely.

It was for this reason that they also added BitGo’s wrapped bitcoin (wBTC).

4 million Dai was just minted with WBTC in a single transaction. This really showcases the latent demand for non-ETH assets, and it's the beginning of a broader trend of DeFi acting as an economic vacuum that will eventually attract almost all value to the Ethereum blockchain.

— Rune Christensen (@RuneKek) May 20, 2020

Like USDC, wBTC is a centralized asset controlled by BitGo. It offers stability and may entice Bitcoin users to join the Ethereum-dominated DeFi movement. Michael Anderson, a co-founder at Framework Ventures, told Crypto Briefing:

“Bitcoin is 7 to 8 times more liquid than current offerings. It could be break out moment for DeFi.”

Despite earlier criticisms, both wBTC and USDC have found some traction on the platform. DAI Stats reports 1.9 million USDC ($1.9M), and ~2,600 wBTC (~$25M) are currently held in collateral. Ether continues to dominate, however, with over 1.9 million ETH ($461.5M) locked in.

Though Ether primarily backs DAI, many in the community have nonetheless begun referring to the stablecoin as “semi-centralized.” Anderson said:

“The centralization risk of wBTC is more philosophical than anything else. And we may use USDC because of its efficiency, but you need to think about how comfortable you are with this risk. How is the wBTC held at Bitgo, for instance?”

A Concentration of Governance Tokens

The crash in March imperiled the entire DeFi space, not just Maker. “People failed to understand the risks,” said Christensen. “Systemic leverage was a problem across all of DeFi.”

Maker’s governance community, however, did an excellent job of picking up the pieces. The Maker CEO added:

“The community was focused on a goal-oriented way of fixing the system. They changed the auction parameters, and added new collateral to create more liquidity.”

Indeed, the move was swift and decisive. Outside of adding more liquid collateral, adjusting incentives to return DAI’s 1:1 dollar equivalency, the team also sold governance tokens to help restore the project’s debts.

Although the auction raised $5.3 million, Maker’s centralization woes have continued.

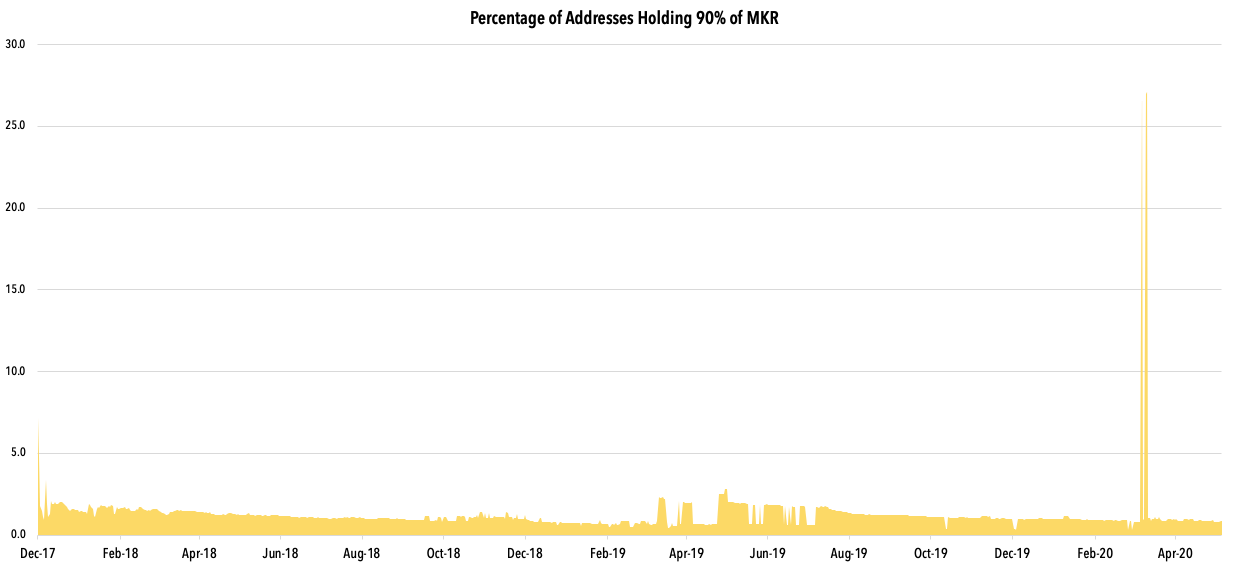

Of the 106 MKR token auctions, Paradigm and the Maker Foundation won 105 of them. Further investigation from Crypto Briefing revealed that 1% of the MKR addresses hold 90% of the MKR tokens.

Christensen admits that the distribution of the governance tokens has been challenging to design. Maker’s centralization concerns may even continue over a long enough time frame, he said.

But he believes that the incentives in place prevent this kind of centralization from being a significant issue. “In the worst-case scenario, users could simply hard fork the protocol away from MKR holders,” he said.

Who Needs Maker More than DeFi?

Saving Maker, as well as its stablecoin, has been critical for keeping DeFi afloat. At the time of press, Maker makes up more than half of all value locked into the DeFi sector.

And though Ethereum’s favorite stablecoin is an ERC-20 version of USDT, Tether has been less than transparent. It is for this transparency that Michael Anderson and Framework Ventures have become such champions of DeFi.

“We love DeFi because it adds this transparency that doesn’t exist in traditional finance,” he said. “Even the latest Bitcoin flash crash indicated some odd trading behavior.”

For Christensen and the Maker project, this is only the beginning. Maker’s centralization concerns aside, the project will continue working towards inclusive finance.

The latest governance proposals include the collateralization of real-world assets like music royalties and invoices thanks to a tie-up with Centrifuge.

The @MakerDAO governance is ~2hrs away from finalizing vote on adding 10 new collateral types (both trustless tokens & real-world assets) to its generalized lending protocol. Pulled some governance stats last night. @paperchainio DROP token likely first real-world asset added pic.twitter.com/1le9QIFsXT

— David Gogel (古大卫) (@dgogel) June 8, 2020

“The next step is to bring real financial assets over to MakerDAO. Once this happens, this is when the real growth will begin to happen,” said Christensen. “We want to help people get mortgages in countries where this is particularly difficult, for instance. Or even offer small business loans with much less fees.”

He added that these kinds of features could happen in 2020, and if not, definitely next year.

Until then, members of the crypto community will be watching the experiment as it unfolds. If Maker finds success, it would further cement DeFi’s place in the world of finance.